Asia’s currency rollercoaster creates winners and losers

March 9, 2014 Leave a comment

March 6, 2014 4:10 am

Asia’s currency rollercoaster creates winners and losers

By Josh Noble in Hong Kong

Central bank policies in the US and Japan have buffeted Asian currencies in the past 12 months, sending the Indian rupee down 15 per cent, the yen lower by 10 per cent, and wiping a fifth off the value of the rupiah. But they have also created some unlikely winners and losers across the region, from Mickey Mouse to pickled cabbage.

The widening of South Korea’s kimchi deficit – whereby the country imported more of its national dish than it sold abroad – and the growing queues at Japanese theme parks are both manifestations of Abenomics, the pro-growth policies championed by Shinzo Abe, Japan’s prime minister, that began with easy money and a devaluation in the yen.

The weaker currency helped fuel a rise in inbound tourism and an increase in Japanese taking “staycations”. As a result, last year Disneyland Tokyo posted a record year for both revenue and visitor numbers. Tourist arrivals to Japan topped 10m for the first time in 2013, comfortably trumping the previous record of 8.6m, while outbound trips dropped by 5.5 per cent year-on-year.

The slide in other Asian currencies – prompted by the global “taper tantrum” in May last year that hit many emerging markets – has also given some a surprise boost. The 20 per cent fall in the rupiah and the 9 per cent drop in the baht in the past year has helped Thai and Javanese cattle herders funnel their fresh milk into the cappuccinos of dollar-based Hong Kong and Singapore.

Although fuel bills and wage pressures are pushing up production costs, Thai milk is still about 20 per cent cheaper than the Australian equivalent in Hong Kong, while Indonesian milk is 30 per cent less expensive. Thus both are expanding their market share in the city’s fridges and flat whites.

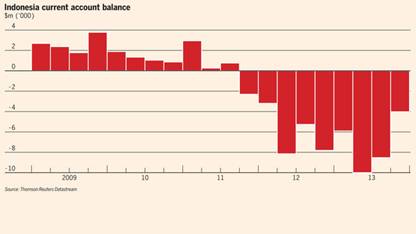

That news will be particularly welcome for the Indonesian authorities, who have been battling to close a damaging current account deficit. Rising exports – predominantly of commodities – are a key part of that effort, and were the main driver of Indonesia’s better-than-expected fourth quarter economic performance. Deficit countries were hit hardest in last year’s sell-off due to their reliance of external sources of funding.

But the latest round of the currency wars has also created plenty of losers. More tourism has not been enough to ease Japan’s growing trade deficit, which stands at a record high this year. With most natural resources priced in dollar, the country has been forced to import ever more expensive fuel to keep the lights on during its nuclear shutdown.

Energy-dependent businesses, such as the famous Japanese bath houses, have felt the chill of rising costs. Data released last month showed that commodity imports have been a major drag on growth, while domestic consumption is failing to pick up the slack.

Then there are the ailing South Korean cabbage patch owners. Japan is Korea’s biggest export market for kimchi – the fiery pickled cabbage served with almost every Korean meal. The slide in the yen has sapped Japanese demand for increasingly expensive kimchi, while cheap Chinese imports into Korea are on the rise. South Korea posted a kimchi trade deficit last year of $28m, a sevenfold increase on the previous year’s $4m.

The weaker rupiah is also draining plush swimming pools in Jakarta apartment blocks as expats paid in rupiah downsized to smaller, cheaper homes following last year’s slide in the local currency. While everyday items are priced in rupiah, many landlords and international schools charge expats in dollars.

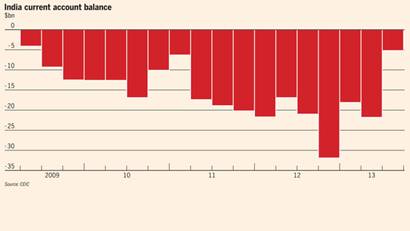

In India – another country hit hard by capital outflows last year – local shampoo producers that price their sachets at Rs1 a pop have problems, too. Faced with the rising costs of imported chemicals, some companies are mulling the unattractive option of a 100 per cent price increase.

But for sports fans, the woes of expats and cabbage farmers pale beside those of Australia.

Alessandro Del Piero was lured to the Australian league in part by the soaring Aussie dollar. The Italian footballer, having seen his earnings shrink by about 20 per cent against the euro since signing in the summer of 2012, is likely to play his last game for Sydney in August.

Last updated: February 19, 2014 8:13 pm

Australian central bank walks a currency tightrope

By Josh Noble in Hong Kong and Jamie Smyth in Sydney

When Italian football star Alessandro Del Piero quit Juventus for Sydney FC in Australia in September 2012, he may have had currency markets on his mind. The Australian dollar had just hit a record high against the euro, making his A$2m-a-year salary all the more attractive.

Since then, slowing growth in China – Australia’s biggest export market – and a central bank campaign to weaken the currency have taken their toll. Mr Del Piero has seen his earnings drop by 20 per cent in euro terms.

The fall in the Aussie has come too soon for the country’s foreign sports stars, but too late for its manufacturing industry. Over recent months Toyota and General Motors’ Holden unit have both decided to close their Australian factories by the end of 2017, which will end a 100-year tradition of making cars in the country.

This week Alcoa said it would close its Point Henry aluminium smelter with the loss of more than 1,000 jobs. Like the carmakers, Alcoa included the strength of the Aussie dollar during the country’s decade-long mining investment boom among its reasons for deciding it was not financially viable to keep the smelter operating.

The industrial sector may yet see brighter times – most analysts expect weakness in the Aussie over the next 12 months. ANZ’s currency team are “structurally bearish” on the currency and expect it to trade down to US$0.84 this year.

But the currency has hit a pocket of renewed strength against the US dollar in February. Since the start of the month, it has gained about 3 per cent to above US$0.90, its highest since early December.

The Aussie is widely considered a proxy for Chinese growth due to its exposure through commodity exports, so better economic data on the mainland has provided a boost. China’s trade numbers last month beat forecasts, while an unexpected boom in bank lending to start the year has prompting some investors to trim their bearish positions in the Aussie dollar.

“The rally has been predicated on people getting out of their short positions, and some better indications in the meantime from China,” says Sacha Tihanyi, FX strategist at Scotia Bank.

Meanwhile, the Reserve Bank of Australia’s campaign to weaken the currency via dovish rhetoric appears to have been put on hold due to worries about rising prices. Underlying inflation was 0.9 per cent in the fourth quarter and 2.9 per cent year on year – far higher than expected – leaving the RBA with limited room for manoeuvre.

“You can talk the currency down when you’ve got a fairly benign inflation profile, but once we got the [fourth-quarter] data – which showed a very strong upside surprise – all of a sudden you have to walk a bit more of a tightrope”, says Jonathan Cavenagh, FX strategist at Westpac.

The RBA’s own policy statement following the inflation reading showed a clear change in language towards the strength of the currency.

“I think the tone of the RBA’s commentary on the Australian dollar has shifted significantly since the upside surprise in the CPI numbers last month,” says Paul Bloxham, chief economist at HSBC bank. “I think the campaign to jawbone the Australian dollar lower is over, at least for the moment.”

The RBA now faces a trickier balancing act. While house prices are rising fast and consumers increasingly confident, the jobs market remains weak and wage growth tepid. Any move to cut rates to support economic growth risks further stoking inflation and property prices, while a rate increase would prompt renewed strength in the currency and delay much needed rebalancing.

“One of the potential risks on the upside for the [Aussie] dollar later this year is an increase in capital flows from Japan. This could be driven by signals from the RBA of a possible interest rate increase later in the year,” says Martin Whetton, rates strategist at Nomura.

Analysts say the RBA is likely to tolerate short-term strength up to about US$0.93, in spite of a previously stated preferred level of about US$0.85, but it may yet be forced to resume its linguistic intervention.

“If the RBA perceived a big speculative push to be long Aussie again, and financial interest driving a wedge between [the strength of the currency and] what they see as the fundamental interests of the economy, then they’ll start sounding more dovish,” says Mr Tihanyi.

Either way, Mr Del Piero already may have cashed out before then. He is likely to play his last game for Sydney in August when the Sky Blues take on his former club Juventus.