Active Stock ETFs Are Poised to Take Off; Fund Companies Are Rolling Out Funds and Regulators Are Weighing New Designs

March 7, 2014 Leave a comment

Active Stock ETFs Are Poised to Take Off

Fund Companies Are Rolling Out Funds and Regulators Are Weighing New Designs

ARI I. WEINBERG

March 3, 2014 4:00 p.m. ET

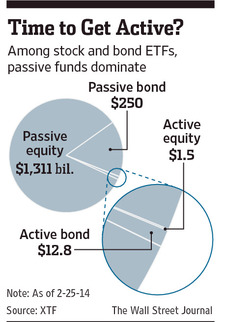

In the $1.7 trillion world of exchange-traded products in the U.S., one lonely corner of the market has received outsize attention lately: the so-far tiny realm of actively managed stock exchange-traded funds.

Such funds held just $1.5 billion, or 0.08% of the assets in U.S. exchange-traded products recently, according to researcher XTF Inc. But dramatic change could be coming, as big companies jostle to get into this business and the regulatory dam holding them back from certain new approaches appears to be getting leaky.

While the majority of exchange-traded funds to date have been products that track indexes, active equity ETFs represent a vast opportunity in the eyes of traditional mutual-fund managers, as well as some of the largest issuers of exchange-traded products. They figure active equity ETFs, with their lower costs and tax efficiency, could attract some of the approximately $6.1 trillion resting in actively managed stock mutual funds, as tallied by Morningstar Inc.

Still, some big hurdles remain for fund providers seeking to enter the business, as do questions about whether active ETFs truly represent an opportunity for investors.

‘Active’ Isn’t Easy

The fundamental challenge facing actively managed equity ETFs is the same one facing conventional stock mutual funds: The odds are stacked against active management.

While some active managers invariably will beat their benchmarks, others will trail theirs. On average, fund investors can expect to get market returns, reduced by the funds’ expenses, which generally are higher for active managers than for index funds because investors are paying for a stock picker’s expertise.

The long odds facing active managers are reflected in data from the S&P Indices Versus Active Funds Scorecard from McGraw Hill Financial’s S&P Dow Jones Indices: Over a five-year period through June 2013, almost three-quarters of U.S. active stock funds failed to outperform the S&P 1500 composite on a total-return basis.

Meanwhile, money is pouring into “smart beta” ETFs, which aim to beat the market by following a new generation of indexes designed to approximate fundamental stock-picking approaches. In some ways these funds, which account for nearly 10% of all U.S.-listed ETF assets, address the hope inherent in traditional active stock picking minus the higher fees.

Nevertheless, many investors remain interested in trying to outperform the broader market with funds run by stock pickers, says Todd Rosenbluth, director of ETF and mutual-fund research at S&P Capital IQ in New York. “Now, the products with which to do that in ETFs are arriving.”

AdvisorShares Investments LLC of Bethesda, Md., is among a small group of companies already trying to build businesses around active equity ETFs. In January, State Street Corp.’s State Street Global Advisors, along with MFS Investments, launched three such funds that collectively have about $15 million in assets. Others that have entered the arena include BlackRock Inc.’s iShares, Columbia Management, Invesco PowerShares and Cambria Investment Management Inc.

Meanwhile, USAA Asset Management, a unit of San Antonio-based USAA, has applied to the Securities and Exchange Commission for a handful of active equity ETFs, including several that closely align with existing equity and balanced funds.

So why aren’t more mutual-fund companies rushing to offer ETF versions of existing stock funds? One of the things holding them back is the current requirement that active ETFs, which trade on exchanges like stocks, disclose their portfolio holdings daily. Many fund managers fear that revealing their daily trades would make their funds more vulnerable to front-running—a situation in which opportunistic traders might push prices higher when they see a fund buying shares of a company, or hedge funds and others might short the ETF.

Others are concerned that lower-fee ETFs could cannibalize their existing business.

Is Nontransparent Next?

Still, take away the daily disclosure requirement and many fund companies say they would love to offer active stock ETFs. Some fund providers are trying to make that happen by seeking clearance from the SEC to build ETFs that would be permitted to reveal their holdings quarterly, like conventional funds, instead of daily.

BlackRock, State Street, T. Rowe Price Group Inc., Precidian Investments, Guggenheim Funds and Eaton Vance Corp. are among the companies that have designed fund and trading structures to bring “nontransparent,” active management to equity ETFs.

There was “a long period of radio silence” in which the SEC didn’t appear to be moving ahead on pending applications for nontransparent active ETFs, says Stuart Strauss, a lawyer who specializes in investment companies and exchange-traded products at Dechert LLP in New York. That has changed recently: “The regulators are engaged and issuers are filing amendments to their applications in response to SEC comments.”

Adding to the momentum, major U.S. stock exchanges have recently proposed rule changes that would allow for the listing and trading of nontransparent ETFs. These changes, however, must be approved by the SEC.

Criticism of nontransparent ETFs centers on trading of the funds and whether investors and market makers would have enough information to keep the ETF price within an acceptable range around its indicative net asset value, a figure broadcast every 15 seconds that represents the value of the basket of securities and cash used to create new shares of an ETF.

Perils of Popularity

Vanguard Group, one of the largest issuers of ETFs, has yet to enter the active ETF arena, but transparency isn’t what is holding it back. Joel Dickson, a Vanguard investment strategist, says the firm is concerned that active equity ETFs, regardless of transparency, could run into capacity constraints.

The investment process of any active manager can be “compromised” by heavy inflows, says Mr. Dickson. For instance, when a small-stock fund gets very large, it becomes difficult for the manager to invest in tiny companies. In such cases, a fund company may close the fund to additional investments by some or all investors. It continues to redeem out existing investors at net asset value, or NAV, the once-a-day share price at which investors buy or sell.

That process is a little more complicated when it involves ETFs. That’s because the thing that keeps the market price of an ETF close to the underlying value of its holdings is the fact that certain market makers, known as authorized participants, can create and redeem shares. If an ETF closes to new creations, part of that mechanism is taken away, and the ETF could start trading at bigger premiums or discounts to the value of its underlying holdings.

Despite these and other concerns, active ETFs seem poised for expansion, experts say. But they say investors should proceed with caution. As with any active fund, it might be wise to wait for such strategies to prove their worth over time, they say.