Looming property default in China raises fears of broader crisis; Nomura said the number of ghost towns has spread beyond the well-known disaster stories of Ordos and Wenzhou to at least eight other sites

March 24, 2014 Leave a comment

Looming property default in China raises fears of broader crisis

Nomura said the number of ghost towns has spread beyond the well-known disaster stories of Ordos and Wenzhou to at least eight other sites

6:51PM GMT 17 Mar 2014

China faces the biggest property default on record as credit curbs threaten to break the housing boom, leaving a string of “ghost towns” across the country.

The Chinese newspaper Economic Daily News said Xingrun Properties, in the coastal city of Ningbo, is on the brink of collapse with debts of $570m, mostly owed to banks. The local government has set up a working group to contain the crisis.

“As far as we know, this is the largest property developer in recent years at risk of bankruptcy,” said Zhiwei Zhang, from Nomura.

“We believe that a sharp property market correction could lead to a systemic crisis in China, and is the biggest risk China faces in 2014. The risk is particularly high in third and fourth-tier cities, which accounted for 67pc of housing under construction in 2013,” he said.

Nomura said the number of ghost towns has spread beyond the well-known disaster stories of Ordos and Wenzhou to at least eight other sites. Three developers have abandoned half-built projects in the 2.5m-strong city of Yingkou, on the Liaodong peninsular. They have fled the area, a pattern replicated in Jizhou and Tongchuan.

Yu Xuejun, the Jiangsu banking regulator, said developers are running out of cash. This risks undermining land sales needed to fund local government entities. “Credit defaults will definitely happen. It’s just a matter of timing, scale and how big the impact is,” he said.

Land sales and property taxes provided 39pc of the Chinese government’s total tax revenue last year, higher than in Ireland when such “fair-weather” taxes during the boom masked the rot in public finances.

Li Kashing, Hong Kong’s top developer and Asia’s richest man, has been selling his property holdings in China, including the Duhui Palace in Guangzhou and the Oriental Financial Centre in Shanghai.

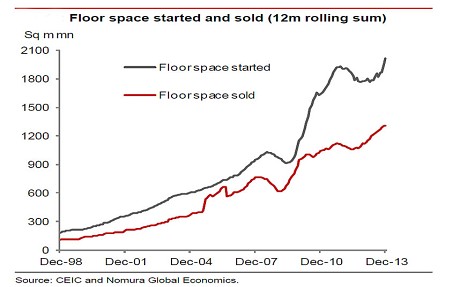

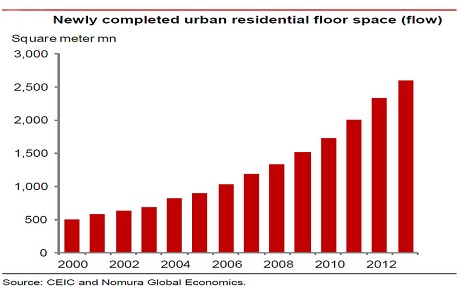

Nomura said residential construction has jumped fivefold from 497m square metres in new floor space to 2.596bn last year. Floor space per capita has reached 30 square metres, surpassing the level in Japan in 1988 just before the Tokyo market collapsed.

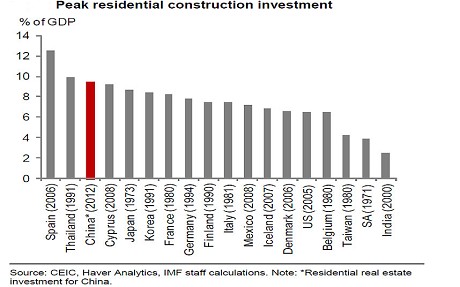

A new study by the International Monetary Fund said the ratio of residential investment to GDP reached 9.5pc in 2012, higher than the peaks in Japan and Korea, and much higher than in the US during the subprime bubble. It also warned that China is running a budget deficit of 10pc of GDP, once the land sales are stripped out, and has “considerably less” fiscal leeway than assumed.

There have long been warnings of a property bust in China. These reached fever-pitch in mid-2012 when a bout of monetary tightening caused house prices to fall briefly.

Prices have since roared back in the tier 1 cites such as Shanghai and Beijing but while these places capture the headlines, they account for just 5pc of total building in China. Prices are falling in 43pc of the tier 3 and 4 cities.

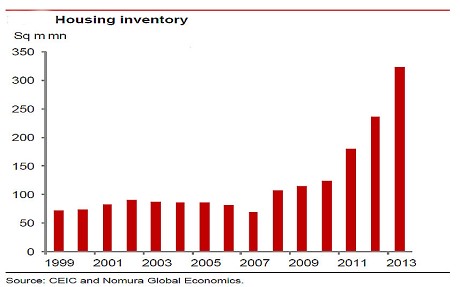

Unsold housing stock in China

Optimists hope that the country’s urbanisation drive will stoke demand for years to come, but this too is in doubt. China’s workforce contracted by 3.45m in 2012 and another 2.27m in 2013 as the demographic crisis began to bite. The number of fresh rural migrants to the cities each year has already halved from 12.5m to 6.3m since 2010. Nomura said there could be net outflows by 2016.

The mounting stress in the property sector is a test of President Xi Jinping’s vow to impose market discipline, however painful. Beijing allowed the solar group Chaori to default earlier this month, the first failure on China’s domestic bond market.

The authorities are trying to wean the economy off excess credit after a $16 trillion spike in loans since 2009 – equal in size to the entire US banking system – but lending curbs are beginning to expose the sheer scale of bad debt in the system.

“It will not be an easy clean-up,” said Diana Choyleva, from Lombard Street Research. Shadow banking ground to a halt in February as tougher rules and the fears of default scared away investors.

“We think the yuan is 15pc to 25pc over-valued. The economic data have been getting weaker and the authorities must be realising that the only way to square the financial circle is to allow the currency to help them,” she said.

The yuan has fallen 2pc against the dollar since January, weakening sharply on Monday after the central bank widened the trading band. While there are technical reasons for the weakness – including efforts to punish speculators with a pinch of “two-way” risk – investors may soon start to ask whether China is quietly devaluing the yuan to cushion the shock of debt deflation.

Premier li Keqiang warned last week that economy will be allowed to slow further and told industry leaders to brace for defaults. “We are going to confront serious challenges this year.”

Kit Juckes, from Societe Generale, said years of double-digit wage growth and slowing productivity gains have eroded China’s competitiveness, cutting the trade surplus from 10pc to 2pc of GDP.

The yuan has already weakened from 6.05 to 6.17 to the dollar. Mr Juckes said there could be a wave of forced selling by leveraged traders if it breaks through 6.20-6.25. The question then is whether the central bank would step in to stabilise it. “You start to wonder whether they might not want a weaker currency to give the economy a helping hand,” he said.

Any such move would amount to a beggar-thy-neighbour policy, exporting excess capacity and deflation to the rest of the world. Europe is the region most nakedly exposed.