Stock caution urged as margin debt levels hit new highs; P/E valuations, record highs flash warnings; stock pickers look for quality, value

March 12, 2014 Leave a comment

March 9, 2014, 3:00 p.m. EDT

Stock caution urged as margin debt levels hit new highs

P/E valuations, record highs flash warnings; stock pickers look for quality, value

By Wallace Witkowski, MarketWatch

SAN FRANCISCO (MarketWatch) — A number of warning signals are flashing in the stock market, and while not indicative of an imminent crash, they’re telling investors to exercise caution, say market strategists.

Stocks finished higher last week, ending on a choppy Friday highlighted by the release of a better-than-expected job report. The Dow Jones Industrial Average (DJI:DJIA) advanced 0.8%, the S&P 500 Index (SNC:SPX) rose 1% to close at another record high of 1,878.04, and the Nasdaq Composite Index (NASDAQ:COMP) finished up 0.7% for the week. All except the Dow are higher for the year, which is still down 0.8% in 2014.

The gains haven’t come without a share of fretting that the good times can’t last. Among the warnings signs: The indexes’ string of record highs; high levels of margin debt, or borrowings to finance stock buys; the slim number of prior bull markets that have lasted past this point; and valuations that are close to levels when stocks last peaked.

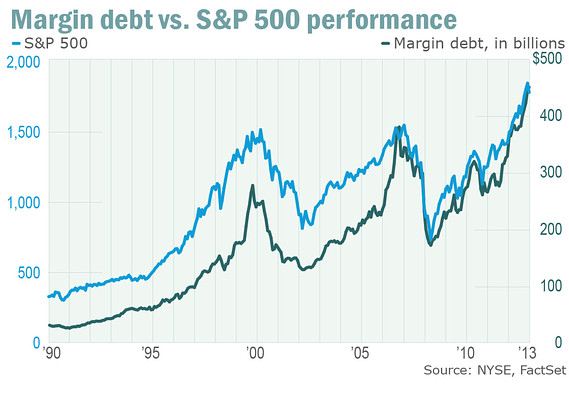

Margin debt, which tends to spike alongside stock rallies and pullbacks, has beenrattling investors for months . “As that debt goes up, the market’s foundation gets shakier and shakier,” said Brad McMillan, chief investment officer for Commonwealth Financial. “The correction could be deeper.”

Also of concern is the bull market’s fifth birthday on Monday. The average bull market only lasts about 4.5 years, putting the current one in rarefied territory. Of the 12 bull markets since World War II, only half have lasted five years, and only three have made it to their sixth birthday.

Speculation about bubbles returned last week. Technical analysts pointed to a possible bubble formation in biotech stocks . Dallas Federal Reserve President Richard Fisher raised concern about “eye-popping levels” of some stock metrics like margin debt.

Valuations, or the prices of stocks compared to the companies’ underlying earnings, have passed levels last reached in 2007, or the top of the last bull market. Bull markets tend to expire when trailing 12-month P/E ratios get into 17x or 18x territory, says LPL Financial’s Jeff Kleintop. They’re approaching 18x now.

Caution, for some strategists, means buying stocks selectively. But there are others who note the market is still moving on broad swings in sentiment, just as it did during the post -2009 recovery from the bottom. That tendency lumps quality and risky stocks together, throwing careful selection out the window.

“This is still very much a risk-on, risk-off market,” McMillan said. “We saw that with Ukraine.”

Last week, both the Dow and the S&P 500 dropped nearly 1% on March 3 after Russian troops assembled near Ukraine’s border, only for stocks to bounce back about 1.5% after Russian President Vladimir Putin pulled them back the next day.

Read: Stock investors look past jobs report to Yellen, Ukraine

Margin debt spike: Canary in the coal mine?

What is troubling is that much of the buying is being fueled by cheap debt, McMillan said. While no formal definition of a “bubble” exists, McMillan said he sees a bubble as a price jump in an asset given the availability of cheap financing.

Margin debt hit record levels at the end of January, according to New York Stock Exchange data. Margin debt at the end of January reached $451.3 billion, its fifth record month in a row. Margin debt returned and surpassed record levels set in July 2007 back in April when it topped $384.37 billion.

“We must monitor these indicators very carefully so as to ensure that the ghost of ‘irrational exuberance’ does not haunt us again,” Dallas Fed’s Fisher said in a speech last week, referring to margin debt and indicators such as price-to-projected forward earnings.

Currently, the 10-year Treasury (ICAPSD:10_YEAR) note is yielding about 2.8%. In comparison, in past instances when margin debt spiked, borrowing was much more expensive, with the 10-year yielding about 4.5% in 2007, and about 6.5% in 2000.

Those elevated margin levels may exist precisely because debt is so cheap and will remain so until the Federal Reserve decides to start raising rates, an event not expected until at least 2015.

And this stock market, notwithstanding an 177% bounce off its 2009 lows, remains the bull market everyone loves to hate. While investors are more receptive to stocks now, investors don’t seem that euphoric, said Mark Luschini, chief investment strategist at Janney Montgomery Scott.

That view of weak investor sentiment is also backed by figures from Bank of America Merrill Lynch. In a recent note, Savita Subramanian, B. of A.’s equity and quant strategist, said investor bullishness was unchanged in February, signalling a buy, with strategists recommending an average weight of 54% in equities, well below the benchmark weighting of 60% to 65%.

It’s best to stay cautious at this point with full valuations and more expected “pain trade” volatility on the horizon, said Luschini said, who believes the current market is suited for stock pickers.

Tech stocks likely best positioned

Sectors Luschini likes the best are cyclicals, namely, techs that are likely to benefit from increased capital expenditure spending, industrials, energy, and financials. Techs are about the cheapest of the bunch right now, he said, citing software and cloud-based companies like Microsoft Corp.(NASDAQ:MSFT) and EMC Corp. (NYSE:EMC)

Another reason to favor the cyclicals are that they will likely benefit the most from a long-overdue capital expenditure replacement cycle that has been delayed by a lack of visibility about economic conditions and political dysfunction in Washington D.C. over the past 18 months, Luschini said.

That reluctance to spend may be coming to a thaw given that CEO confidence improved in the fourth quarter, according to Confidence Board data released in January.

Contrary to popular belief, capital expenditure spending is already ramping up, according to a recent note from Tobias Levkovich, chief U.S. equity strategist at Citi Research.

A review of 725 publicly traded companies, excluding financial ones, showed planned 2014 capex growth of 5%, compared with expected 1.5% growth when data was examined before fourth-quarter earnings season, Levkovich said.

Another reason to hold onto tech companies is that they’re sitting on about a third of the $1.5 trillion in cash held by U.S. companies excluding financials, with health care companies holding about 16% and industrials accounting for about 15% of it, according to a recent Morgan Stanley note.

Economic data, earnings on tap

Economic data this week include February retail sales data on Wednesday along with March consumer sentiment data and the producer price index on Friday. Also, on Tuesday, the NFIB February small-business index will be released along with January wholesale inventories.

No one single data point will likely move markets this week, however, Janney’s Luschini said. Investors are more closely anticipating the Federal Open Market Committee meeting on March 18 and 19.

With earnings season virtually over, a few stragglers will report quarterly results this week including Urban Outfitters Inc. (NASDAQ:URBN) , American Eagle Outfitters Inc. (NYSE:AEO) , Dick’s Sporting Goods Inc. (NYSE:DKS) , Williams-Sonoma Inc. (NYSE:WSM) , Aeropostale Inc. (NYSE:ARO) , Dollar General Corp. (NYSE:DG) , SeaWorld Entertainment Inc. (NYSE:SEAS) , and Ann Inc. (NYSE:ANN)