China Faces Test With Potential Corporate Bond Default; Government and Banks Have Stepped in to Avoid Past Failures; Investors and economists poised to cheer China bond default

March 9, 2014 Leave a comment

China Faces Test With Potential Corporate Bond Default

Government and Banks Have Stepped in to Avoid Past Failures

LINGLING WEI

March 5, 2014 7:55 a.m. ET

BEIJING—The first potential default in China’s fast-growing corporate bond market offers a test of whether Beijing will allow a long-taboo practice as it seeks to rein in runaway credit: corporate failures.

A deeply indebted Shanghai solar-equipment maker late Tuesday warned that it won’t be able to meet interest payments totaling 89.8 million yuan ($14.7 million) due on Friday on a bond sold two years ago, citing a cash squeeze and its inability to raise enough funds in time.

The potential default by Shanghai Chaori Solar Energy Science & Technology Co.002506.SZ +3.19% , though small, would mark the first time a Chinese company has defaulted on a bond traded in the mainland, according to Moody’s Investors Service. Phones at the company rang unanswered on Wednesday, and an investor relations employee’s mobile phone was turned off.

So far, the Chinese government and state-owned banks have largely kept risky borrowers afloat by providing bailouts or debt extensions, keeping borrowing costs low for companies with high debt.

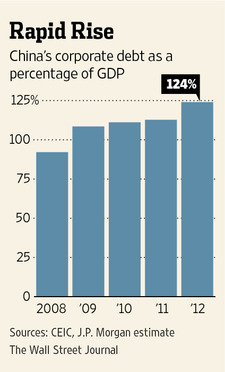

That has led many investors to flock to Chinese corporate bonds on the belief they have an implicit guarantee, helping to fuel growth. Total corporate bonds outstanding rose more than tenfold to 8.7 trillion yuan at the end of January from the end of 2007, allowing even weak borrowers to tap funds at relatively low rates.

“China needs real credit defaults to reduce the problem of moral hazard created by implicit guarantees and to develop a healthy credit market,” said Jian Chang, China economist at Barclays Capital. “That would also help reduce wasteful investment and a potential bad debt buildup.”

At the same time, a default would come amid rising worries about the overall Chinese financial system, which could face mounting bad debt as economic growth slows. Local governments and state banks have already moved to shore up troubled trust products, investment products in China that are less regulated than bonds.

Investors largely took the news in stride. An index that tracks 100 high-yield corporate bonds on China’s Shanghai and Shenzhen stock exchanges, called China Securities Index’s medium-high yield corporate bond index, on Wednesday dipped 0.3%.

Shanghai Chaori’s disclosure came as China’s national legislature began its annual meeting in Beijing. Speaking to lawmakers on Wednesday, Premier Li Keqiang reiterated the government’s pledge to give the market a bigger role in allocating resources and stressed the need to “guard against and defuse debt risks.”

Since the global financial crisis, China’s debt levels have grown at a clip similar to the U.S., the euro zone and South Korea before those economies fell into deep recession. While few economists forecast such an outcome for China, the country’s debt accumulation could eventually slow growth, analysts say, as occurred in Japan during the 1990s. For all of 2013, the most recent official data available, overall new credit in China rose 9.7% to 17.29 trillion yuan compared with a year earlier.

Many analysts believe that Chinese authorities may allow defaults only on debt that isn’t big enough to cause systemic risks or drag down the broader economy. Chinese leadership, they say, faces the challenge of creating a more market-oriented economy while ensuring stable economic growth.

“The immediate repercussions in the bond market may not be systemic,” said analyst Zhiwei Zhang at Nomura Holdings Inc., speaking of the potential default by Shanghai Chaori. “Nonetheless, we continue to expect more credit defaults” on debt tied to Chinese companies and local governments, he said.

Shanghai Chaori, a midsize solar company, avoided a default a year ago after a local government in Shanghai persuaded its bank to defer claims on overdue bank loans, according to Chaori’s filings. Many analysts don’t expect the government to step in again this time, though the company has said it would try to minimize investors’ losses.

As of the end of June, the last period such data are available, Shanghai Chaori had failed to pay 12 banks almost 1.5 billion yuan of loans on time.

In November, Bank of Tianjin said it was looking for investors to buy more than 52 million yuan of loans and unpaid interest payments it was owed by the company. The bank had already extended the loan once and taken the company to court to get its money back, according to Chaori filings. Bank executives didn’t answer phone calls Wednesday.

Investors first braced for a potential default in 2012. Shandong Helon Co., a maker of chemical fibers, avoided defaulting on 400 million yuan of maturing commercial paper after a local government stepped in.

Chinese solar companies LDK Solar Co. LDK -1.94% and Suntech Power Holdings Inc.STPFQ -3.02%

missed debt payments last year, but those bonds were issued abroad.

March 5, 2014 10:47 am

Investors and economists poised to cheer China bond default

By Josh Noble in Hong Kong and Simon Rabinovitch in Shanghai

It is a rare thing to see investors and economists come together to cheer a bond default, except it seems in China.

On Tuesday, Shanghai Chaori Solar said it would not be able to pay investors the Rmb89.8m ($14.6m) interest payment they are owed on money that the company borrowed two years ago, raising the prospect of the country’s first true corporate bond default.

Analysts think a default in China is both inevitable and most likely imminent. Many hope it will mark a change for the better in the country’s financial markets, helping money flow to deserving companies at the right price.

The belief – repeatedly borne out in practice – that the government always rides to the rescue of troubled borrowers has encouraged investors to lend money at artificially low rates to weak companies. That in turn has fuelled a pile-up of bad investments and a surge in China’s debt levels.

Chaori has not yet missed its March payment, which is due on Friday, meaning it could yet be bailed out as it has been in the past when faced with financing difficulties. The bonds themselves have not traded since July last year.

A high-profile default in the trust sector was narrowly avoided in January, when investors in a product backed by loans to a coal company were rescued just days before maturity. In that instance, investors were given back their principal but lost two-thirds of the interest owed this year.

At the time, all three international rating agencies criticised the authorities for perpetuating the view that investors in China would always be bailed out, no matter how risky their investments.

“A default would definitely be a good thing for the long-term development of the corporate bond market,” said Ivan Chung, a credit officer with Moody’s. “Investors have just been buying the bonds with the highest yields. Pricing does not reflect risk.”

Chinese companies have missed interest payments on bonds before – delinquencies that would be classified as defaults in developed markets – but bailouts have always ultimately been provided by third parties.

The Chinese bond market has boomed in recent years, partly on the back of the country’s 2009 stimulus package. The outstanding volume of corporate debt reached Rmb8.7tn at the end of January – up from Rmb800bn at the end of 2007, according to Bank of America Merrill Lynch.

The potential for a default by Chaori is an indication of the financial stresses that are encumbering Chinese companies after their debt splurge.

Yet onshore investors know they need not worry about a wave of defaults. As much as 80 per cent of corporate debt issued in China comes directly from state-owned enterprises and local government investment companies, and these bonds are still seen as safe.

“It is an isolated case, a small private enterprise in the solar power sector. Even if Chaori defaults it will not create a systemic risk for financial markets or the economy,” Mr Chung said.

David Cui, China strategist at Bank of America Merrill Lynch, points out that the Chaori bond in question is backed by a local government and an underwriter with ample resources to bail out investors. As such, any default would have been deemed a desirable outcome by those involved.

“If the bond is allowed to default, we believe it will most likely be because the government wants to teach the market a lesson and address the implicit guarantee moral hazard issue,” he wrote in a report.

Yields on Chinese corporate bonds have been rising steadily over the past six months, a reflection of increasing wariness among investors about the risks in the credit market but also of tightening liquidity in the Chinese economy.

Jian Chang, China economist at Barclays, said that there are default risks in a number of sectors suffering from overcapacity – such as shipbuilding, steel, property and cement – but that the government would provide support if any threaten to pose systemic risks. “They still have the capacity to take such action,” she wrote in a note.

In the meantime, buyers of the Chaori bond are vowing to put up a fight. A group of investors has filed a lawsuit against Citic Securities, the underwriter of the bond.

“They were dishonest about Chaori’s profitability and should be held liable to repay us,” said Mr An, a retail investor in the eastern province of Shandong.

Citic Securities was not immediately available for comment.