China Falters in Effort to Boost Consumption; Growth in Urban Households’ Disposable Income Slows, Hindering Beijing’s Plan to Cut Emphasis on Unreliable Exports

July 16, 2013 Leave a comment

Updated July 15, 2013, 8:51 p.m. ET

China Falters in Effort to Boost Consumption

Growth in Urban Households’ Disposable Income Slows, Hindering Beijing’s Plan to Cut Emphasis on Unreliable Exports

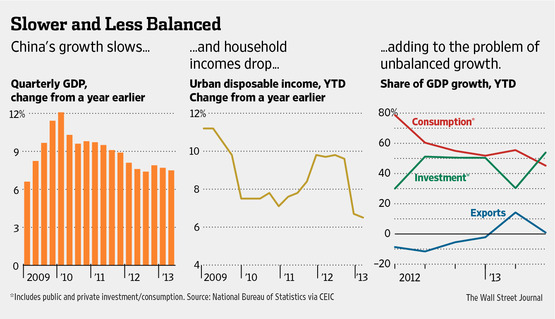

BEIJING—China’s push to get consumers to open their wallets more and refocus the economy on domestic consumption is stalling, contributing to lower growth in the second quarter and forecasts of even slower momentum ahead. A slew of data released on Monday showed that disposable income growth for urban households slowed to 6.5% in the first half compared with a year ago, down from 9.7% growth in the first half of 2012 and below the growth rate of the economy as a whole. That contributed to a slide in the share of consumption in China’s growth—the reverse of the government’s plans. Salary increases are “getting slower and slower,” said Peter Zhou, a 29-year-old manager at an information-technology company, who saw his income eke out a meager 3.7% increase to 28,000 yuan a month ($4,500) in 2013. “We used to buy consumer electronics and jewelry every month,” he said, but now he hasn’t made a big-ticket purchase for three months.Higher incomes are critical to remaking the Chinese economy so it depends more on domestic consumption and less on increasingly unreliable exports and investment in capital-intensive industries. Spending by China’s growing middle class, economists inside and outside of China have argued for years, should provide a firmer foundation for long-term growth.

Growth in China’s retail sales edged up in June. But in another sign of slow progress, for the first half as a whole it rose 12.7% year-on-year, down from 14.4% in the same period in 2012.

China’s new leaders have said repeatedly that they are willing to take a hit when it comes to short-term growth in order to carry out such a transition. But so far they have delivered the slower growth, not the structural adjustment.

Sheng Laiyun, a spokesman for the National Bureau of Statistics, warned that after 30 years of rapid growth the Chinese economy had entered a new phase. “Without breakthroughs in technology, the same inputs are producing smaller outputs,” he said.

China’s economic growth decelerated to 7.5% in the second quarter compared with a year earlier, down from 7.7% in the first quarter, the government’s statistics bureau said on Monday. Most economists now expect growth for the year of around 7.5%, which would be the slowest since 1990.

On a quarter-on-quarter annualized basis—the way growth is reported in the U.S.—the economy accelerated slightly to 6.9% year-on-year, up from 6.6% in the first quarter, according to Wall Street Journal calculations based on official data. But that pace was below the government’s 7.5% target for the year.

After China reported the disappointing results, Nomura downgraded its forecast for 2014 growth to 6.9% growth from 7.5%. It cited slow progress in restructuring the economy, among other factors. J.P. Morgan, meanwhile, reduced its 2014 forecast to 7.2% from 7.7%. Last month Barclays said it thought growth in China could fall to 3% or below within the next three years—though it figured China “would bounce back dramatically” in such an event.

Cautious consumers have thrown China back on its old reliance on investment spending to drive growth. Consumption contributed 45.2% to GDP growth in the first half of the year, down from 60.4% in the first half of 2012. Domestic investment—spending on factories, real estate and infrastructure— increased its share to 53.9% from 51.2% over the same period.

Zeng Qinzhao, a manufacturer of computer parts for companies like Sony Corp. in the east coast city of Xiamen, has been trying—without success—to make the kind of transition the government has sought. He says rapid wage growth and a stronger yuan was eroding China’s manufacturing competitiveness, and he decided to diversify.

But with the economy fragile, he has sharply scaled back his plans to launch a chain of fried chicken restaurants. “I opened 10 restaurants,” said Mr. Zeng, instead of making a big splash with 50 outlets. “All of them have been losing money” in the slowing economy, he added.

At the beginning of the year, top leaders were promising a renewed crackdown on the bubbly real-estate sector to limit the chance of a debilitating crash. Now, the housing build out is one of the few things keeping the economy ticking over.

The area of new residential property under construction rose 2.9% year-on-year in the first half of 2013, a turnaround from contraction in 2012. That has come at a cost, with real estate prices in Beijing and Shenzhen clocking double digit gains and other major cities not far behind, taking the dream of homeownership further out of reach for many first-time buyers.

There are indications that China’s leaders are beginning to get antsy about slower growth and may look to pull some levers to rev up GDP—or at least to prevent it from falling further. During a recent tour of south China, Premier Li Keqiang said that “economic operations should be managed in such a way that ensures that the growth rate, employment and other indicators don’t slip below the lower limit.”

He didn’t specify those limits, but an increasing number of economists think that China may not meet its 7.5% growth target. That would be a first after 15 years of hitting the mark.

At a meeting last Friday of the State Council, China’s top government body, Mr. Li said China should focus investment on energy efficiency and information technology as a way to boost growth. While he said that would also speed up the pace of reform, the government selection of favored industries smacks of old-style “industry policies instead of more fundamental structural reforms,” said a research note from Bank of America.

At a government meeting in Beijing on Monday, central bank Gov. Zhou Xiaochuanurged financial institutions to boost lending to the nation’s smaller companies and urged those companies to issue bonds as a way to get credit, according to a statement released after the meeting.

Government officials now are putting together an economic-restructuring plan that’s due to be released at a Communist Party conclave in October. That process continues, although some academics say opposition from vested interests may limit the depth of the changes. For instance, a plan to guide urban growth so it gives rural migrants more social benefits—seen as crucial to increasing labor force participation and raising consumption—has stalled because of opposition from some provincial leaders, say academics who are consulting on the plan.

The greatest threat to economic restructuring would be a rise in unemployment, which would prompt leaders to do whatever they could to boost growth quickly. So far, China’s labor markets have remained robust.

Mr. Sheng, the NBS spokesman, said that China’s cities created more than seven million new jobs in the first half, and the number of migrant workers leaving farms for factories continued to grow.

“China’s economy will continue the downward trend in the third quarter, but Beijing won’t loosen monetary policy” in a bid to lift growth, said a researcher tied to the powerful National Development and Reform Commission, adding that the government would turn instead to greater public spending.

Whether greater stimulus would work is an open question. “You can stimulate the economy, but the inflationary effect will be much higher” than it was in the past, said Yu Yongding, a senior Chinese economist and former adviser to the central bank.

“You also need to worry about asset bubbles,” Mr. Yu added.