Hedge Funds Are for Suckers

July 12, 2013 Leave a comment

Hedge Funds Are for Suckers

By Sheelah Kolhatkar on July 11, 2013

At the height of the financial crisis in 2008, a group of famous hedge fund managers was made to stand before Congress like thieves in a stockade and defend their existence to an angry public. The gilded five included George Soros, co-founder of the Quantum Fund; James Simons of Renaissance Technologies; John Paulson of Paulson & Co.; Philip Falcone of Harbinger Capital; and Kenneth Griffin of Citadel. Each man had made hundreds of millions, or billions, of dollars in the preceding years through his own form of glorified gambling, and in some cases, the investors who had poured money into their hedge funds had done OK, too. They were brought to Washington to stand up for their industry and their paychecks, and to address the question of whether their business should be more tightly regulated. They all refused to apologize for their success. They appeared untouchable.

What’s happened since then is instructive. Soros, considered by some to be one of the greatest investors in history, announced in 2011 that he was returning most of his investors’ money and converting his fund into a family office. Simons, a former mathematician and code cracker for the National Security Agency, retired from managing his funds in 2010. After several spectacular years, Paulson saw performance at his largest funds plummet, while Falcone reached a tentative settlement in May with the U.S. Securities and Exchange Commission over claims that he’d borrowed money from his fund to pay his taxes, barring him from the industry for two years. Griffin recently scaled back his ambition of turning his firm into the next Goldman Sachs (GS) after his funds struggled to recover from huge losses in 2008.

As a symbol of the state of the hedge fund industry, the humbling of these financial gods couldn’t be more apt. Hedge funds may have gotten too big for their yachts, for their market, and for their own possibilities for success. After a decade as rock stars, hedge fund managers seem to be fading just as quickly as musicians do. Each day brings disappointing headlines about the returns generated by formerly highflying funds, from Paulson, whose Advantage Plus fund is up 3.4 percent this year, after losing 19 percent in 2012 and 51 percent in 2011, to Bridgewater Associates, the largest in the world.

This reversal of fortunes comes at a time when one of the most successful traders of his time, Steven Cohen, founder of the $15 billion hedge fund firm SAC Capital Advisors, is at the center of a government investigation into insider trading. Two SAC portfolio managers, one current and one former, face criminal trials in November, and further charges from the Department of Justice and the SEC could come at any moment. The Federal Bureau of Investigation continues to probe the company, and the government is weighing criminal and civil actions against SAC and Cohen. Cohen has not been charged and denies any wrongdoing, but the industry is on high alert for the possible downfall of one of its towering figures.

Despite all the speculation and the loss of billions in investor capital, Cohen’s flagship hedge fund managed to be the most profitable in the world in 2012, making $789.5 million in the first 10 months of the year, according to Bloomberg Markets. His competitors haven’t fared as well. One thing hedge funds are supposed to do—generate “alpha,” a macho term for risk-adjusted returns that surpass the overall market because of the skill of the investor—is slipping further out of reach.

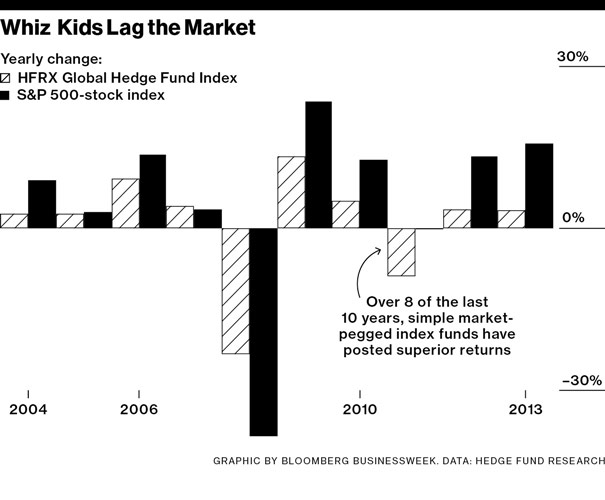

According to a report by Goldman Sachs released in May, hedge fund performance lagged the Standard & Poor’s 500-stock index by approximately 10 percentage points this year, although most fund managers still charged enormous fees in exchange for access to their brilliance. As of the end of June, hedge funds had gained just 1.4 percent for 2013 and have fallen behind the MSCI All Country World Index for five of the past seven years, according to data compiled by Bloomberg. This comes as the SEC passed a rule that will allow hedge funds to advertise to the public for the first time in 80 years, prompting a flurry of joke marketing slogans to appear on Twitter, such as “Creating alpha since, well, mostly never” (Barry Ritholtz) and “Leave The Frontrunning To Us!” (@IvanTheK).

Hedge funds are built on the idea that a smarter guy (and they are almost all guys; only 16.8 percent of managers are women) with a better computer can make miracles possible by uncovering inefficiencies in the market or predicting the future. In pure dollar terms, there are more resources, advanced degrees, and computing firepower devoted to chasing this elusive goal than almost any other endeavor, and that may include fighting wars. Yet traders face the immutable fact that every second, each megabyte of information, blog post, one-line rumor, revenue estimate, or new product order from China has already been taken into account by the efficient market and reflected in a security’s price. This means that trying to gain what traders call an “edge,” at least legitimately, is almost impossible. As the financial incentives on Wall Street have become enormous, so have the competition and pressure to gain an advantage at any cost.

Few people will shed tears for an industry that has produced more than its fair share of billionaires—some of whom, like Cohen, are notorious for their displays of wealth. Nevertheless, the decline of hedge funds has implications beyond Wall Street. The financial kingpins who profited most from hedge funds’ golden age gained the ability to make influential political donations and to bend big banks to their will. In the U.S., hedge funds manage a significant portion of pension funds and university endowments. For investors who chased the colossal returns once promised, the downturn may well bring painful losses. But it could also be the beginning of a virtuous cycle. If it’s going to survive, the industry may need to get smaller and a lot more modest.

Hedge funds began as a small, almost sideline, service. They were the alternative investments for the wealthy, intended to perform differently than the overall market. “Any idiot can make a big return by taking a big risk. You just buy the S&P, you lever up—there’s nothing clever about that,” says Sebastian Mallaby, the author of More Money Than God: Hedge Funds and the Making of a New Elite. “What’s clever is to have a return that’s risk-adjusted.”

This is what Alfred Winslow Jones, an Australian-born onetime financial journalist, had in mind in 1949 when he created a private investment partnership that was designed to be “hedged” against gyrations in the market. Jones borrowed shares, sold them short, and hoped to earn an offsetting profit on them if the market dropped and his long positions lost value.

It didn’t come without risks: Shorting exposes an investor to potentially limitless losses if a stock keeps rising, so regulators decided that only the most sophisticated investors should be doing it. Hedge funds would be allowed to try to make money almost any way they wanted, and charge whatever fees they liked, as long as they limited their investors to rich people who, in theory, could afford to lose whatever money they put in. It was a side bet.

For a while, the funds were expected to produce steady, modest returns, in contrast to the wider swings of the market. In a 2011 paper that he updated this year, Roger Ibbotson, a finance professor at the Yale School of Management who runs a hedge fund called Zebra Capital Management, analyzed the performance of 8,400 hedge funds from 1995 to 2012; he concluded that on average they generated 2.5 percent of precious alpha. “They have done a good job, historically,” Ibbotson says. “Now, I think it’s overcapacity. I doubt that the alphas are completely gone, but alphas are going to be harder to get in the future than they have been in the past.”

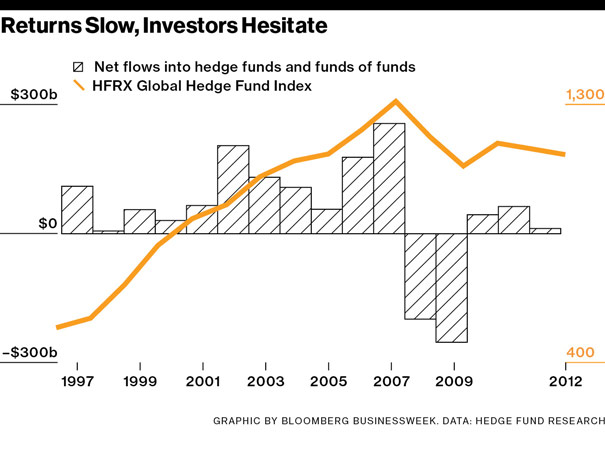

With each millionaire-minting stock market boom, the number of hedge funds has increased as the rich scour the market for new ways to get even richer. It’s no coincidence that the first decade of the 21st century, when the wealthiest 0.1 percent became exponentially wealthier, marked the high-water mark for hedge funds. Now there are about 10,000 hedge funds managing $2.3 trillion. The pioneers, such as Cohen and Paulson, had learned that working at investment banks with their brutal hours and byzantine corporate cultures—not to mention the fighting over bonuses every January—was for suckers. Hedge funds offered would-be financial hotshots a faster and more glamorous path to obscene wealth.

One of the most alluring aspects of the business vs. other sectors of Wall Street is what people in the tech world call “scalability.” Hedge fund managers could easily expand their annual bonuses from millions a year to tens of millions or more just by bringing in more investor money and making the fund larger, often with little extra work. Most hedge funds charge a management fee of 2 percent of assets, which is intended to cover expenses and salaries, as well as 20 percent of the profit generated by the fund at the end of the year. A fund managing $300 million would take $6 million in fees, plus its 20 percent cut; if the fund grew to $3 billion in assets, the management fee would jump to $60 million. If a fund of that size returned only 6 percent that year, it would generate $180 million in profit, $36 million of which the managers could keep. It quickly starts to look like a smart use of a Harvard degree.

Yet this once hugely lucrative model has proven unsustainable. One chief investment officer at a $5 billion institution breaks down the typical hedge fund life cycle into four evolutionary stages. During the early period, when a fund is starting out, its managers are hungry, motivated, and often humble enough to know what they don’t know. This tends to be the best time to put money in, but also the hardest, as the funds tend to be very small. Stage two occurs once the fund has achieved some success, when those making the decisions have gained some confidence but they aren’t yet so well-known that the fund is too big or impossible to get into.

Then comes stage three—the sort of plateau before the fall—when the fund gets “hot” and suddenly has to beat back investors, who tend to be drawn to flashy success stories like lightning bugs to an electric fence. Stage four occurs when the fund manager’s name is spotted as a bidder for baseball teams or buyer of zillion-dollar Hamptons mansions. Most funds stop generating the returns they once did by this stage, as the manager becomes overconfident in his abilities and the fund too large to make anything that could be described as a nimble investing move. “The bigger a fund gets, the more difficult it gets to maintain strong performance,” says Jim Kyung-Soo Liew, assistant professor in finance at the Johns Hopkins Carey Business School. “That’s just because the number of opportunities is limited in terms of putting that much money to work.”

Hedge funds have also been hurt by their success. Most of the advantages their investors once had—from better information to far fewer people trying to do what they do—have evaporated. In the easy, early days, there was less than $500 billion parked in a couple thousand private investment pools chasing the same inefficiencies in the market. That’s when equities were traded in fractions rather than decimals and before the SEC adopted Regulation FD, which in 2000 tightened the spigot of information flowing between company executives and hungry traders.

After 2000, the supposed “smart” money began paying expert network consultants—company insiders who work as part-time advisers to Wall Street investors—to give them the information they craved. The government has since cracked down on that practice, which in some cases led to illegal insider trading. The rise of supercharged computer trading means speed is one of the few ways left to gain an advantage.

As their returns have fallen, the biggest hedge funds have started to seem more like glorified mutual funds for the wealthy, and those rich folks might start to take a harder look at whether they’re getting their money’s worth. This could be an encouraging development for the world economy, considering that hedge funds provided huge demand for the toxic mortgage derivatives that helped lead to the financial collapse of 2008. At the same time, the tens of billions that pension funds have plowed into funds such as Bridgewater’s All Weather Fund—down 8 percent for the year as of late June, according to Reuters, compared with a 10.3 percent rise in the S&P 500—mean that the financial security of untold numbers of retirees could be threatened by a full-scale hedge fund meltdown.

For the moment, that possibility seems remote. The age of the multibillionaire celebrity hedge fund manager may be drawing to a close, but the funds themselves can still serve a useful purpose for prudent investors looking to manage risk. Let the industry’s recent underperformance serve as a reality check: No matter how many $100 million Picasso paintings they purchase, hedge fund moguls are not magicians. The sooner investors realize that, the better off they will be.