Chinese Firm’s Bond Default May Not Be the Last

March 12, 2014 Leave a comment

Chinese Firm’s Bond Default May Not Be the Last

Some See It as Injecting Some Discipline Into a Swelling Debt Market

LINGLING WEI, DINNY MCMAHON And WAYNE MA

March 9, 2014 3:28 p.m. ET

BEIJING—The first default in China’s corporate-bond market is unlikely to be the last.

The failure by a distressed Chinese solar-equipment maker to make a bond-interest payment on Friday signals Beijing’s willingness, however tentative, to let some weak companies fall—a move that analysts and investors said could inject some discipline into a swelling debt market long viewed as implicitly supported by the government.

At the same time, the default by Shanghai Chaori Solar Energy Science & Technology Co. also adds to worries over mounting risks in the country’s financial system.

“It’s just like when you find a dead roach in your kitchen. You would know there must be more to come,” said Huang Cendong, an analyst at Sinolink Securities Co., a Chinese brokerage firm.

Shanghai Chaori failed to pay 89.8 million yuan ($14.7 million) in interest on a one billion yuan bond sold two years ago. If relatively small, the amount is part of a mountain of hundreds of billions of dollars that businesses and local governments borrowed during a credit binge that started in late 2008 and falls due this year.

With China’s slowing economy testing a 15-year low in year-over-year growth, concerns about companies’ abilities to repay are rising. A director at the China Securities Regulatory Commission said the regulator “will keep an eye on potential regional and systemic risks” in the wake of Shanghai Chaori’s default.

Some analysts and investors welcomed the default, saying it is a sign that Chinese authorities are beginning to chasten companies and investors after years of bailouts and arranged fixes for financially unviable borrowers.

“It’s a good start,” said Zhang Zili, a managing director at Harvest Fund Management, a Chinese mutual-fund company that manages more than $35 billion. “Unlike a bank failure, which could really freeze up the market, this default is a small test case that could make investors more cautious when buying bonds,” Mr. Zhang said.

After Shanghai Chaori disclosed early last week that it wouldn’t make the interest payment, the yield on five-year AA-minus notes, China’s equivalent of junk bonds, rose 0.05 percentage point to 7.89% on Thursday, the highest level since late last month, according to the most recent information available on ChinaBond, a government website that tracks China’s bond market. Bond yields rise as prices fall.

“If China wants to develop its domestic financial system beyond a bank-dominated framework, then bond defaults have to be possible,” said Brian Coulton, an emerging-market strategist at London-based Legal & General Investment Management, which has more than $700 billion in assets under management. But “the change can cause some volatility and disruption in the near term.”

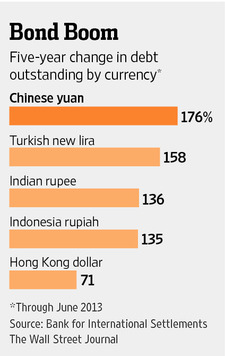

Borrowing by Chinese companies has risen faster than China’s economy has expanded over the past five years. J.P. Morgan Chase & Co. estimates that overall corporate debt jumped to 124% of China’s gross domestic product in 2012 from 92% in 2008. That exceeds the 81% for the U.S. and is far higher than the 40% to 70% of other emerging economies, according to J.P. Morgan Chase.

While banks remain the most important source of funding for companies and local governments, an increasing share of credit comes from the bond market and so-called shadow lenders—trust companies, leasing firms, pawnbrokers and other loosely regulated nonbank lenders.

Shanghai Chaori is a symbol of China’s growing debt troubles. The midsize maker of solar cells and panels has continued to borrow in recent years even as overcapacity swamped the industry and the company’s losses grew. It booked a loss of about 1.4 billion yuan in 2012, the year it sold the one billion yuan, five-year bond with a variable annual interest rate starting at 8.98%.

In addition to tapping the bond market, company founder Ni Kailu also turned to trust companies. From March 2011 to November 2012, company filings show that Mr. Ni and his daughter, who together owned 44% of the company’s shares, began pledging their shares to a number of trust companies in exchange for funds. The pair kept borrowing money from those companies to pay off existing loans, the filings show. By November 2012, they had pledged all their shares. The company later said it started to experience “serious liquidity problems” at the end of 2012.

Mr. Ni and his daughter couldn’t be reached for comment. Liu Tielong, the company’s board secretary, said Shanghai Chaori plans to pay just four million yuan in interest owed on the bond. “We’ll try our best to pay bondholders as soon as possible but the company also has other debts,” he said.

Zhang Kouzhen, a 73-year-old Shanghai resident, and her husband are among the investors who bought the Chaori bond in 2012, according to Ms. Zhang’s daughter, Shen Wenjie.

Ms. Shen said her parents used to invest in stocks but moved their money into bonds a few years ago because it was a better option for retirees. “The bond was rated AA. AA bonds are supposed to be relatively good, right?” Ms. Shen said. “There was definitely no risk.”

Penyuan Credit Rating Co. originally rated the Shanghai Chaori bond as AA but downgraded it to BBB+ last April. It declined to comment.

Shanghai Chaori avoided a default a year ago after a district government in Shanghai persuaded its bank to defer claims on overdue bank loans, according to the company’s filings. At the end of June, the last period for which such data are available, Shanghai Chaori had failed to pay 12 banks almost 1.5 billion yuan in loans on time.

Beyond Shanghai Chaori, a total of 2.7 trillion yuan worth of corporate bonds and 1.2 trillion yuan worth of high-interest loans extended through trust companies are scheduled to mature this year, according to analysts at Macquarie Capital Securities Ltd.