African banks: Fragile dream; An institution created to embody stability and unity came close to failure. A new chief could provide a second chance

March 16, 2014 Leave a comment

March 12, 2014 6:40 pm

African banks: Fragile dream

By William Wallis

An institution created to embody stability and unity came close to failure. A new chief could provide a second chance

For nine months, Ecobank Transnational Incorporated was creeping towards disaster. Depositors were taking fright. The stock price was dipping. A stream of internal letters warned the bank and the decades-old dream of building a pan-African rival to Barclays or Citibank was at risk of collapse.

When the bank’s board met on Tuesday, directors were swift and unanimous in removing Thierry Tanoh, the chief executive at the centre of the crisis, ending months of paralysis. This time neither political intervention from Ivory Coast, Mr Tanoh’s home country, nor an order from a Togolese court could save him.

The damage wrought to one of Africa’s best-known brands provides a cautionary tale of the volatility of business on the continent even as much of the investment world is focused on its emergence. With regulators, shareholders and now the board behind a comprehensive overhaul, Ecobank appears to have taken an important step towards regaining stability.

“We have faced challenges at the governance level in the recent past but they are not insurmountable. We have put in place a detailed governance action plan that will strengthen us to meet these challenges,” said Albert Essien, the understated interim chief executive. Appointed on Tuesday, he has worked for 20 years at the bank and is considered a safe pair of hands for the forthcoming transition.

For years, Ecobank appeared emblematic of a dynamic new class of business rising to the opportunity of growth in Africa. In recent weeks, some African investors feared it could fail, sending shockwaves across the continent.

As Dan Majtila, chief investment officer at South Africa’s $150bn Public Investment Corporation, Ecobank’s largest shareholder, warned in a letter to the board last month calling for the dismissal of the CEO: “If we don’t take this drastic step, we may not have a bank in the near future. That would be the death of a pan-African dream . . . and the Africa growth story will be under serious threat.”

The board’s moves this week allayed those fears. But allegations of mismanagement, highly charged audits, board paralysis and a mutiny of directors have shaken the lender.

Underlying the turmoil was a battle not just over management but also ownership. Underperforming but with an unparalleled footprint across a continent perceived among investors as the last frontier, Ecobank has become an alluring target – the kind financial predators dream of taking over in search of sharp returns.

Stephen Jennings, the bullish former chief executive of Russia’s Renaissance Capital, tried and failed. South Africa’s Nedbank has options this year to convert debt and buy equity up to 20 per cent. There are others now circling in the region in search of prey.

Conversely, Ecobank’s problems have proved a critical test for regulators struggling to develop effective cross-border supervision. Officials in Nigeria, where Ecobank is a top five bank, have been acutely aware of how the crisis at the holding company, which falls outside their regulatory purview, could by association undermine confidence in a broader banking sector recovery.

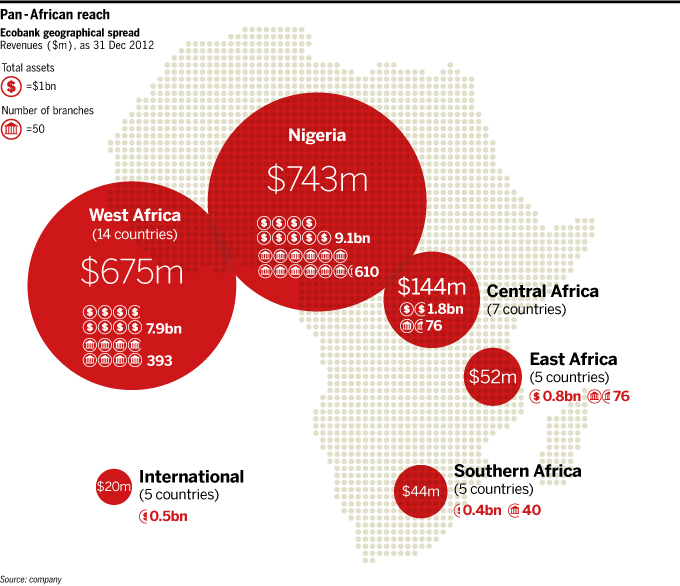

They have also worried about the risk that a run on the Nigerian subsidiary would pose elsewhere as it represents 40 per cent of a business spread across 35 African countries. “If Ecobank has a problem, too many bank systems in Africa will have one, too,” says a senior Nigerian official.

Ecobank’s pioneering shareholders were rallied from across west Africa by a group of well-connected business people who straddled the anglophone-francophone divide. When they came together in 1985, their ambition was to create something more than a bank. They were intent on breaking down the linguistic and bureaucratic barriers that had fragmented markets and hindered development since European colonisers carved up the continent.

“The vision of the bank was let’s create something that will unite people and can show that Africans are not always bickering: that they can set out a high goal and work towards it,” said Kolapo Lawson, former chairman.

The road the group has travelled since has been strewn with bumps, some laid by the French. They saw Ecobank’s ambitions as a threat in former colonies where their banks still dominated. Using independence-era agreements, they complicated Ecobank’s creation, forcing the founders to open a holding company headquartered in Togo rather than a transnational bank. The complex relationship between Ecobank and its country subsidiaries slowed its evolution.

“Against that French opposition it was a tremendous success,” said Philip Asiodu, a former chairman from Nigeria.

There were early near crashes, mostly reflecting the difficulties of raising capital and generating profits when African economies were still dominated by the state and currencies were in freefall.

But the bank survived in part because of the dedication of staff and shareholders to its mission – a commercial approach to the ideal of African unity that Kwame Nkrumah, Ghana’s independence leader, had championed. The lead role of the private sector spared Ecobank the problems of state-owned regional projects, not least Air Afrique, the airline that crashed in 2001 in a sea of debt.

On the back of booming demand for services and strong investor interest, Ecobank has become over the past decade one of the few genuinely pan-African companies of scale.

“We took a near bankrupt bank with a $500m balance sheet operating in five countries and with no profits to speak of and turned it into the leading pan-African bank with $20bn in assets, 1,200 branches and pre-tax profits of over $380m,” said Arnold Ekpe, chief executive for 12 of the past 18 years.

Some of the problems the group is experiencing are the result of that rapid expansion and the challenges of managing the transition from its club-like early ownership to today’s complex shareholdings across multiple markets. Ecobank is now listed in Abidjan, Accra and Lagos. It has tens of thousands of retail owners as well as big institutional shareholders from Africa, Europe and beyond.

Detractors of the ousted chief executive say the governance crisis served as a reminder of how quickly progress can unravel when institutions fall into the wrong hands.

Mr Tanoh was hired from International Finance Corporation, where he was vice-president in charge of Africa, Latin America and Europe.

Although he presided at the IFC over a significant increase in investment in Africa – including in Ecobank – his tenure had its “own challenges”, in the institution-speak of the organisation, according to a former colleague. Ecobank is one of the IFC’s largest investments in Africa.

Soon after his appointment as chief executive in January 2013, he became embroiled in conflict with Laurence do Rego, the executive director in charge of risk and finance from Benin. She had a reputation as a careful administrator.

Last August, she accused the chief executive of conspiring with Mr Lawson, then the chairman, to amend his contract and increase his bonus by 400 per cent without board approval; of pressing her to collude in writing off longstanding debt owed by a family company of the chairman; and of planning to flip bank assets cheaply to a former board member.

In a letter to Nigeria’s Securities and Exchange Commission, Mrs do Rego also accused the chief executive of attempting to boost his first full-year results. People familiar with the matter said this involved an alleged attempt to move a $70m item of income from 2012 to 2013.

Mr Lawson paid back debts. Mr Tanoh announced he would forego the $1.14m bonus. Allies of Mrs do Rego, who was suspended and then fired, contend her actions saved the bank tens of millions of dollars.

. . .

Mr Tanoh portrayed her as a bitter, underqualified employee who lashed out only when faced with the sack. The two men denied all wrongdoing, telling the Financial Times last year it would involve an implausible conspiracy involving multiple players to pull off the alleged mismanagement she had implied. Mr Lawson was nevertheless asked to resign as chairman. Mr Tanoh however, clung tenaciously to his post in the face of a mounting petition for him to go.

Armed with a sweeping order from a Togolese court purportedly protecting a minority shareholder’s rights, Mr Tanoh prevented the board from forcing him out two weeks ago.

Senior managers at the bank say they were unable to find the petitioner’s name on the bank’s register. Gervais Koffi Djondo, the Togolese co-founder of the bank, called her a “phantom”. It was the final straw that brought unanimity to the board, say those familiar with the matter.

The drama had begun to mirror the bigger governance crisis in Nigeria, where the central bank governor has been suspended after exposing a multibillion-dollar hole in the oil accounts. After the injunction, a senior manager commented gloomily that circumstances at the bank were looking more like those in Mr Tanoh’s home country in 2011. Then the loser of an election, Laurent Gbagbo, refused to concede defeat and Ivory Coast descended into civil war.

Mr Tanoh’s camp struck back at detractors, arguing that the many petitions against him were designed to divert attention from alleged malfeasance predating his tenure. He and Mr Lawson claimed the bank’s real challenge lay with legacy issues of financial engineering during Nigeria’s 2009 banking crash.

They also contend that Ecobank has become a football in a larger geopolitical game. This view has support among some west African politicians wary of the creeping commercial dominance of South Africa on their turf.

“West African heads of state are emotionally attached to Ecobank. They think the South Africans have taken over everything. You can’t blame them for feeling crowded out,” a senior Nigerian official said.

But PIC is a portfolio investor and says it has no intention of mounting a takeover. Nedbank is still weighing whether to convert its debt to stock. Mr Ekpe, Ecobank’s Nigerian former chief executive, dismisses talk of a South African takeover, pointing to strong clauses introduced during his tenure to protect the independence of the group. He also defends the South African involvement: “Firstly, it has enabled us to grow Ecobank into the largest banking group in middle Africa and, secondly, it is a model of intra-African co-operation where African institutions are supporting the growth of other African companies.”

For some time these overlapping disputes revealed the opposite of what the bank’s founders hoped. Instead of pulling together towards a higher goal, the bank’s diverse African stakeholders appeared driven by personal and regional rivalry on a race towards the bottom.

A brighter denouement is now in sight. Although the bank has been shaken, senior managers argue that its fundamentals remain robust. “We Africans have this tendency of sweeping problems under the carpet. The best thing is that all this has triggered serious internal talks on the real issues,” says one manager.

“Ecobank will come out of this with strong governance structures and new management. I think the story will continue to sell well.”

——————————————-

Whistleblower: Rare victory for a tenacious accountant

Whistleblowers tend to get a rough ride on the African continent. So the reinstatement of Laurence do Rego as Ecobank Transnational’s executive director in charge of risk and finance marks a rare victory for their cause.

Arunma Oteh, head of Nigeria’s Securities and Exchange Commission which has been investigating Ms Do Rego’s allegations of mismanagement, ordered the bank to reinstate her in January, citing whistleblower protection laws. Thierry Tanoh, chief executive until this week, resisted.

A significant precedent has been set with the Ecobank board’s decision to remove him and reinstate the woman who provided the greatest detail on the problems at the pan-African lender. An accountant from Benin, who in 2010 won an African businesswoman of the year award from the Commonwealth Business Council, Ms Do Rego gained a reputation as a meticulous housekeeper during a decade at the bank.

Some of Ecobank’s leading shareholders, including South Africa’s Public Investment Corporation, have also backed her strongly, recognising the role she played in achieving conformity with international financial reporting standards as the bank expanded.

“It is this reputation that kept Ecobank largely unscathed by the financial scandals which have overtaken some of its rivals,” said Richard Uku, a Commonwealth spokesman and former Ecobank employee, after she was suspended last July. Mr Tanoh fired her in January after questioning her competency and claiming she had lied about her qualifications – a charge denied by her and former colleagues.

According to colleagues, she declined a golden parachute designed to cushion a quiet departure. She stuck tenaciously to her story that she was forced out for resisting instructions against the interest of the bank and its shareholders.

Nevertheless, it would have taken a hardy gambler to wager that Ms Do Rego would eventually come out on top in the protracted battle over how Ecobank is run.