Why Japan invests too much

March 29, 2014 Leave a comment

Why Japan invests too much

March 20, 2014 7:48 amby Andrew Smithers

The Japanese government is trying to encourage the country’s companies to increase the amount they invest. This is like trying to push water uphill. Japan as a whole and in terms of business already invests too much.

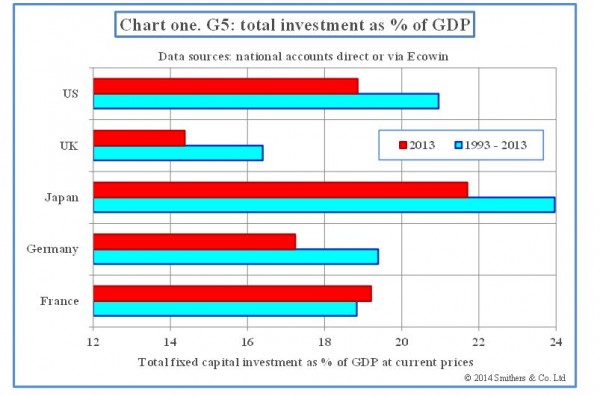

Chart one (above) shows that Japan invested more than any other Group of Five advanced economy over the past 20 years and was still doing so last year.

Chart two (below) shows that investment was far too high even if only business is considered, rather than everything.

Japan has probably been the most economically successful G5 country, at least over the past 15 years, if due allowance is made for the fall in the working population (as explained in my third blog, “Japan: the confusion at the heart of Abenomics”). But, because of its demography, its gross domestic product has nonetheless grown more slowly than other G5 countries.

The efficiency of capital can be measured by seeing how much investment is needed to produce a given amount of output. This is known as the incremental capital/output ratio, or Icor. Japan’s combination of heavy investment and slow growth has meant that Japan’s capital efficiency has been by far the worst of any G5 country (see chart three below).

The massive inefficiency of Japan’s capital investment has meant that the return on capital has also been extremely poor. Output is divided between labour (wages and salaries) and profits. This ratio varies from country to country and over time, but it does not vary all that much for mature economies such as the G5 (which also includes the US, Germany, UK and France). As a broad generalisation 30 per cent of output goes to profits, measured before depreciation, interest and tax, and 70 per cent goes to labour. The differences between countries are far too small to make up for the huge difference in capital efficiency shown by the Icor.

The return on capital in Japan has therefore been extremely bad, whether measured in total or in terms of business investment. This is why investment in Japan has been steadily falling and it needs to go on falling. The government’s hopes of persuading companies to invest more are absurd and doomed to fail. Indeed, I plan to explain later why any success in the short-term would simply make matters worse looking further ahead.