The long-term-care insurance industry now is shrinking, premiums are soaring and there is no fix in sight

July 2, 2013 Leave a comment

Updated July 1, 2013, 11:03 p.m. ET

Long-Term-Care Insurance Leaves Customers Groping

KELLY GREENE and LESLIE SCISM

Rob and Katherine Deane thought they were being responsible by buying insurance policies to provide for care in their later years. Instead, the Michigan couple are encountering a growing gap in health-care coverage that the government overhaul will do nothing to fix.

The Deanes say they got hit last year with rate increases on both of their long-term-care policies, insurance plans that pay for nursing homes or in-home care. Manulife Financial Corp.’s MFC.T +0.42% John Hancock unit told Mrs. Deane that the premium on her 10-year-old policy would jump 77% to $6,406 a year. Her husband’s insurer, Unum Group, UNM +1.26% increased his premium by 25%.After they complained, Hancock trimmed Mrs. Deane’s rate hike to 46%. In exchange, she agreed to shrink the policy’s benefit period to six years from 10. “Seniors are really getting hammered,” says Dr. Deane, a 76-year-old retired surgeon.

Spokespeople for Hancock and Unum declined to discuss the Deanes’ specific situation. In general, the insurers say, they give policyholders ways to reduce or eliminate a looming rate increase, generally by giving up part of their benefits.

The long-term-insurance industry now is shrinking, premiums are soaring and there is no fix in sight. At the same time, government safety-net programs, already under cost-cutting pressure, are bracing for demand from more of the 77 million aging baby boomers.

President Barack Obama’s health-care overhaul is supposed to provide insurance for millions of Americans. But the administration abandoned an effort to provide affordable long-term care, concluding it was too expensive. Instead, Congress appointed a commission to find ideas that could become law in five years.

Currently, Medicare pays for only short stays in nursing homes or in-home care under limited conditions. For the most part, seniors who need care have to burn through their savings to pay for it. Only after they are impoverished will Medicaid—the government health program for poor people—pay for a basic level of care.

Insurers have been aware of this gap for decades, and many began selling long-term-care policies in the 1980s and 1990s. They vowed to provide policyholders with better access to high-quality nursing homes and home-based health care than Medicaid.

But insurers underestimated how fast medical costs would rise, and how many seniors would actually use the benefits. And they underpriced the insurance premiums. Making matters worse, some insurers that were “hungry for market share” charged too little at first and planned to increase premiums later, says Joseph M. Belth, editor of the Insurance Forum newsletter and professor emeritus of insurance at Indiana University.

Many once-prominent sellers of long-term-care insurance are in full retreat. Five of the 10 largest sellers, includingMetLife Inc., MET +1.70% Prudential Financial Inc. PRU +0.37% and Unum, have sharply reduced or discontinued sales since 2010, according to Moody’s Investors Service.

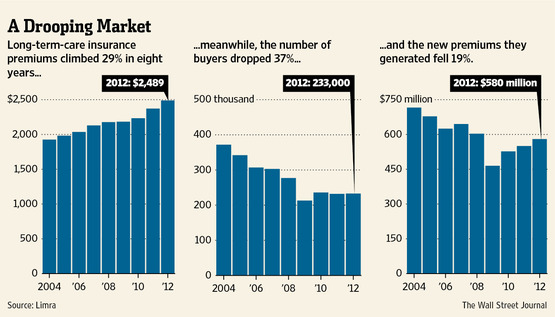

Only a dozen or so companies still sell meaningful numbers of policies, down from about 100 a decade ago, according to LifePlans Inc., a consultant. In the past decade, sales to individuals have fallen by two-thirds to 233,000 policies a year, and the number of insured people is stuck at about seven million.

Most of the actuarial assumptions made by insurers years ago turned out to be overly optimistic. Underestimating how long elderly policyholders would live—and collect benefits as a result—led to a 14% shortfall in premiums, according to a presentation to college students by PricewaterhouseCoopers principal Larry Rubin.

And many state regulators erred by routinely signing off on the premium on the new products and subsequent rate increases without questioning the companies’ pricing assumptions, some officials say.

Since then, many states have adopted “rate stabilization” laws to tighten oversight. Michigan, where the Deanes live, adopted such changes in 2006 “to reduce the potential of future rate increases by requiring a more accurate initial pricing of policies by insurers,” says an insurance department spokesman.

The insurance industry also failed to realize how desperate many Americans are to protect themselves from runaway nursing-home costs. So they cling to their long-term-care coverage for dear life.

Many insurers predicted that 5% to 7% of people who bought long-term-care coverage would cancel their policies each year without tapping their benefits.

Instead, the annual cancellation rate at many insurers has been less than 2%, actuaries say. Initial premiums would have been about 35% higher if insurers had assumed such a low cancellation rate, PricewaterhouseCoopers estimates.

“We don’t want to be a burden to our children,” says Allan Sugarman, 71, of Morganville, N.J. Mr. Sugarman and his wife, Joyce, bought long-term-care policies from John Hancock about a decade ago after hearing that a friend had paid more than $100,000 to support his father in an assisted-living facility. They later learned another friend’s disabled mother was sleeping on her son’s sofa, for lack of an affordable alternative.

The couple are paying $6,380 a year for the two policies. They want to keep their coverage so much that Ms. Sugarman says she was relieved when Hancock let them avoid a double-digit rate increase by sacrificing part of an inflation-protection perk.

Hancock says it won’t discuss specific policyholders.

Some regulators are making it tough for insurers to bump up premiums to a sustainable level, contributing to the decision by some companies to leave the market. Last year, a Pennsylvania state-court judge faulted the state’s insurance department for not approving big premium increases for two troubled insurers.

“This case presents a serious indictment of the existing system of rate regulation of long-term-care insurance,” Judge Mary Hannah Leavitt wrote. Pennsylvania officials have appealed the ruling and are seeking approval of a rehabilitation plan for the shaky insurers. The department declined to comment on the judge’s comments.

Genworth Financial Inc., GNW +4.47% with about a 33% market share of long-term-care policies sold to individuals, said in May that it is seeking premium increases averaging more than 50% to stave off more losses in its oldest policies.

Genworth also halted sales June 1 through AARP, the older-Americans’ group with a huge pool of potential customers.

“We’ve learned a lot over the last 30 years, and we now believe we have a better ability and more knowledge” to issue policies that “provide significant financial protection to Genworth,” Genworth Chief Executive Thomas McInerney said in an interview.

The insurer started requiring blood tests and other medical screening, which the industry generally hadn’t done before. And it is charging women who apply individually more than men for the first time because women tend to live longer and require more years of care.

In general, a 55-year-old single person buying long-term-care protection can expect to pay $2,065 a year for $162,000 in benefits, including a 3% inflation-protection rider—a 20% increase from last year, according to the American Association for Long-Term Care Insurance trade group.

Rate increases are forcing existing policyholders to dig into savings, sacrifice elsewhere—or drop their coverage. For insurers, that could mean healthier policyholders abandon ship while sicker, more expensive customers hang on.

Bob Barry, a 74-year-old AT&T Inc. T -0.28% retiree in Bluffton, S.C., says he walked away from his Hancock policy 18 months ago after the annual bill for basic, three-year coverage jumped about 50% to nearly $1,000. He and his wife, both healthy, are grappling with big premium increases for their homeowner’s insurance, too, he says.

For the time being, they chose to maintain coverage for his wife, who is four years younger, reasoning that she could outlive him. “I wanted her to keep hers because I expect to check out before her,” he quips.

Many insurance agents and financial planners are steering clients to new “hybrid” coverage, basically life insurance with a rider providing long-term-care benefits. One appeal: The policyholder can leave something to heirs even if the long-term-care benefits don’t get tapped.

But the long-term-care benefits often are less generous than those in conventional policies, and policyholders typically have to write one big check upfront to obtain the coverage, rather than paying premiums each year, says Nancy Courser, the Deanes’ insurance agent.

“We have no way of knowing if these policies will self-destruct in the future,” cautions Mary Ahearn, a financial planner in Arizona.