Cash for copper in China (or whack-a-mole financing)

July 12, 2013 Leave a comment

Cash for copper in China (or whack-a-mole financing)

FT Alphaville | Jul 10 15:06 | 13 comments | Share

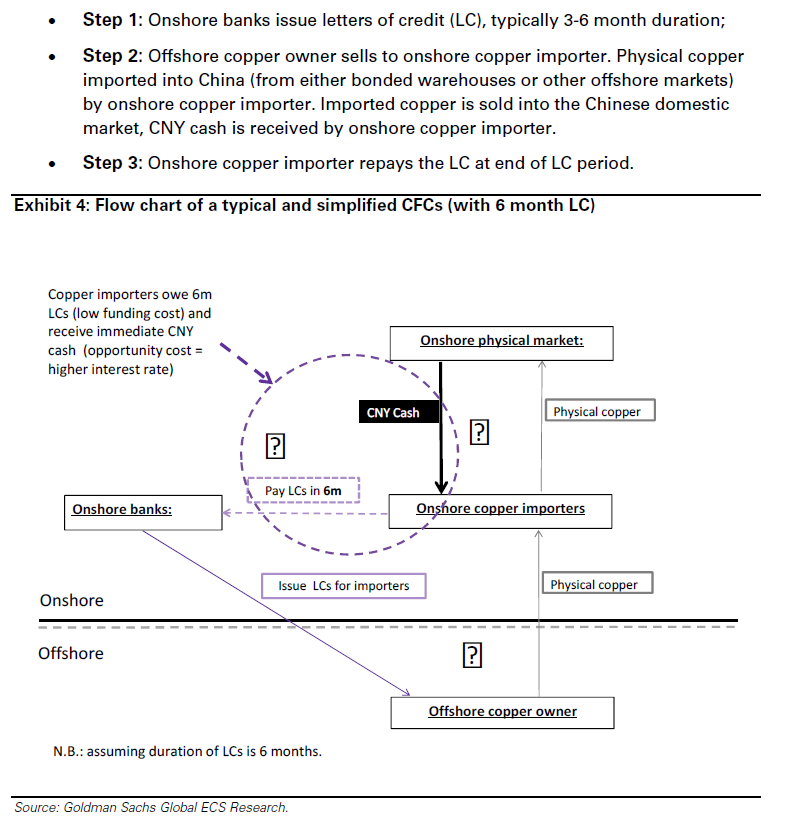

Kate’s post on the June China trade data mentions that commodities imports were the only bright spot (although it’s a somewhat dubious bright spot if it indicates a resurgence in investment). It turns out that copper imports were particularly strong, recording a 9.7 per cent year-on-year increase in June, a rather large change compared to a 14.6 per cent decline in May. Goldman point us to one compelling reason why that might be the case. It’s basically another case of whack-a-mole financing in China. Hit over-invoicing over the head and up pops ‘Cash For Copper’ (CFC) financing. This differs from more traditional Chinese Copper Financing Deals in that CFC financing involves moving physical copper from offshore to onshore; and there is no circulation of warrants. But the point of the two mechanisms is the same — getting access to CNY through cheap FX funding. A CFC financing deal looks a little something like this (click to enlarge):

And here’s Goldman’s Roger Yuan, Max Layton and Jeffrey Currie to flesh it out a little:

And here’s Goldman’s Roger Yuan, Max Layton and Jeffrey Currie to flesh it out a little:

In essence, some Chinese market participants – particularly those that are highly leveraged – are buying non-domestic copper material in order to raise CNY cash, in a development we have not seen since mid- 2011. Specifically, CFC financing – which is allowed by SAFE, and has been a factor in the copper market for years – involves the purchase and importation of non-domestic copper into China, the immediate sale of this copper into the Chinese domestic market post-importation (for immediate CNY cash), and a 3-6 month loan at foreign interest rates issued by an onshore bank. In this way CFC’s are a combination of the China/ex-China price and interest rate differentials.

The recent increase in short-term Chinese rates has resulted in CFC’s being highly profitable. Put differently, the interest rate differential adjusted copper import arbitrage is now substantially open – raising China’s demand for non-domestic material, and likely contributing to the recent pick-up in Chinese bonded physical premia (to record highs of $180-$200/t), higher LME Asia cancellations, and tighter LME copper spreads. In this way, interest rates differential changes, via CFC financing, can change where global copper inventories are located (today there is a pull on non-domestic copper inventories into the domestic market).

While these developments are typically a sign of a tightening copper market, we believe that market participants should be wary of interpreting these recent ‘signals’ – including future resulting copper import strength – as bullish, since they are in large part driven by Chinese liquidity tightness, and not primarily driven by real Chinese demand/re-stocking.

So Goldman expect strong demand for non-domestic copper (LME, Chinese bonded), supporting high bonded and ex-China premia and Chinese imports which will mean extra supply that is unlikely to be met by real Chinese demand.

This also ties into our argument that China’s powers-that-be, seeking to keep dollar shorts from unwinding — in the face of rising US bond yields, FX volatility and Fed taper speculation — are encouraging borrowing at foreign rates, mainly by inflating their own rates in relative terms.

High domestic rates make accumulation of commodities sensible so the copper keeps rolling in — especially as the PBOC remains committed to appreciating and internationalising the renminbi. The shut down in over-invoicing and the carry-trade unwind threat both fit the narrative and make China a bit of a commodity aberration. Goldman point back to mid-2011 to reinforce the point:

China’s short-term interest rates spiked, driving up the profitability of importing via CFC financing. Put differently, the rise in short-term rates led to the opening of the interest rate differential adjusted import arbitrage, resulting in a substantial rise in Chinese copper imports (Exhibit 1).