An Asian Innovator in the Race Towards the Autonomous Car and the Next Bosch India for Buffett’s Growing Auto Empire

May 4, 2015 Leave a comment

| “Bamboo Innovators bend, not break, even in the most terrifying storm that would snap the mighty resisting oak tree. It survives, therefore it conquers.” |

| BAMBOO LETTER UPDATE | May 4, 2015 |

Bamboo Innovator Insight (Issue 81)

|

| Dear Friends,Can You Guess This Asian Wide-Moat Company? An Asian Innovator in the Race Towards the Autonomous Car and the Next Bosch India for Buffett’s Growing Auto EmpireIs Berkshire Hathaway building an automotive empire next?Following up on the Oct 2014 acquisition of auto dealer Van Tuyl with $9bn in sales, Buffett bought German bike gear maker Devlet Louis Motorradvertriebs for $450m in Feb 2015 and splurged $560m for a 8.7% stake in Axalta Coating (AXTA US), the former DuPont auto coatings business and the world’s biggest supplier of coatings to auto repair shops and the second-largest provider to manufacturers of cars and lights trucks in Apr 2015. Interestingly, BRK invested in Axalta when it is trading at an all-time high. The valuation of the Axalta deal was not cheap at EV/EBIT 21x and EV/EBITDA 13x, highlighting the confidence that Buffett has in the well-managed consolidators in the automotive sector with a long-term reputation amongst clients. BRK also controlled a 2.6% stake in General Motors (GM US) and is exposed to the automotive sector through Lubrizol, a maker of lubricants for automobiles and machinery, which was acquired for $9bn in 2011.Are there worthy automotive candidates in Asia for BRK to pounce upon, beyond auto dealers?This month, we highlight a wide-moat innovator who is the #1 in Asia in a patented automotive electronics part that is part of the fast-growing Advanced Driver Assistance System (ADAS) market worth >$22bn by 2018, doubled from $11bn in 2014. The ADAS market is driven by more stringent safety requirements from governments forcing the automotive industry to develop automotive electronics solutions to increase vehicle safety. [Company’s name] is the third-largest in the world behind Valeo (FR EN) and Bosch. It has >50% market share in new cars sold in China, and the installation rate of this ADAS product on China’s auto is still low (35%+ on new cars vs 80%+ in developed markets). Established in 1979 by founder and Chairman Mr. C, [Company’s name] is one of the rare Tier-1 automotive suppliers in Asia to major OEM car makers that include Ford, GM, Daimler, Hyundai, Nissan, China’s top 10 auto companies such as Great Wall Motor, thereby directly shipped to them and involved in their R&D processes and early stage processes of concept car design and prototyping, creating a pre-emptive advantage in winning new orders.

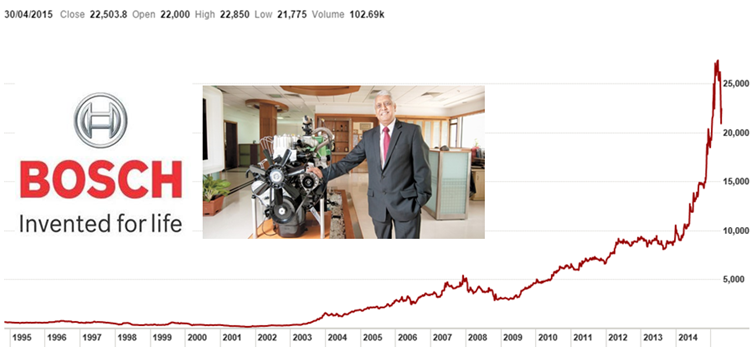

Over the past 36 years, [Company’s name] has forged formidable competitive advantages in scale, product quality, technological know-how and R&D capabilities and in May 2012, [Company’s name] outgunned illustrious industrial automotive giants Valeo (founded in 1923) and Bosch (founded in 1886) to sign a breakthrough global 10-year contract with GM, with the commencement of worldwide shipment to 18 countries and 25 factories at the end of 2016. The journey has not been easy for Mr. C who recounted his days of carrying the same brief case containing the auto parts to knock on doors.. ******** Q: “Can you share with us what is so difficult about making these [Company’s flagship product] and automotive electronics parts beyond having more capital and money?” Mr. C: “Time. Time is the most difficult thing. The closed, protected automotive industry demands an exceptionally high standard of safety, durability and reliability of the 8,000 to 15,000 auto parts that go into the car, even more so for automotive electronics products since these are integrated into a system and platform as opposed to some stand-alone parts. It’s not a case of whether you can produce the parts with high quality and people will then use them. Only AFTER you produce the parts and somehow manage to convince someone to test it for at least a year or more, ensure that the parts stay defect-free, zero PPM (parts per million), under rigorous test conditions, can the OEM carmaker say, OK, we will try it. But the actual truth is, when you have produced what you think is a high quality part and approach the OEM carmakers, they will all say, ‘Why don’t you bring this to other factories to test it out first. If the others are ok, we will look at it. Every car factory will say the same to you. No one wants to be the guinea pig, the lab rat. As a result, you will never get in to their supply chain. To win their trust is not easy. I remembered in those years, I would carry the same brief case that I use to knock on doors. In it contained the auto parts. Everyone would say that they are interested and to send them the samples. However, when the samples are sent, the rock sinks to the ocean and there is no news. Hence, time is the biggest cost and the most difficult thing. One might think that automotive electronics products could be similar to consumer electronics parts. Hence, the barriers to entry are low and there could be new entrants. This thinking could not be more wrong. On our flagship product itself, do you know that a [Company’s flagship product] would have to withstand extreme hot and cold temperature changes, withstand vibration, stay water-resistant, anti-dust, anti-humidity, anti-signal disruption, and a battery of tests. Amongst these tests is the requirement to continue functioning in the sudden change from minus 40 degrees Celsius to 85 degrees Celsius. And our engineers have to go with the OEM carmakers to actual sites in Northern Europe, China’s Heilongjiang and the Gobi desert to do the tests. [Company’s name] is proud that our production quality has reached over 36 months (and still running) of zero PPM (parts per million) defect. This is the real reason why we are able to win Valeo and Bosch and win the hearts of our customers to place orders with us. ******** Bosch India (NSI: BOSCHLTD) – Stock Price Performance 1994-2015

In the ruthless cut-throat automotive industry, the fact that Bosch India (BOS IN, MV $11bn) and [Company’s name] have strikingly similar EBITDA margin at 15.6% and ROE of around 14.5% (although Bosch India is net-cash but has low dividend payout) speaks volume about [Company’s name]’s wide-moat advantage in securing long-term pricing power and earnings sustainability with the major OEM carmakers by winning their trust to strike long-term partnership in global platform deals. Bosch India trades at an expensive valuation premium of EV/EBITDA 45.7x as compared to 15x for [Company’s name]. While [Company’s name] has a dividend yield of 2.2%, it is not cheap in valuation at EV/EBIT 18.4x and EV/EBITDA 15.1x. We believe that the key to valuation success for an innovative automotive supplier is a Tier-1 status (as opposed to the “cheap” Tier-2 or 3 players) and the long-term visibility and sustainability in generating quality growth by offering products and technology that play into the upcoming movement towards either (1) “Efficiency”: fuel efficiency, emissions and environmental footprint of a car, or/and (2) “Content”: comfort, convenience and safety features that help improve the ownership experience of the automobile. Bosch India belongs to the “Efficiency” category when it was re-rated since its tipping point moment in 2006 when it set up the manufacturing facilities for CRDi-based passenger diesel engine system in India and market value compounded 8-fold in 9 years to $11bn while sales climbed 150% over the same period to generate a doubling in earnings growth from Rs5.5bn in FY06 to Rs10.5bn ($160m) in FY14. [Company’s name] belongs to the “Content” category and is also one of the rare few Tier-1 auto suppliers in Asia. We believe the technical superiority of [Company’s name] in developing low-cost innovative solutions that enabled it to command a >50% market share for new cars in China deserves to command a higher valuation. We are impressed by Mr C’s dedication, patience and focus in not only building up a rare Tier-1 supplier capability but also in forging a corporate culture that feels like an enterprise of engineers, reminding us of automotive parts innovator Gentex (GNTX US, MV $5.2bn)/John Bauer. [Company’s name] has around 400 engineers and R&D specialists, comprising 20% of the workforce, a similar ratio to Gentex. We like how [Company’s name] has consistently reinvested back into the business to develop its R&D and new product innovation capabilities beyond its flagship product that are now building up sales momentum as well as set the company on a long-term growth trajectory path in the fast-growing multi-billion ADAS market and the race towards the autonomous car. As Mr C puts it aptly: “What’s next for [Company’s name] isn’t about how many cars there are; it is about how electronic the cars can be. There is great long-term potential for automotive electronics parts in the future car, which will jump from the present 10% of the total cost of making a car to 40%. To capture this long-term opportunity, [Company’s name] will continue to build upon our 36 years of accumulated know-how, capabilities, global partnership platform and underlying trust with our global clients to enable [Company’s name] to shine bright in the global automotive industry!” Who is Mr. C and this wide-moat Bamboo Innovator? A new monthly issue of The Moat Report Asia is now available! Access the in-depth idea presentation: http://www.moatreport.com/members/ Warm regards, KB The Moat Report Asia http://accountancy.smu.edu.sg/faculty/profile/108141/KEE-Koon-Boon A new monthly issue of The Moat Report Asia is now available! Access the in-depth idea presentation: http://www.moatreport.com/members/ Paid subscribers get:

|