China, Australia and a hard landing

July 4, 2013 Leave a comment

China, Australia and a hard landing

Neil Hume | Jul 04 03:53 | Comment | Share

Kevin Rudd 2.0 has been quick to highlight the dangers posed by slowing Chinese growth since he was returned as Australia’s prime minister. For example: When I look at the challenges of rest of this year, and certainly for the upcoming three-year term, the huge outstanding economic challenge for us is the end of the China resources boom. This will have a dramatic effect on our terms of trade, a dramatic effect on living standards in the country, a dramatic effect also potentially on unemployment unless we have an effective counter-strategy. And… There are a lot of bad things happening out there. The global economy is still experiencing the slowest of recoveries. The China resources boom is over. China itself, domestically shows signs of recovery and when China represents such a large slice of our own economy, our jobs and our own opportunities for raising our living standards. But just how dangerous is a Chinese slowdown?Barclays economist Kieran Davies has some answers.

Our China team’s central case is for China to average GDP growth of 7.4% over 2013 and 2014, but it sees an increased risk that China may briefly experience a temporary hard landing (ie, growth of 3% or less) at some point in the next three years as the authorities reform the economy and reduce leverage.

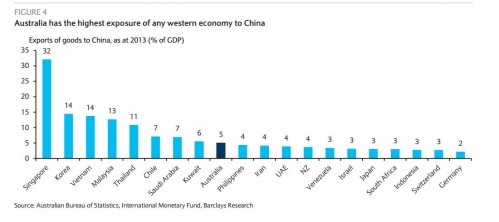

Australia would be hit hard in that scenario as it has the most exposure to China of any western country, with China accounting for 35% of exports, or 5.7% of GDP. Modifying some recent IMF analysis, we calculate the direct hit to Australian growth from a slump to 3% growth in China as 1.4pp, which could be enough to tip Australia into recession given the Japan-led boom in mining investment is starting to roll over.

Importantly, though, a collapse of the exchange rate would help cushion the shock, with the Fund, somewhat optimistically in our view, estimating a completely offsetting effect (the budget would also blow out, and the RBA would cut the cash rate towards the cited 1% floor)

However, the most pressing challenge to Australian growth isn’t China, says Mr Davies. It’s the end of the unprecedented resource investment boom. Please take note Mr Rudd.

More generally, we are mindful that a hard landing is only a risk to our China team’s central case, with Australia’s exports to China reaching a fresh record high in May on strong growth in iron ore volumes over the past year. At present, the tangible challenge to growth in Australia is the end of the Japan-led boom in mining investment, where mining capex may have already peaked. This boom is already starting to pay dividends via a surge in bulk commodity exports, but we still think that overall growth will be weak next year as stronger exports (combined with a lift in interest-sensitive spending) is unlikely to be enough to offset the shortfall left by mining investment returning to a more normal level.

The adjustment in mining investment is likely to take a few years as capex returns to more normal levels, with the exchange rate likely to trend lower as increased commodity supply drags commodity prices down. At the same time, the Reserve Bank should retain an easing bias and seems likely to keep rates at a record low of 2.75% for an extended period to help the economy adjust to lower mining investment.

Quite, because it is a huge hole to fill.