Are Small Investors a Sell Signal?

March 11, 2014 Leave a comment

Are Small Investors a Sell Signal?

The case for a market top isn’t that clear-cut.

JOE LIGHT

March 7, 2014 1:50 p.m. ET

David Avery used to keep half his 401(k) account in bonds and cash. Last year, the 35-year-old computer programmer moved his entire portfolio into stocks, with one recent purchase being Enanta Pharmaceuticals, ENTA -1.05% a small biotechnology company that posted a loss last quarter.

“I could see it going up maybe 50% at a minimum, just being conservative,” says Mr. Avery, who is the co-founder of an investment club in Augusta, Ga. “If the market does well, I could see it double easily.”

Small investors, well known for poor market timing, are flocking back to stocks. Does that mean it is time to sell?

In 2013, investors put $172 billion into U.S. stock mutual funds and exchange-traded funds, according to fund tracker Lipper. Not accounting for inflation, that was the highest total since at least 1992, the earliest year for which Lipper has data.

The trend worries some strategists, who argue that small investors are notorious for clamoring to buy just before a market top. An analysis of small-investor sentiment shows that the widely held belief is true, but perhaps not reliable enough to warrant any major buying or selling on its own.

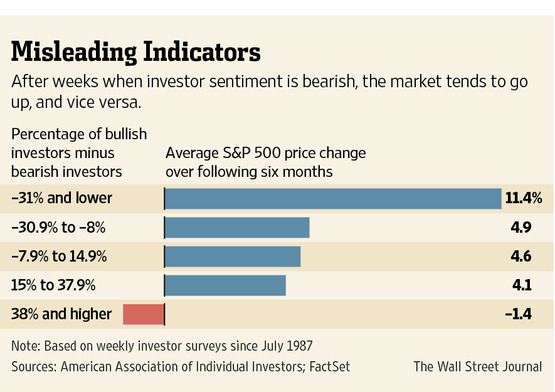

The first challenge is to decide what measure of investor sentiment to look at. One widely used option: the American Association of Individual Investors sentiment survey, which the 170,000-member nonprofit in Chicago has conducted weekly since July 1987. AAII says the survey typically gets responses from a few hundred affluent, hands-on investors.

AAII asks its members whether they think the stock market will rise, fall or stay the same over the following six months. The difference between the percentage of bullish investors and bearish investors is seen as a measure of how small investors feel that week.

For example, in the week ended March 5, 40.5% of investors were bullish while 26.6% were bearish. The net 13.9% bullish reading was higher than the long-term average of 8.5%.

What does that say about the chances of the S&P 500 rising or falling? Not much.

In the 1,362 surveys since July 1987 that are at least six months old, investors correctly guessed the direction of the S&P 500 slightly more than half of the time.

That isn’t good by any means. If small investors always bet that stocks would rise, they would have been right 72% of the time.

But it also probably isn’t strong enough evidence that small investors’ optimism warrants a stampede out of stocks, says Harvard Business School professor Malcolm Baker, who has developed his own sentiment index using other factors.

Though bullishness is a sell signal, Prof. Baker says, “none of these indicators are going to predict the market in a very reliable way.”

The AAII survey works as a better buy or sell signal at extremes.

After weeks when a net 38% or more of AAII members were bullish, the S&P 500 went on to lose 1.4% over the following six months on average. In weeks when a net 31% or more were bearish, stock prices subsequently climbed 11%.

Even then, Prof. Baker says that very bullish sentiment should push an investor only to move his stock allocation five percentage points below normal. So an investor who normally puts 60% of his portfolio in stocks would sell until the allocation reached 55%.

Lately, some researchers have come up with ways to detect specific emotions and how they affect stock moves. Richard Peterson, founder of MarketPsych, analyzes text in news stories, social media and other sources to estimate whether investors feel, say, “joy” or “trust” about specific stocks and sectors.

In particular, Mr. Peterson has found that anger—for example, a series of tweets about the Apple chief executive that say “Tim Cook is an idiot!”—is a better predictor of good returns than general bearishness. In international stocks, future returns are better when investors feel that a country’s government is unstable, he says.

Right now, the sectors that investors are angriest about on social media include Internet companies, industrials and banks, according to MarketPsych. Individual stocks registering angry sentiment include defense company General Dynamics, GD +0.04% tech companyOracle ORCL -1.60% and real-estate developer St. Joe. JOE -1.17%

Investor bullishness also seems to be a stronger sell signal for stocks with speculative attributes, such as those that deliver low profits or don’t pay dividends, Prof. Baker says. “Stocks that are difficult to value are more prone to sentiment,” he says.

When such joy fades, he says, those stocks will be punished the most.