Corporate Insiders Shift From ‘Buy’ to ‘Sell’ as Bankruptcy Nears

July 12, 2013 Leave a comment

July 10, 2013, 11:02 p.m. ET

Corporate Insiders Shift From ‘Buy’ to ‘Sell’ as Bankruptcy Nears

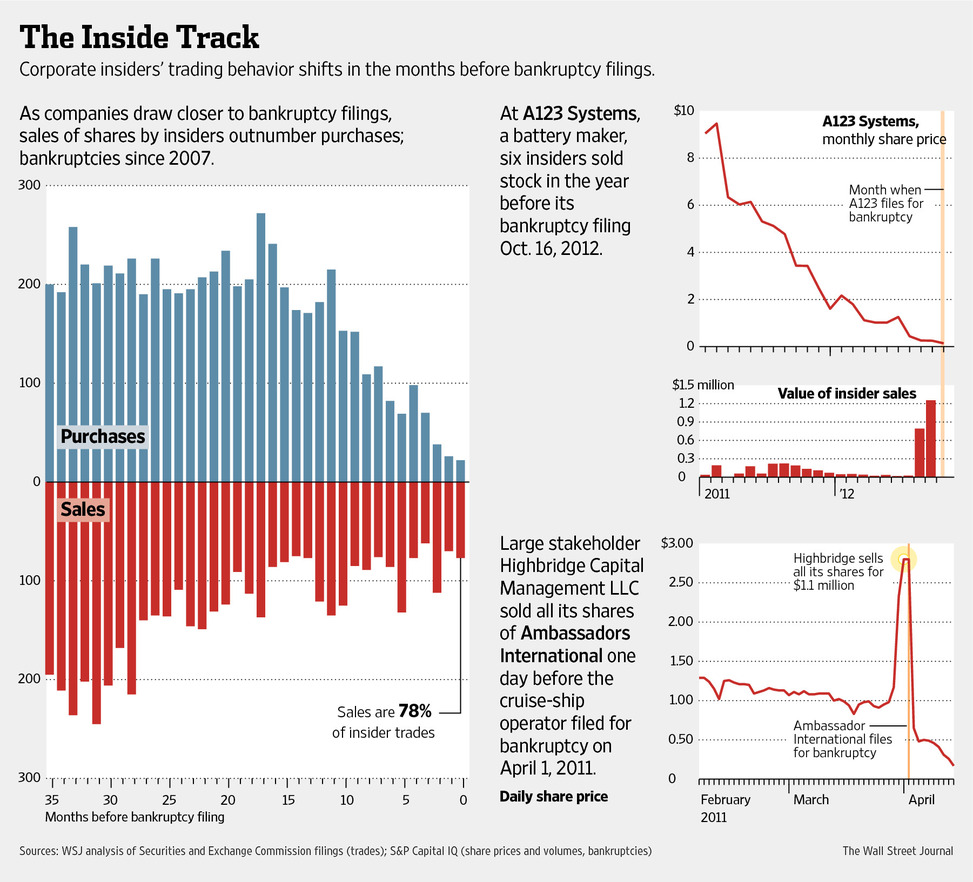

One day in September 2011, Wall Street analysts trundled into the spacious lobby at the Livonia, Mich., plant of a company called A123 Systems Inc. to view a slide presentation describing a rosy outlook for the maker of lithium batteries. “They stood up in front of investors and painted a very bullish picture,” said Andrea James, an analyst at Dougherty & Co., who took pictures of the lobby’s two-story floor-to-ceiling window. “It looked like the lobby of a company that was making money hand over fist.” Thirteen months later, it filed for bankruptcy protection. But not before insiders unloaded a total of $2.5 million of its stock. The company said the sales conformed to its policy for insider transactions. The episode suggests how corporate insiders’ trading can shift in the months before their companies file for bankruptcy. A Wall Street Journal review of thousands of trades by insiders in their own company’s stock found the trades veering heavily toward selling rather than buying as bankruptcy filings drew nearer.Such trading is sensitive because insiders often are in position to know of a company’s worsening problems ahead of other investors. The data raise a question of whether some insiders at stressed companies see the writing on the wall before ordinary investors and take action to protect their own investment. Like all shareholders, insiders are prohibited from trading on material nonpublic information.

In some cases, “insiders anticipate bankruptcy filings and they reduce their holdings so they don’t suffer the same loss as [other] shareholders,” said H. Nejat Seyhun, a University of Michigan finance professor who has studied bankruptcies and insider trading.

The Journal paired a list from S&P Capital IQ of bankruptcy filings announced since 2007 with trading by corporate insiders. Going back to three years before the filings, to detect changes in trading patterns, the analysis identified nearly 11,000 trades by insiders at 550 publicly traded companies.

The review found that insiders’ trading initially skewed toward buying. But in the last months before the bankruptcy filings, that trend dramatically reversed.

In the final three months before the filings, the average number of insider stock buys each month plunged to 29, from 176 a month one year earlier, a drop of more than 80%. Insiders’ selling eased only slightly, to 86 trades a month from 91.

Some experts say any trading at all by insiders during the last months before a bankruptcy filing can be problematic, because this corporate trauma often wipes out shareholder value.

“If a company knows it is going to file, insiders can only trade if they have no inside information and have told the market they are going to file,” said Martin Bienenstock, head of the corporate governance and bankruptcy practice at law firm Proskauer Rose LLP.

The problem, lawyers say, is that a bankruptcy typically is preceded by a series of negative developments, some of which initially might be known only to executives and other insiders. “There are many large and small companies that start addressing their distress one year or more before they ultimately file for bankruptcy,” said Mr. Bienenstock.

Of course, not all stresses at companies are known to all insiders, and certainly such stresses don’t always lead to a bankruptcy filing.

During the last full year before the bankruptcy filings, insiders at 154 of the companies reviewed, which is about 28% of them, made sales of their own company’s stock. For those who sold, the trades proved well-timed. The value of the shares sold fell an average of 16% after 30 days. That well exceeded a 6% decline after 30 days in shares insiders bought.

Patriot Coal Corp. PCXCQ -2.00% faced a turning point at the beginning of 2012 when the price of its main product began a sharp slide. This posed a danger, because two customers had agreed near the end of 2011 to buy hundreds of thousands of tons of coal from the company. Analysts who follow Patriot said they believed the price decline in January would have raised internal worry whether the sales would go through.

On Feb. 8, Patriot’s chief accounting officer, Christopher Knibb, sold $53,000 of Patriot shares at an average price of $9.05, Securities and Exchange Commission filings show.

The customers didn’t take delivery in January or February. On March 2, Patriot told one customer it was in default on its purchase contract. On May 14, according to filings with regulators, Patriot said the other customer might default as well.

A week after that, a Patriot regulatory filing raised concerns on Wall Street that these developments would affect the company’s ability to complete a credit agreement. Its shares fell 35% in a day, to $2.18.

On July 9, after the lenders revised the credit plan, making its provisions more onerous, Patriot filed for bankruptcy protection. In the filing, Patriot said the collapse of coal prices and of the two sales contracts were key developments that led to the bankruptcy.

Mr. Knibb, the officer who sold some shares in February, said he did so because he planned to buy a condo in Florida, though the transaction ultimately fell through. “I had no knowledge of there being a problem with a contract. I wouldn’t have sold shares if I had nonpublic information,” Mr. Knibb said. He added that he cleared the selling with his company’s chief financial officer and general counsel.

Patriot is now reorganizing under Chapter 11 of the federal bankruptcy code.

Selling isn’t the only defense against a vulnerable stock. At American Home Mortgage Investment Corp. AHMIQ 0.00% in 2007, the chief executive borrowed against his company shares, 37 days before telling employees the company’s business was no longer viable and it “has been forced to close.”

CEO Michael Strauss borrowed $3 million from his brokerage account—pledging American Home Mortgage shares as collateral—and wired the funds to a personal bank account, according to SEC documents. At the time he did so, June 26, 2007, Mr. Strauss’s American Home Mortgage holdings were worth at least $90 million, records show.

A little over a month later, as the housing downturn gathered steam, the mortgage firm’s stock had fallen nearly 95%.

Although Mr. Strauss’s broker liquidated a portion of his shares, their value didn’t cover what he had borrowed against them, leaving him with a profit on the transaction of about $2 million, the SEC said.

The SEC described the stock transaction in a civil complaint in which it alleged Mr. Strauss had concealed the company’s worsening condition from investors. He later settled the allegations, without admitting or denying them, agreeing to disgorge profits and interest of $2.2 million and pay a $250,000 penalty.

Mr. Strauss declined to comment. American Home Mortgage is no longer in business.

In one bankruptcy situation, involving a different company, a big shareholder bailed out just a day before the filing.

Highbridge Capital Management LLC, a hedge fund owned by J.P. Morgan ChaseJPM -0.11% & Co., was the second-largest shareholder of cruise-line operatorAmbassadors International Inc. AMIEQ 0.00% SEC filings show that Highbridge sold $1.1 million worth of Ambassadors stock, its entire position, on March 31, 2011.

The following day, Ambassadors filed for bankruptcy protection.

A spokesman for J.P. Morgan Chase said Highbridge wasn’t aware of the impending filing when it sold.

The spokesman said Highbridge had been trying to sell its position, and a surge of trading volume in Ambassadors shares that took place in the final two days before the bankruptcy filing provided an opportunity to get out.

During that trading surge, the stock price jumped to $2.80 a share from $1.18. What was behind the rise isn’t known; analysts said there could have been speculation Ambassadors would be acquired.

The stock fell more than 70% on the news that Ambassadors would file for bankruptcy. Ambassadors converted the filing to a Chapter 7 liquidation and now has no significant operations. Efforts to reach the company and former executives were unsuccessful.

At A123—named after a concept in physics called the Hamaker force constant that describes atomic interactions—six insiders sold a total of 9.1 million shares in the 12 months before the lithium-battery maker’s bankruptcy filing.

This was 34 times as many shares as insiders had sold in the preceding 12 months, and 39 times as many as they sold in the 12 months before that.

Among the sellers in the year preceding the bankruptcy filing was Gilbert Riley, co-founder and chief technology officer, who sold shares both before and after the bullish September 2011 analyst meeting.

At that meeting, said Ms. James, the Dougherty & Co. analyst, executives were “so annoyed” when she asked how the company was going to take costs out of its manufacturing process. “It seemed to me they didn’t really know how they were going to do that,” said Ms. James, who initiated coverage of A123 stock in January 2012 with a “neutral” rating.

In its presentation at the meeting, A123 said it had reached a “business inflection point” and expected revenue to double by the end of the year. One slide said the company had a “strong business pipeline with customer activity in all target markets.”

Mr. Riley told the group that A123’s “research and development success is the result of a world class team” and its “technology portfolio is a foundation for continued market leadership,” a copy of the presentation shows.

Mr. Riley was selling shares steadily at the start of each month, under a trading plan that had begun in July, two months before the analyst meeting. Such trading plans, known as 10b5-1 plans, exist to let insiders avoid suspicion of insider trading when they buy or sell their own company’s stock, by following schedules calling for trades at certain prices or times. Insiders needn’t disclose the plans or any changes to them, and the plans generally become known only if mentioned in a trade report to the SEC.

Filings show Mr. Riley sold a total of about $720,000 of stock under his trading plan from July to December 2011, including $268,641 of stock in October through December 2011 after the bullish analyst meeting.

On Dec. 21, A123 disclosed it had manufacturing problems with its batteries, and “certain hose clamps may have been positioned incorrectly during assembly.” This could lead to coolant leaks, and “an electrical short could occur possibly resulting in a fire,” it said in a regulatory filing.

Its largest customer, electric-car company Fisker Automotive Inc., issued a recall for cars with the faulty batteries. In a bankruptcy filing, the company said “the problem required significant management time and expense.” A later manufacturing glitch cost the company more than $51.6 million.

Mr. Riley didn’t respond to requests for comment about his share sales. A123 said insiders who sold under trading plans conformed to its requirement that they wait a period of months after setting up the plans before trading under them.

Last August, A123 struck a deal to sell itself to a Chinese auto-parts manufacturer, but this eventually fell through after members of Congress and the Obama administration objected because A123 had received government grant money. On Oct. 16—having missed a bond-interest payment and with the Chinese deal in jeopardy—A123 said it would file for bankruptcy protection.

After the filing, a bankruptcy court approved a new deal for the Chinese company, Wanxiang Group, to acquire the bulk of A123’s assets.

Between the initial August agreement with Wanxiang and the October bankruptcy filing, investor North Bridge Venture Partners, which was a large enough shareholder in A123 to have a representative on its board, bailed out. The board member, Jeffrey McCarthy, sold roughly $2 million of shares on behalf of North Bridge from Aug. 29 to Sept. 10 at an average price of 23 cents. Neither Mr. McCarthy nor North Bridge returned calls seeking comment.

On the day in October when the battery maker filed for bankruptcy protection, its shares fell 75% to six cents apiece.