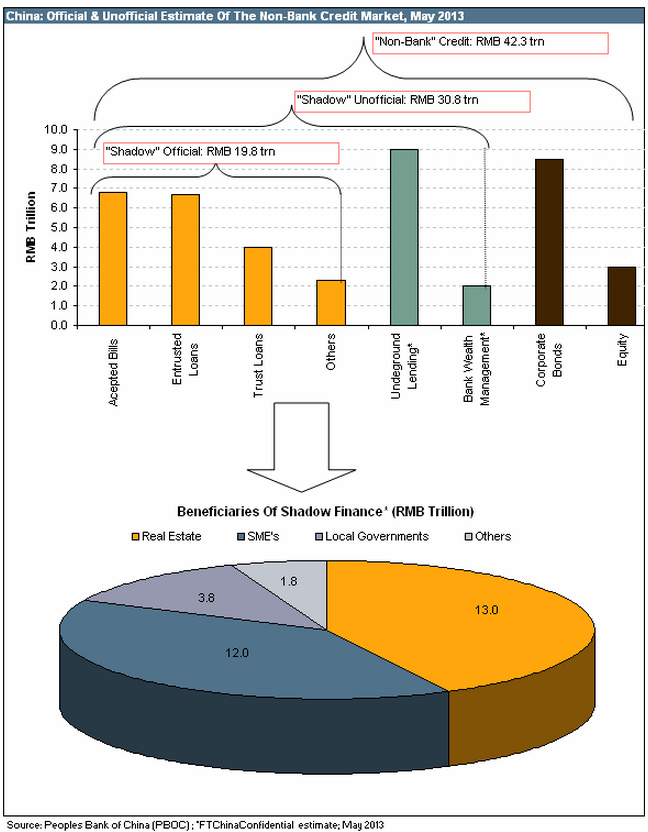

Shadow financing charted in China; At least 50% of the debt on smaller developer balance sheets would be from trust financing, funding construction at initial stages which puts the company and the trust at redemption risk

July 12, 2013 Leave a comment

Shadow financing charted in China, and a property catch-up

| Jul 11 11:18 | 10 comments | Share

Part of the UP SHIBOR CREEK… SERIES

You’ll note that real estate is where a significant amount of the credit apparently flows and thus quite a bit of the risk resides — property developers, particularly the small ones, have had to go begging to trust companies and underground lenders at interest rates usually in the low to mid teens and for something like 6 months to two years. The duration mismatch is pretty obvious.The property market has benefited from relatively easy refinancing in the shadow market which has kept the liability mismatch as an ironically distant fear — particularly as property prices rose, and shadow banking products such as WMPs and trust companies were assumed to benefit from a state guarantee.

China’s powers-that-be deigning to notice that a load of credit growth was happening outside of their control — Shibor has come back in since kicking up to 13 per cent or so but their message stands — changes that and has quite a few people spooked.

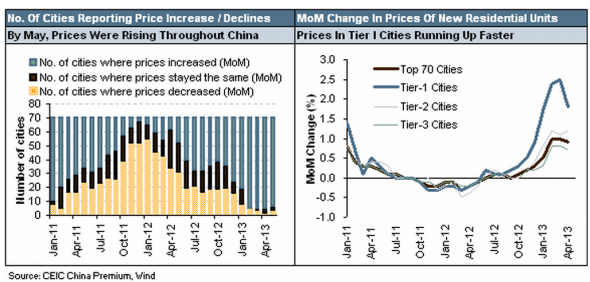

The actual impact of shadow financing of real estate also supports and drives other sectors dependent on housing. As CreditSights said, it’s no real surprise that shadow lending practices have mostly sprouted about in large Tier I/II cities, which have seen rapidly rising prices.

From CS again (our emphasis):

The consensus is that at least 50% of the debt on smaller developer balance sheets would be from trust financing. What worries us more is that much of this is funding construction at even initial stages, which automatically puts the company and the trust company at redemption risk. There have not been any defaults or evidence of stress so fa, but then again, issuance has been surging. The suggestion that issuance will continue to surge as real estate demand and prices keep rising is probably correct, but certainly not comforting…

A basic run through the balance sheet of 127 property developers listed on the Shanghai Stock Exchange reveals that short term debt is on average 40-50% of their total debts, and cast rarely ever covers these commitments. If banks start to play hard-ball as the PBOC may want them to, or more worryingly, if trust funding is a big component of their debts (as is suggested) and if issuance retreats, then refinancing pressure would increase. Clearly, much depends on regulatory action/ inaction.

As Michael Pettis said near the end of June, “the PBoC has almost no experience of any kind of financial market condition except that of soaring money creation and credit expansion. Until last year they have never had to deal with a stable or even contracting money supply, and consequently they have had little experience in dealing with these kinds of conditions.” Simply the fact that the PBOC is looking at this market is enough to warrant caution.