Japan’s pension giant: Risk on; The world’s largest pension fund is changing the way it invests, with big consequences for the market

March 20, 2014 Leave a comment

Japan’s pension giant: Risk on; The world’s largest pension fund is changing the way it invests, with big consequences for the market

Mar 15th 2014 | TOKYO | From the print edition

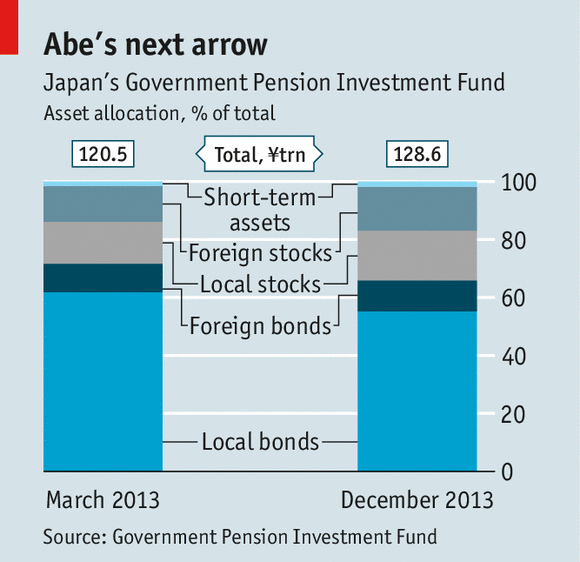

WHEN George Soros, a billionaire investor, met Shinzo Abe, the prime minister of Japan, at Davos in January, he hectored him about asset management. Japan’s massive public pension fund needed to take more risk, he reportedly told Mr Abe. With ¥128.6 trillion ($1.25 trillion) of assets, the Government Pension Investment Fund (GPIF) is the world’s biggest public-sector investor, outgunning both foreign rivals and Arab sovereign-wealth funds. Yet its mountain of money is run by risk-averse bureaucrats using an investment strategy not much more adventurous than stuffing bundles of yen under a futon. It keeps around two-thirds of assets in bonds, mostly of the local variety. Like an investing novice, it mostly follows indices passively, and hardly ventures abroad.

The government would dearly love to oblige Mr Soros. Mr Abe is now taking steps to overhaul the fund. In November last year an official panel laid out a plan of far-reaching reform, some of which could take effect as soon as this year. To boost returns to future pensioners, it concluded, the GPIF should reduce its reliance on bonds, head into stocks and also invest in different asset classes including infrastructure and venture capital.

Most radically, the government wants to break the ties that bind the GPIF to the Ministry of Health, Labour and Welfare. It is the ministry’s cautious bureaucrats that keep the fund so averse to risk-taking. Even with a low return, of an annualised 1.54% over the past 12 years, the GPIF has met its own targets cheaply. The ministry is frugal to the point of meanness. The fund’s 80-strong staff are often unable to buy the market data they need. It is one thing to keep costs low, quite another to forgo receptionists, as the GPIF does at its non-descript office in Tokyo.

For Mr Abe, geeing up the fund is part of his plan to revive Japan’s economy, alongside a radical monetary easing which the Bank of Japan began in earnest in April 2013. As well as defeating deflation, Mr Abe seeks to boost risk-taking in the economy. The planned changes to the fund also include demanding better corporate governance from Japan’s large companies.

Already, the markets are anticipating the effect of the slow shift in direction. GPIF’s influence is amplified by other public pension investors following its lead. The fund lowered the weight of Japanese government bonds (JGBs) from 62% in its portfolio in March 2013 to 55% at the close of the year, putting most of the money—roughly ¥8 trillion—into local and foreign shares instead (see chart). The GPIF’s shift may have contributed to the giddy rise of Japan’s stockmarket, which was one of the best-performing rich-country bourses in 2013. For investors, the likelihood that the GPIF will continue shifting towards equities is a convincing reason to buy Japanese shares. That in turn reinforces Mr Abe’s will to enact the reform. So far this year the Nikkei’s rise, an important contributor to the government’s broad popularity, has stalled.

But for every equity punter cheering on the reform, there is a JGB holder fretful about the eventual impact on prices if the asset class’s biggest backer continues to sell off. Investors have long predicted a meltdown in the Japanese bond market, given that its public debt stands at nearly 240% of GDP. One explanation of why the cost of borrowing for the government has remained low is that JGBs are chiefly held by loyal local banks and by public pension funds, rather than by foreigners who would demand a higher risk premium. Yet the landscape is changing as retirees draw down their savings, meaning that institutional holders will become still more important. Ominously, Japan’s current account has moved into deficit.

For the time being, the monetary easing undertaken by the Bank of Japan will more than offset the effect of any bond sales by the GPIF. So now is exactly the right moment for the fund to sell with no fear of triggering a broader sell-off, argues Takatoshi Ito, the chairman of the government-backed panel on the GPIF.

Yet though the fund may at last escape its duty of holding oodles of government debt, the shift could exacerbate problems once the central bank starts eventually to withdraw from its “quantitative easing”. The partial withdrawal of the GPIF from the market, says Naka Matsuzawa, chief strategist at Nomura Securities in Tokyo, may contribute to a crisis later on. When in December Mr Ito called for a radical cut in the GPIF’s bond portfolio from 55% down to 35%, yields on JGBs temporarily rose.

The basic arguments for overhauling the fund are persuasive. With an ageing population, meaning the fund is already paying out more in benefits than it receives in contributions, it can ill afford to settle for a low-risk, low-returns approach. Its strategy stands in contrast to pension pots in Canada and Australia, for example, which are given leeway to be more daring. They also regularly badger managers of the firms whose shares they own. Obliging the GPIF to insist on more active oversight of firms would be the most useful way to improve Japan’s corporate governance, says Hans-Christoph Hirt of Hermes, a British fund manager.

For now the GPIF and the ministry are together resisting Mr Abe’s initiative. The GPIF’s purpose is not to lift the stockmarket but to invest the people’s money in a safe and efficient way, complained its president, Takahiro Mitani, in February. The GPIF will probably seek to reduce its bond portfolio by as little as it can. The labour ministry’s bureaucrats are understandably loth to forgo the prestige of managing the planet’s single-largest pot of money. Yet the government is determined to overcome opposition, say insiders. Mr Soros, who reportedly made a cool $1 billion by shorting the yen in 2013, may soon be called in to offer further lessons.