Novo’s Scale Advantages and Drug Lineup Broaden Its Wide Moat

July 4, 2013 Leave a comment

Novo’s Scale Advantages and Drug Lineup Broaden Its Wide Moat

By Lauren Migliore, CFA | 07-03-13 | 06:00 AM | Email Article

Novo Nordisk (NVO) has been consistently at the forefront of diabetes care, and we expect favorable industry dynamics and the firm’s formidable research and development and diabetes-focused commercialization infrastructure to continue to drive strong returns on shareholder capital.

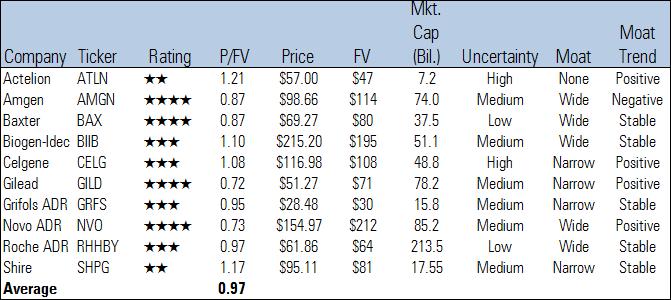

We expect growth to come from increased market penetration in diabetes care and stable growth in biopharmaceuticals. Once-daily Victoza continues to outperform once-weekly Bydureon in the GLP-1 market thanks to the competing drug’s inability to prove noninferiority in trials, and we expect Victoza to break the $2 billion mark in annual sales this year. Novo’s next-generation products, Tresiba and Ryzodeg, will help the company defend its leading insulin franchise, though we expect that a complete response letter will delay U.S. launch by two to three years. This regulatory setback, along with recent safety concerns for the incretin class–of which Victoza is a member–has caused shares to underperform, and Novo is now trading at one of the steepest discounts to fair value (over 20%) in the large-cap biotech space (see the following table). However, we think these issues have little long-term impact on the company’s value, and instead present investors with the rare opportunity to own this high-quality name at an attractive price.

Comparables Within the Biotechnology Industry

Source: Morningstar

Portfolio/Moat Rating: Novo’s Leading Position in Diabetes Will Benefit From Industry Tailwinds

We assign Novo a wide economic moat based on its industry-leading, diabetes-focused salesforce, loyal patients, significant intellectual property, little near-term patent exposure, and robust pipeline. Novo is the world’s premier diabetes drugmaker and will benefit from substantial market tailwinds thanks to an increasingly overweight world population. The firm remains at the forefront of research in the next generation of insulins, with ultra-long-acting insulins launching this year and oral insulins in early-stage trials. With patent expirations on key products still several years out, Novo has relatively little near-term exposure to generic competition. The firm is also leveraging its expertise in protein therapy into other areas like human growth hormone, which allows Novo to further supplement core revenue and boost profit margins. Novo’s proven ability to innovate in diabetes care, hormone therapies, and blood coagulation provides the firm with the potential for at least 20 years of excess economic profits.

Diabetes’ spread will continue to drive robust demand for insulin. Today 371 million people worldwide are affected by diabetes, and this number is expected to grow to 552 million by 2030, according to the International Diabetes Foundation. While Type I diabetes is on the rise, the epidemic stems primarily from the growing prevalence of Type II diabetes thanks to an increasingly obese and sedentary global population. Global insulin sales topped $19 billion last year. With the incidence of diabetes expected to increase by more than 50% over the next two decades, we expect diabetes to continue to drive robust demand for insulin. Specifically, we think Novo’s modern insulin portfolio (NovoLog, NovoMix, Levemir, and Tresiba/Ryzodeg) will grow 65% over the next five years, and we expect Victoza’s sales to more than double to nearly $4 billion during the same period.

The diabetes market is characterized by high barriers to entry, especially for generic hopefuls. Potential rivals looking to break the oligopoly of Novo, Sanofi (SNY), and Eli Lilly vise-hold on the diabetes market face multiple barriers to entry. To begin, insulin is not a very dynamic market; according to Novo, close to 95% of patients stay on their current therapy from year to year. Diabetes is a chronic disease and diabetics make extremely sticky customers, forcing generic entrants to compete for share primarily among new patients. Most patients are elderly and become accustomed to a certain insulin regimen over time. Furthermore, unlike small-molecule drugs, automatic substitution does not occur at pharmacies for insulin; physicians need to specifically prescribe a generic version. We believe risk-averse physicians will be hesitant to prescribe a new–albeit slightly cheaper–product if their patient is well controlled on his or her current therapy, especially considering that significant risks like hypoglycemia can arise from altering a treatment regimen.

The prevalence of devices in diabetes treatment intensifies the stickiness of customers, and the complexity of their manufacture erects further barriers to entry for a generic player. From a generic drugmaker perspective, the popularity of devices adds an additional layer of cost, clinical trial requirements, and regulation to bringing biosimilar insulin to market. The importance of first-mover advantage and inertia in diabetes treatment are illustrated in device penetration dynamics worldwide. According to Novo, the majority of mature markets in the world have device penetration rates of about 90%. However, although this rate is steadily increasing over time, less than 40% of patients in the U.S. receive their insulin via devices. The U.S. has historically been a stronghold for Lilly, which did not have a portfolio of devices in the past and thus shaped the market toward insulin in vials, while Europe has traditionally been dominated by Novo, which boasts a wide lineup of insulin devices. Treatment inertia is also seen in China, where Novo has aggressively promoted both the human and modern versions of its premixed insulin. Premixed formulations compose 65% of insulin in China, contrary to most Western markets where long-acting insulins predominate.

The insulin market is also characterized by significant economies of scale in manufacturing and distribution that favor larger, incumbent players. A generic drugmaker would have to make significant upfront investments to build an insulin production facility; Novo estimates that a reasonable active pharmaceutical ingredient manufacturing facility costs $1 billion to construct. All this investment must be made up-front without any definitive knowledge of the payoff down the road. Although the FDA and the European Medicines Agency are evaluating the issue, there is still no finalized pathway in place for generic biologics, and a great deal of uncertainty remains surrounding the type of clinical trials drugmakers might need to conduct to show bioequivalence for insulin. Clinical data is costly, and there is no guarantee of success; Marvel Life Sciences withdrew its marketing application to the EMA in 2008 after trials demonstrated that its biosimilar insulin was not comparable to the reference product.

Despite wide-moat potential in diabetes, key drugmakers face new challenges on horizon. While Novo, Sanofi, and Lilly have been highly successful maintaining market share to date, changing regulatory dynamics and additional patent expiries will present these diabetes powerhouses with a host of new challenges in the near future. Many developed countries are contemplating abbreviated pathways and less restrictive clinical programs for biosimilar products as a way to curb skyrocketing health-care costs. Cost pressure from payers could lead to lower regulatory hurdles for biosimilar entrants over time. Accordingly, Novo is leveraging its expertise with therapeutic proteins into new indications. The firm’s recombinant factor VIIa product NovoSeven makes a sizable contribution to revenue, and Novo has introduced a slew of growth hormone and inflammation therapies into clinical development to further diversify its top line.

Pipeline/Moat Trend: Novo Is Broadening Its Portfolio Within Some of the Fastest-Growing Markets

Novo’s response to both branded and biosimilar competition has been continuous innovation and improved therapy. Regular human insulin has been used for decades to control blood sugar levels, but it remains a less-than-ideal treatment option due to its slow absorption and delayed onset of action. These shortcomings have opened the door for modern insulin analogs, which offer improved durations of action, lower risk of hypoglycemia, and less weight gain. Sales of human insulin have declined consistently over the past few years as drug companies convert patients to modern insulin analogs, which offer numerous safety, efficacy, and convenience benefits. To illustrate, human insulin composed only 18% of sales in Novo’s diabetes care segment last year, compared with 25% in 2010 and nearly 50% in 2005.

Novo’s newer offerings enjoy a longer runway of patent protection and claim a pricing premium over human insulin. However, even these state-of-the-art products are unable to mimic the body’s natural insulin response and still require patients to inject themselves at least once daily. With patent expirations for modern analogs looming, Novo is positioning itself for the next advance in insulin therapy. Novo is also in late-stage development for several additional diabetes and obesity candidates, including label expansion for Victoza in obesity and a long-acting GLP-1 candidate semaglutide.

Regulatory setbacks should delay launch of Novo’s next-generation insulin in the U.S., but we think Tresiba and Ryzodeg will ultimately gain approval. The firm’s ultra-long-acting insulins, Tresiba and Ryzodeg, were shown to offer glucose control similar to Lantus, even when used only three times a week, and were recently approved in Europe. In a disappointing turn of events, the firm announced that it has received a CRL from the FDA for the U.S. approval of its next-generation insulins, Tresiba and Ryzodeg. Despite an 8-to-4 positive advisory panel recommendation last November, the FDA decided that the drugs’ application cannot be approved in its current form. In the letter, the FDA requested that additional cardiovascular data from a dedicated outcomes trial be provided before the insulins can be approved. We see the CRL as further evidence of an increasingly risk-averse FDA regarding the safety profile of new diabetes drugs in the wake of controversy surrounding GlaxoSmithKline‘s (GSK) Avandia in recent years. Novo is waiting for further discussions with the FDA before providing an updated timeline for when these data will be available, but we estimate this will delay launch until at least 2015, if not 2016. Novo will likely start the trial, which will compare the number of cardiovascular events associated with Tresiba to Lantus, within one year, and data to support interim analysis could be available two to three years after the trial’s start.

This news is definitely a boon to Sanofi’s Lantus–currently the best-selling insulin on the market–which was threatened by the potential from a newer, ultra-long-acting Novo product. Tresiba and Ryzodeg have been approved in Japan, the European Union, and other countries, and should begin to boost the firm’s outside-U.S. performance in the second half of this year. It is still too early to tell how Tresiba is faring against Lantus in Europe (especially given the 70% pricing premium it set in order to try to raise European insulin pricing toward that of the U.S.). However, we would expect initial sales to come from patients who aren’t well controlled on existing products or who have to administer twice-daily injections due to Lantus’ dose ceiling, and for some cannibalization to occur from Lantus and Levemir. Data regarding share of new patients will likely come later in the cycle.

Furthermore, we think there is still a very high chance that Tresiba and Ryzodeg will eventually make it to market in the U.S. following the submission of additional data. That said, our expectations for these products have always been relatively muted, as we believe it will be difficult to convince doctors of the benefits of the new products over existing therapies. The CRL is not expected to meaningfully affect Novo’s earnings this year, as any sales losses will be offset by decreased launch costs for the next-generation insulin. Further, the firm intends to redouble marketing resources behind its currently marketed modern insulin portfolio. However, if the drugs fail to launch within the next two to three years, it will make the firm’s double-digit long-run earnings growth targets a bit more challenging to achieve. Even so, Novo boasts an extremely diversified diabetes and biopharmaceutical lineup, and Tresiba and Ryzodeg are not essential to the long-term success of this wide-moat, positive-trend biotech. Given a high degree of customer stickiness, we expect the insulin market to remain a fairly stable oligopoly consisting of Novo, Sanofi, and Lilly for the foreseeable future.

Novo is looking to leverage its expertise in protein therapy to establish a leadership position in other areas like hemophilia and inflammation. NovoSeven, the leading recombinant treatment for acute bleeds in inhibitor patients, has secured a foothold for Novo, which the firm plans to expand through a pipeline of new hemophilia A and B treatments. Novo stands to bring innovative, long-acting factor VIII and IX proteins to the market in 2014 and 2015, respectively, putting it in a position to begin to steal some of the market’s growth from incumbents like Baxter (BAX), CSL (CSL), Grifols (GRFS), and Bayer (BAYN). Today, 10% of Novo’s sales and 14% of its profits stem from hemophilia, by our estimates, and we expect this contribution to remain relatively stable in the near term. The operating margins of the firm’s biopharmaceuticals segment have averaged about 80% higher than Novo’s core diabetes care business over the last three years. Therefore, we expect new launches from the firm’s hemophilia pipeline to mostly offset the impact of Novo’s new insulin line over the next few years.

Biosimilar/Generics Risk: High Barriers to Entry Entrench Key Insulin Players

Novo, with its broad portfolio of insulin products, is no stranger to competition. Insulin has been sold for decades and is one of the easiest biologic drugs to manufacture. In several markets, such as India and China, Novo already faces competition from biosimilars, yet the company maintains a 60% market share by volume in these countries. The insulin market is dominated by Novo, Sanofi, and Eli Lilly. According to IMS, these three key players control over 90% of the world’s total insulin volume, while 40-plus other players–including biosimilar manufacturers–compete for the remaining share. Although patents have already expired on several leading human insulin products (such as Novo’s Novolin and Lilly’s Humulin and Humalog), the only places where biosimilar insulin has had more than a single-digit impact on market share are in emerging markets. For example, biosimilar insulin represents only about 10% of volumes in China.

Unlike many biologic drugs, insulin is consumed in such large quantities that production scale is important in driving competitive manufacturing costs. The low cost per unit of insulin makes the space less attractive compared with other therapeutic areas. The average cost of modern insulin is roughly $4.50 per day in the U.S., followed by $3 per day in Japan and $1.50 per day in Europe, which leaves generic drugmakers little room to meaningfully cut prices. As a result, generic drugmakers’ traditional low-cost strategy isn’t as effective. Novo has spent years manufacturing insulin and optimizing its processes with yeast cells, and the firm can produce insulin in very high volumes using its process of continuous fermentation. Accordingly, Novo can use competitive pricing on older insulins as a defense against new generic entrants. Additionally, Novo continues to separate itself from competitors with its strong brand, innovative insulin formulations and device delivery systems, and a focused salesforce.

Although competition from generic human insulin is on the horizon, Novo has been steadily converting patients to premium-priced modern insulin analogs, which will benefit from patent protection for several more years. By the time marketing exclusivity for these drugs runs out, Novo should have ramped up yet another generation of insulins. Combined, we think these factors insulate Novo well from the threat of biosimilars.

Valuation

We recently increased Novo’s fair value estimate to $212 per ADR from $177 per ADR after lowering our cost of equity assumption to 8% (from 10%). We model Novo on a constant-currency basis in Danish kroner, and convert our fair value estimate to dollars at the current spot rate of DKK 5.67 per $1. We project that Novo will yield an 8% CAGR during the next five years. We expect diabetes care revenue to grow faster than biopharmaceuticals thanks to Victoza’s strong uptake and continued patient conversion from human insulin to modern insulin analogs. We think Tresiba will take at least another two to three years to make it to market in the U.S., allowing Sanofi’s Lantus to remain the top-selling insulin for the foreseeable future. That said, diabetes care should make up nearly 80% of sales this year, in our opinion. Patient conversion to higher-margin modern insulin and continued growth of Victoza–a highly profitable asset for the firm–should help operating margins expand to the high-30% to low-40% range during the next five years. Our five-year revenue and earnings growth CAGRs are 8% and 14%, respectively.

In our opinion, Novo will throw off over 25% of revenue in the form of free cash flow during the next five years, which we believe the firm will deploy to fund internal capital requirements, targeted acquisitions, and its ambitious dividend and share repurchase schedule. The firm has steadily increased its dividend payout ratio over the years and recently paid out 45% of 2012’s earnings in the form of dividends. Novo also plans to return DKK 14 billion worth of value to shareholders this year through share repurchases.