Why investors should stop buying the biggest funds

March 11, 2014 Leave a comment

Why investors should stop buying the biggest funds

Our analysis of peformance shows why investors should look to smaller funds for the best returns, rather than the bigger, more well-known ones

By Richard Evans, Investment Editor

7:47AM GMT 08 Mar 2014

“Past performance is no guide to the future.” How many investors overlook that ubiquitous warning when they think they have identified a brilliant fund manager? But there may be very good – and unappreciated – reasons why they should take heed.

It’s nothing to do with a belief that a fund manager’s performance is down to luck, that no one can maintain exceptional returns over the long term. Rather, it’s because good managers tend to attract more money – and that this very success makes it harder for them to deliver the goods in future.

Put simply, big funds have to buy big companies. And big companies cannot grow as quickly as small ones.

If you want proof that investing gets harder as the amount that you manage grows, look no further than two of the world’s best investors, Neil Woodford and Warren Buffett.

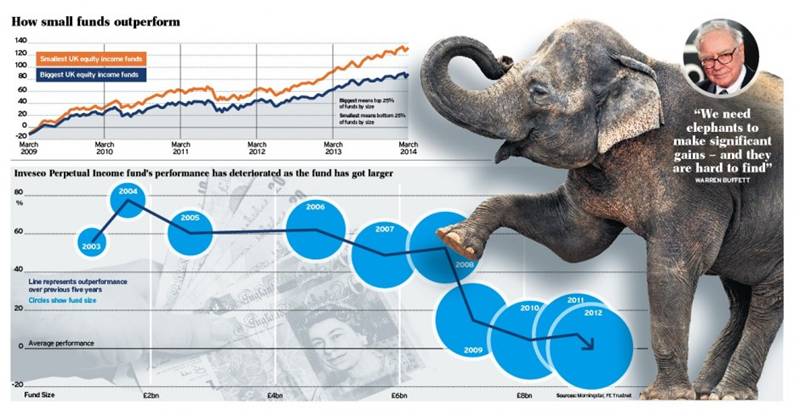

Over the course of his 25 years at the helm of the Invesco Perpetual Higher Income fund, Mr Woodford has produced extraordinary annual returns averaging 13.1pc. But in recent years his performance has started to look rather pedestrian. After outperforming at least three quarters of his peers for five years between 2004 and 2009, he has underperformed them three times in the past four years, according to FE Trustnet, the data company.

Over the past 10 years the amount of money in the fund has ballooned from £2.4bn to £13.6bn. According to the professionals paid to pick funds, the increasing size of Mr Woodford’s fund is the direct cause of its diminished returns.

Mr Buffett, meanwhile, has been saying for years that as his company, Berkshire Hathaway, grows, it becomes harder to produce the gains that investors have become used to. Between 1965-1974 the company – which, with its diverse array of subsidiaries, is in some ways similar to a fund – underperformed the broad US stock market only once. But over the past 10 years this has happened five times.

The “Sage of Omaha” said as long ago as 2002: “In the future we won’t come close to replicating our past record … [In the past] we could often buy businesses and securities at much lower valuations than now prevail; and more important, we were then working with far less money than we now have.”

He explained why it was harder to produce spectacular returns when there was more money to invest: “Some years back, a good $10m idea could do wonders for us. Today, the combination of 10 such ideas and a tripling in the value of each would increase the net worth of Berkshire by only 0.25pc. We need elephants to make significant gains now – and they are hard to find.”

Apart from the fact that even brilliant buys of small companies will not make much difference to a giant fund, there are other reasons why they find things tougher than their smaller rivals. Imagine the manager of a large fund identifies a dramatically undervalued company. For it to make any difference to the fund’s performance, he or she must buy a substantial stake. But this can be easier said than done.

Individual investors see buying shares as a simple matter of telling the broker how many they want at the price stated. For institutional buyers of tens of millions of shares, it’s different. There may simply not be enough sellers around, so building the desired stake could take days – or longer. Meanwhile, other investors could realise that there is a big new buyer in the market and decide to sell only at a higher price.

“A few years ago I realised that Arbuthnot Banking Group was very attractively priced,” said one highly regarded fund manager, who runs a relatively small amount of money. “But it took me a while to buy all the shares I wanted, because they are very tightly held. The manager of a large fund would have had no chance to buy a meaningful stake.”

Whereas there is little point in a big fund buying shares in small companies, there is nothing to stop small funds buying big companies. So small funds have greater flexibility to exploit opportunities of all sizes, potentially giving them an edge.

“I would occasionally buy a FTSE 100 company if the shares were very cheap,” said Mark Slater, who runs the £92m Slater Growth fund.

People who are paid to pick the best funds include “fund of funds” managers – those who allocate clients’ money to baskets of funds, not shares. Many of them prefer smaller, less well known funds.

“We try to buy funds when their managers are creating their track records, not when they are living off them,” said Rob Burdett of F&C’s fund of funds team.

Simon Evan-Cook, one of his counterparts at Premier Asset Management, said: “Buying funds of the right size is a huge part of what we do. When they get too big, we aim to move on to the next generation of top managers.”

How to avoid getting caught in giant funds that have stopped growing

It’s human nature for investors to trust their money to the perceived safety of a successful fund. But if this means buying a big fund, they could miss out on the best returns. The tips below should help guide you to the right choices.

Balancing act

As the main article explains, investing in successful funds that have grown big as a result could mean settling for unspectacular returns. But plumping for a small fund with a shorter track record of outperformance can also be risky.

It’s hard to say exactly when superior returns cease to be a question of luck rather than skill, but Anthony Bolton, the legendary fund manager, suggested at least three years as a rule of thumb.

The other point is that large funds often owe their size to a skilled fund manager. Investors need to weigh this benefit against the degree to which the fund’s size restricts his or her freedom of action. Ideally, find a good manager who runs a smaller fund in preference to an equally skilled manager in charge of a big one.

How big is big?

When should a fund’s size ring alarm bells? It depends on the type of fund, but one that concentrates on small companies could hit problems at several hundred million pounds, whereas a “large cap” fund could comfortably go into the billions. Warning signs are a rise in the number of holdings and a fall in the percentage of the fund accounted for by the biggest holdings.

Go for conviction

One problem for large funds is that it is harder for them to differ markedly from the broader market – they risk becoming “closet trackers”. Only a manager who believes strongly in his investment methods and is prepared to back them through periods of unfashionability can hope to succeed by refusing to follow the herd. It’s vital to understand the manager’s approach and character. Fortunately, there is a wealth of insight into these questions available online at fund managers’ websites, those of independent analysts such as Trustnet and Morningstar and attelegraph.co.uk/investing.

Consider investment trusts

This alternative type of fund does not become bigger through being in demand, because every new investor is matched by one who is selling his or her holding. Investment trusts therefore tend to be smaller than ordinary funds. However, if a fund and an investment trust are run in the same way, constraints on the fund would spill over and affect the trust, too. Well regarded trusts without “mirror” funds include Scottish Mortgage and City of London. Watch out for large “premiums”, however – when the trust’s share price exceeds the value of its assets.

Follow the professionals

“Fund of fund” managers are paid to identify the most promising funds in which they then invest their own portfolio. It is striking how often their holdings avoid the big “household name” funds in favour of less well-known, smaller rivals.

For example, Rob Burdett of F&C favours the River & Mercantile UK Equity Long Term Recovery fund, with £146m in assets, as a “small and nimble” alternative to “quality giants” such as the £6.9bn M&GRecovery fund.

Rather than Invesco Perpetual’s £8.4bn Income fund, investors could consider the £649m Cazenove UK Equity Income fund, he added, while JO Hambro’s £900m Continental European fund was a smaller, nimbler rival to the £2.4bn Fidelity European fund.

Simon Evan-Cook of Premier Asset Management tipped the Prusik Asian Equity Income fund as an alternative to better-known names such as Newton Asian Income. He also backed Charlemagne Magna Emerging Markets Dividend for its “Neil Woodford-style” approach.

“We admire Aberdeen’s Asset Management’s Asia funds, but this one has a fraction of the assets,” he said.