Investment: A better bubble; The current froth in technology stocks is driven by revenue. That does not make it rational

March 5, 2014 7:49 pm

Investment: A better bubble

By James Mackintosh and Lex reporters

The current froth in technology stocks is driven by revenue. That does not make it rational

In the world of technology stocks, it is February 2000 – at least as measured by the Nasdaq Composite, the index preferred by tech investors. A week ago it hit a level topped only during the final month of dotcom insanity before that bubble burst in March 2000.

For sceptics, this is a sign of froth in high-growth shares. Companies such as Facebook, Twitter, Arm Holdings, Tesla and the biotechnology sector are trading at levels that many find hard to comprehend. Facebook paid $19bn for WhatsApp, a price of $345m per employee. The number of highly valued companies – worth more than 20 times expected earnings and more than 10 times both sales and book value – is the highest since the dotcom crash.

No surprise, then, that companies are choosing to cash in. This year had the strongest start for US listings since 2000, according to Jay Ritter, finance professor at the University of Florida. Biotech companies in particular have rushed to take advantage of public demand for speculative stocks, while online retailers are among those floating in Europe. Frequently founders and private equity backers merely wish to sell, with many companies raising little new cash.

There is wide agreement on the explanation: years of weak economies have left investors without the usual sources of growth from the economic cycle, so rising optimism was directed to new technology instead.

“There’s some appetite from investors now to hope and dream rather than focus on the downside risks, and that naturally points them towards technology,” says Mark Haefele, head of investment at UBS Wealth Management.

The hopes are focused in four areas: social media, biotech, online retail/payment and a handful of disruptive hardware technologies, in particular Tesla’s electric cars, Arm’s cheap processors and 3D printing.

All tell solid stories. This, shareholders say, is not a repeat of the dotcom bubble years. Back then, listed companies that simply added .com to their name averaged a 74 per cent gain in 10 days, a post-bubble study showed. Business plans written on table napkins attracted venture investors.

By contrast, today’s companies have real revenues and are growing at the expense of slow-moving incumbents weighed down by old business models. The companies dominating Nasdaq as it approaches its 2000 highs are now mature businesses. Even among the new “story stocks”, many – including Facebook, Arm and the bigger biotechs – are very profitable. Clearly the future of retail is online. Social networks are used by hundreds of millions of people. Biotech is no longer purely promise. The future of the electric cars looks brighter than at any time since the early 20th century.

There was a solid story to tell about every bubble in history, from Dutch tulips in 1634 to the British railway mania of the 1840s, Florida land in the 1920s or the safety provided by portfolio insurance in 1987.

Dotcoms, too, had a tale: the internet has indeed proven to be a disruptive technology. The question is, will today’s stocks reap big enough benefits from the disruption? Or are investors once again overexcited?

The case against is fairly simple. Easy money has encouraged speculation. Emerging markets were the initial beneficiaries; investors and companies even began to rebrand them as “growth markets”. A mini-bubble inflated rare earth stocks fivefold in 2010 (they are now worth half their starting point). Apple and Samsung soared as investors latched on to the smartphone and tablet boom, before dropping back. The new tech stocks are merely the latest fashion.

Your opinion

Are you investing in technology stocks?

No. There is a bubble developing and I am steering clear.Yes. There is a bubble developing so I’m buying them.Yes. There is no bubble developing and prices are justified.No. I have no idea how to value these stocks at all.

VoteView Results

“The market is starving for growth ideas,” says Alain Bokobza, head of global asset allocation at Société Générale. “We are back to where we were in 1996, 1997, where the market’s moved to a new story.”

That does not mean every company will lose out or even that they are all overvalued. Pierre Lagrange, co-founder of London hedge fund GLG, says there is “massive upside” for many of the disruptive stocks, including Facebook, which GLG has owned since it listed. However, he warns that the number of investors chasing themes such as big data mean any company disappointing revenue expectations will suffer badly.

“You have a lot of people interested in big data and you have got relatively few stocks so there’s a rarity factor,” he says. “There’s lazy money in some of those [shares] because it is thematic.”

Many fund managers are ditching traditional valuation tools, instead guesstimating how much of a total market – advertising, pharmaceuticals, cars – a company might grab in a decade, rather than focusing on growth rates or earnings.

As one hedge fund manager put it, if there’s a 10 per cent chance that Tesla could take 10 per cent of the market value of the motor industry, it justifies its current price (Mr Lagrange has doubts about this methodology).

A frequent refrain is that “if [insert favoured company] can grow the way Google did, it is worth far more” than the current share price.

Valuations assume that the new tech stocks will create an awful lot of disruption in traditional companies, that incumbents will fail to fight back effectively, and that yet more start-ups will not disrupt the new business models (as Facebook did to previous social networks). Some of these stocks might be the Google of retail or carmaking; others will be as valuable as a losing lottery ticket.

“Are there going to be people who wake up one day and find that they let their greed trump their fear? Absolutely,” says Mr Haefele.

——————————————-

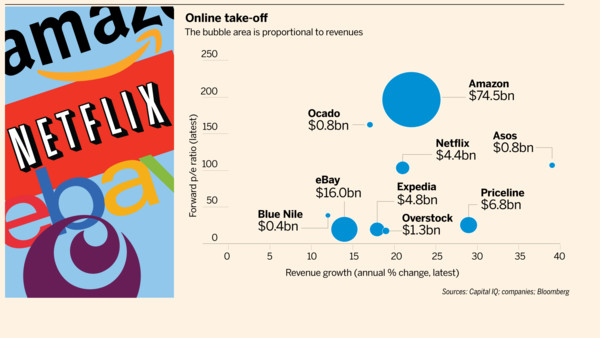

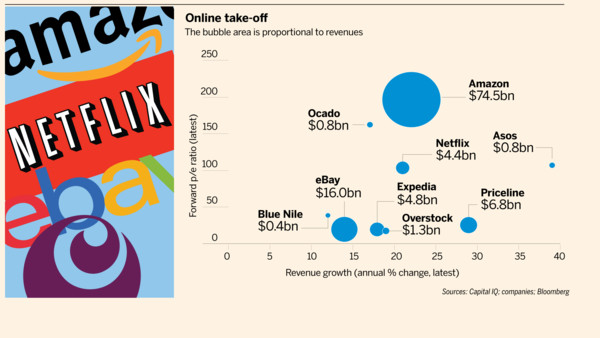

Online: a low-return game

Here’s the case for owning Amazon’s shares at $360, writes Robert Armstrong .

The company’s sales are growing at about 20 per cent a year. If this continues for 10 years it will have revenues of about $460bn (Walmart’s current level – and who denies that Amazon is the next Walmart?).

Now assume that its operating margin goes to 10 per cent, from 1 or 2 per cent now. High for a mass- market retailer, sure, but Amazon has higher-margin businesses, too – cloud computing and all that.

At a 20 per cent tax rate (think Luxembourg, Ireland or Bermuda), 2022 profits are $71 a share. If the valuation is then 20 times earnings, it’s a $1,600 stock. Buy!

Fast and loose? Sure. But a much more rigorous projection is hard to imagine. The crucial variable – what competition in internet retail will do to any one company’s growth and margins – is unknowable.

So stress test the projection: plug in 15 per cent average growth, 7 per cent margin, a 30 per cent tax rate and a multiple of 15. On this view Amazon still doubles its sales twice in the next 10 years and its margin triples – but the stock remains under $500 in ‘22. That’s a bond-like annual return of 3 per cent. Buy something else!

Bulls on Amazon and internet retail generally can point to one segment long penetrated by internet sales: travel. Margins, growth and valuations remain high for the leaders, Expedia and Priceline.

Remember, though, that these companies are exchanges that aggregate supply and demand, and exchanges enjoy powerful network effects. Everyone wants to be on an exchange (or, for that matter, a chat app) that has a lot of people on it already.

So don’t confuse the travel sites with companies that are essentially old-fashioned retail operations – sourcing, selling and distributing physical goods – that happen to have digital storefronts. This group, which includes Ocado, AO World and big parts of Amazon, will compete on price, distribution and selection – a capital-intensive, low-return game.

——————————————-

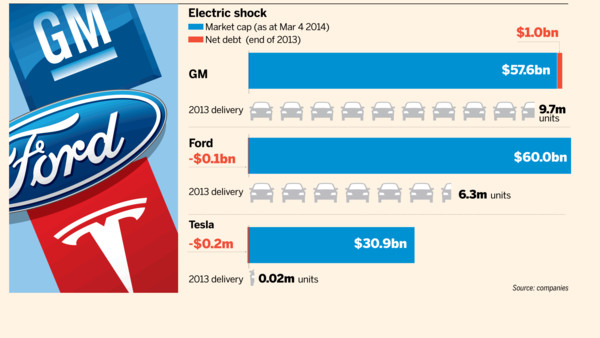

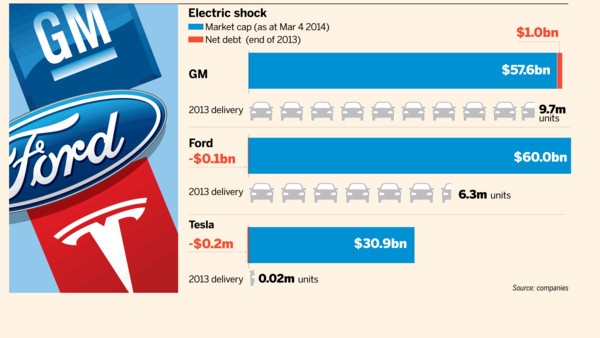

Tesla: A bet on batteries

A company with a $30bn market cap does not get to sell niche products, writes Sujeet Indap . Tesla Motors, after a 600 per cent run-up over the past two years, has been given credit for being a mass-market car company far in advance of moving mass-market volumes.

The company has sold a grand total of 25,000 Model S sedans at $70,000 a pop. By 2020 the electric car revolutionary plans to sell 500,000 units a year – aggressive, but bordering on plausibility.

Audi, BMW and Mercedes together sell almost 6m cars annually. Can Tesla profitably deliver that many vehicles? If so, then its share price still looks pricey but not absurd.

Ramping up production of cutting-edge cars is much trickier than getting a few hundred million people to download an app.

By 2020, Tesla’s “generation III” model will be available and selling at, say, $45,000 each. If 80 per cent of the company’s volume targets are made up of these, with the rest being the plush Model S, Tesla will rake in $25bn in revenue.

At an 11 per cent operating margin (higher than what Ford and General Motors aim for) earnings per share could be $13. Applying a 30 times forward multiple, and then discounting back five years at a 15 per cent discount rate yields a stock price of about $200. This is about where Tesla shares were just before its recent earnings announcement. (Its shares are now $250).

There is a hypothetical combination of price, margin and volume that justifies the share price. But investors are betting on Tesla’s ability to overcome a non-financial hurdle: it must make breakthroughs in battery design and manufacture which bring the unit costs down dramatically while increasing the distance the cars can go on a charge and decreasing the time it takes to charge up. What’s more, it is not enough for this technology to exist: Tesla must own it, or it will suddenly be on a level playing field with much larger competitors. Because Tesla has wisely tapped financing markets as its stock has soared, it won’t be short of capital. It will need it.

——————————————-

Social media: the new, new thing

Go ahead, gramps. Try saying social media is not the future of advertising and watch the reaction from the whippersnappers, writes Nicole Bullock . That #enthusiasm supports high growth expectations. Sales at Facebook rose 55 per cent to nearly $8bn in 2013 from a year ago. And it is wildly profitable: over a third of its revenues converted to free cash flow last year. At Twitter, revenue more than doubled, hitting $665m.

Both increased their share of worldwide digital advertising, too. At $119.5bn for 2013, the market expanded by 15 per cent, according to eMarketer. But what percentage of ad spend do they have to capture to justify the high hopes?

Take Facebook. Looking out to 2017, Wall Street expects Facebook will produce sales of about $23bn and earn $2.86 per share. For both sales and profits that comes to compound annual growth of about 30 per cent. At the current share price of $71, the multiple a few years out is then 25 times – not bad. Assume $20bn of sales comes from advertising. eMarketer forecasts worldwide digital ad spend of $179bn for 2017. Facebook would have to win an 11 per cent share; it has 6 per cent now. This doesn’t seem a stretch for a company with 1.2bn monthly users.

For Twitter, 2017 sales forecasts of $4bn would equal nearly 60 per cent CAGR from 2013 and just 2 per cent of the digital ad market, against 0.5 per cent now. The multiple on expected 2017 earnings is about 50 – toppy, but Twitter is younger than Facebook.

The market is big enough that reasonable market share targets translate to big growth. The tricky bit is what these projections imply about the structure of the market: that a new disruptive competitor is unlikely to emerge quickly, as Twitter and Facebook did themselves.

One might argue that Facebook and Twitter cannot suffer the fate of MySpace. Their huge user bases mean that those who defect for the new new thing risk losing connections. And the companies have the money to buy the next new thing anyway. But if their business models turn out to be based on user inertia and pricey acquisitions, the market will rethink those valuations.

——————————————-

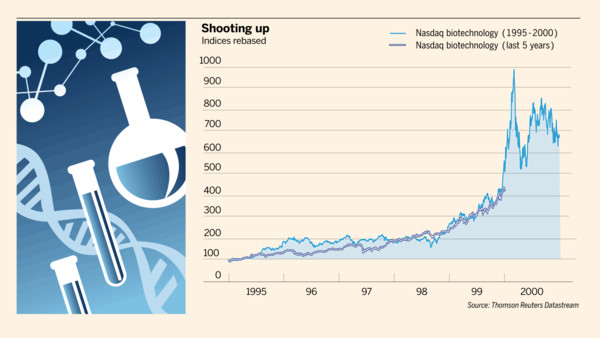

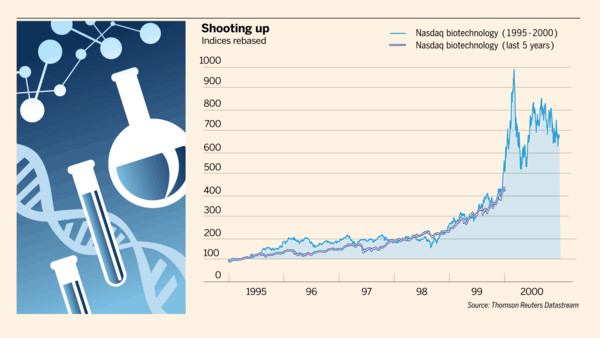

Biotech: real medicine, snake oil prices

Please don’t wake, no don’t shake me. Biotechnology investors are channelling John Lennon as they hope the “dream” stocks at the cross-section of medicine and innovation continue to float upstream, writes Arash Massoudi . In three years, the sector has turned $100 into $284, humbling the $151 the S&P 500 returned. But the alarm is buzzing.

The sector has top-heavy DNA. A handful of large companies – Amgen, Biogen Idec, Celgene and Gilead – have seen their research come good, and amassed an arsenal of cash from a diverse drugs portfolio. Start-up labs, by contrast, are often experimenting with cures to ultra-rare “orphan” diseases. They depend on funding from private investors and venture capitalists that buy scientists time to tinker.

The hope is that good trial results will attract the big boys: Gilead’s $11bn purchase of Pharmasset in 2011 laid the ground for the start-ups’ incredible boom.

These companies are now creating more froth than medicine. Labs yet to begin trials are sizzling out of their test tubes to list their shares. In one case, investors waived important protections on insider share sales. It didn’t matter; the pre-clinical issuer’s shares more than tripled. Valuations for the smaller biotechs cannot be justified by anyone other than a gambling addict hoping they can spot the next Pharmasset.

Sure, management teams have learnt from mistakes that left shattered glass across the industry after the dotcom bubble burst. Regardless, most will still fail. These are stocks for thick-skinned professionals. Generalists should steer clear, but instead are investing willy-nilly; the sector’s main exchange traded fund has seen inflows of $1.4bn over the past three years.

The case for the big four is different, and rests on earnings growth. So far, analysts have been forced to revise estimates higher and higher. Assuming operating profit growth of more than 20 per cent, the four trade at 18 times 2015 earnings and 15 times 2016. That compares pretty fairly with the broader healthcare sector. But the big four’s halo effect on the start-ups makes no sense.

That is why some are hitting snooze.