Retailers in the rich world are suffering as people buy more things online. But they are finding ways to adapt

July 16, 2013 1 Comment

Retailers in the rich world are suffering as people buy more things online. But they are finding ways to adapt

Jul 13th 2013 |From the print edition

“THE staff at Jessops would like to thank you for shopping with Amazon.” With that parting shot plastered to the front door of one of its shops, a company that had been selling cameras in Britain for 78 years shut down in January. The bitter note sums up the mood of many who work on high streets and in shopping centres (malls) across Europe and America. As sales migrate to Amazon and other online vendors, shop after shop is closing down, chain after chain is cutting back. Borders, a chain of American bookshops, is gone. So is Comet, a British white-goods and electronics retailer. Virgin Megastores have vanished from France, Tower Records from America. In just two weeks in June and July, five retail chains with a total turnover of £600m ($900m) failed in Britain.Watching the destruction, it is tempting to conclude that shops are to shopping what typewriters are to writing: an old technology doomed by a better successor. Seattle-based Amazon, nearing its 19th birthday, has lower costs than the vast majority of bricks-and-mortar retailers. However many shops, of whatever remarkable hypersize, a company builds in the attempt to offer vast choice at low prices, the internet is vaster and cheaper. Prosperous Londoners and New Yorkers ask themselves when was the last time they went shopping; their shopping comes to them. “Retail guys are going to go out of business and e-commerce will become the place everyone buys,” pronounces Marc Andreessen, a celebrity venture capitalist. “You are not going to have a choice.”

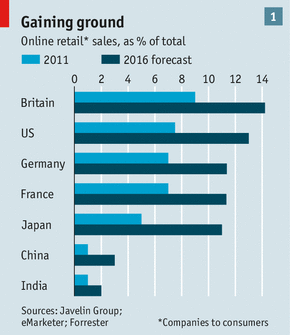

Online commerce has grown at different rates in different countries, but everywhere it is gaining fast (see chart 1). In Britain, Germany and France 90% of the rather modest growth in retail sales expected between now and 2016 will be online, predicts AXA Real Estate, a property-management company.

Old dog, meet new tricks

This would hurt less if shoppers were spending more; smaller slices are more acceptable when they come from bigger pies. But in many rich countries, especially in Europe, consumers are still smarting from the bursting of the credit bubble and high unemployment. American consumers are perkier, but seem to be clinging to the bargain-hunting habits of the recession. Services have been consuming a bigger share of their wallets for decades, leaving less to spend on things (see chart 2). Ageing populations could shrink the pie further. Old people shop less.

When shoppers both know what they want and are willing to wait for it they will go online. And retail’s simple moneymaking ways of yesteryear—find a catchy concept, fuel growth by opening new shops and attracting more shoppers to existing ones, use your growing size to squeeze suppliers for better margins—have run out of steam. But that does not mean that there are no new options for bricks and mortar.

Shopping is about entertainment as well as acquisition. It allows people to build desires as well as fulfil them—if it did not, no one would ever window-shop. It encompasses exploration and frivolity, not just necessity. It can be immersive, too. While computer screens can bewitch the eye, a good shop has four more senses to ensorcell. No one makes the point better than Apple; in terms of sales per unit area its showrooms-slash-playrooms best all other American retailers.

And shops make money. Bricks-and-mortar retail may be losing ground to online shopping, but it remains more profitable. The physical world is also increasingly capable of taking the fight to its online competitors. Last year online sales of shop-based American retailers grew by 29%; those of online-only merchants grew by just 21%. Apart from Amazon—which has long spurned profits in favour of growth—most pure-play online retailers are losing market share, says Sucharita Mulpuru of Forrester Research. The bricks-and-mortar retrenchment will be painful, but the survivors may make shopping a less formulaic, more satisfying and possibly even more profitable experience, both offline and on.

Many brands still think shops are the best way to attract customers. Inditex of Spain, owner of the ubiquitous Zara fashion brand, opened 482 stores in 2012, bringing its total to 6,009 in 86 countries. Primark, a fast-growing vendor of nearly disposable clothing, sells nothing on its website, relying on its 242 shops for almost all its sales. The same can hold at the luxury end, too—few will buy a $10,000 necklace online, or entrust it to the post. Space on the snazziest streets in London, Paris and New York is in such demand that luxury retailers pay millions in “key money” to secure it, says Mark Burlton of Cushman & Wakefield, a property company.

Offline-only, though, is a shrinking category. Now that the initial shock of the online onslaught has worn off, most big retailers have joined it. They proclaim themselves to be “omnichannel” merchants, as adept as Amazon online but with the added excitement and convenience that comes with physical shops. Philip Clarke, chief executive of Tesco, Britain’s largest retailer, says that app development will come to be as important to his company as property development. Walmart, the world’s biggest retailer, has 1,500 employees in Silicon Valley trying to out-Amazon Amazon in areas such as logistics and making the most of social media.

Some online natives are going omnichannel, too. Pace Mr Andreessen, New York-based Warby Parker, which sells trendy spectacles at prices lower than those charged by famous brands, has opened 14 shops, one of them a school bus that tours the country. Some potential customers were wary of buying spectacles from an online-only merchant. “We thought bricks and mortar would bring gravitas to the brand,” says Neil Blumenthal, a co-founder. Its SoHo flagship resembles a library. Appointments with the in-store optometrist are displayed on a railway-station-style time board.

Currying favour

Britain may be one of the places where the future of retail is most easily seen. Online shopping has advanced further there than in other developed economies. The population is quite tightly packed, which makes delivery relatively cheap, and 70% have broadband internet access. It is one of the few places where online grocery shopping has taken off. Eventually, predicts Panmure Gordon, an investment bank, 20% of the food business will be online. For non-food items it will average 40%, but there will be a large range. For entertainment it may be 90%; for DIY supplies as little as 15%.

Footfall on British high streets has declined for seven years running. Citi Research, part of Citigroup, a bank, calculates that comparable sales at a representative selection of Britain’s clothing chains fell by 3-5% a year between 2009 and 2012. Shop rents are high and leases are long, which piles on the pressure. Vacancy rates have risen fivefold to 14% since 2008. A report by the Centre for Retail Research predicts that a fifth of Britain’s high-street shops will close over the next five years, eliminating more than 300,000 jobs.

Britain’s brick-burdened retailers may be heartened, though, by the example of Dixons Retail, owner of Britain’s biggest electronics and computer retailers, Currys and PC World, and of similar chains in other countries. Between 15% and 20% of sales at Dixons are online, depending on the season, and the proportion is rising. But Dixons thinks the advantages which online-only merchants get by doing away with shops and sales staff are undercut by the need to pay more than high-street shops do to acquire customers (largely by paying Google for clicks on adverts) and to spend a lot on shipping. So instead of doing away with shops and sales staff, Dixons is trying to get more out of them.

Shoppers may be tempted to treat electronics stores as showrooms for Amazon and its like, but at least they cross a retailer’s threshold at some point during their quest 90% of the time, notes Dixons’ boss, Sebastian James—and with rivals like Comet having closed down, that threshold is ever more likely to be Dixons’. This gives the company the means to procure better terms than online rivals do from its suppliers, which like the idea of customers actually seeing their wares in the flesh, shown off by flesh-and-blood people. Sometimes, as with a recent AEG washing machine and Samsung camera, Dixons enjoys a period of exclusivity.

Thus people’s tendency to use the shops as showrooms is turned, at least in part, to the company’s advantage. Other retailers are seeking to embrace the practice too. Best Buy, America’s biggest electronics retailer, used to cover up barcodes to stop shoppers from using their phones to compare prices. Today the retailer’s new boss, Hubert Joly, professes to “love showrooming” because it means that a prospective customer is on the premises.

Having people on the premises also helps Dixons to bundle sales—in particular, to sell high-margin accessories and services along with low-margin devices. Mr James says that computers in Dixons were 26% more expensive than on Amazon three years ago. Now the difference is pretty much zero. So the shops must make money by selling “the world that goes around the product”—like a computer bag or high quality cables.

These stratagems depend on having attractive stores and able shop assistants. Dixons has retrained its staff and changed their incentives. Individual sales commissions have been scrapped in favour of store-wide schemes linked to measures of customer satisfaction. To overcome managers’ reluctance to refer customers to the website, stores are now credited with all sales in their catchment area, regardless of whether a buyer entered the premises.

The omnichanneller’s dilemma

But though owning shops is basic to Dixons’ strategy, the number of shops is dropping, and will drop further. Dixons has cut its British network from 780 to 486; it aims to end up with just under 400. Jessops, which has been reopened after shedding more than 80% of its stores by Peter Jones, a flamboyant reality-television entrepreneur, is making a similar bet.

For many retailers, such reductions are an inescapable part of going omnichannel. “You’re putting in more capital to keep the sales you have,” says Colin McGranahan of Sanford C. Bernstein, a research firm. Investment which used to go mainly into new stores must now in part be redirected towards the technology and distribution that online sales require. And sales through new channels come in part at the expense of existing shops, the costs of which are largely fixed. That depresses the retailer’s profits and forces it to close shops.

Other sectors have some advantages over electronics and camera sales. It is not so easy for shoppers to use food and clothing shops—both of which are big parts of retail—as showrooms for online sales. You cannot squeeze a melon with a tablet computer; phones make poor fitting rooms.

For online-only retailers such products cause extra headaches. Clothes shoppers return a quarter or more of the garments they buy. Selling groceries online is laborious, with lots of low-value items stored at different temperatures that have to be assembled into all manner of unique orders and then delivered rapidly.

But online-only retailers keep inventing clever ways to overcome such disabilities. Amazon’s “subscribe and save” service delivers at regular intervals staple products like nappies and coffee. Fits.me sets up “virtual fitting rooms” for online clothiers, which let shoppers enter their measurements to see how garments would look on them. Citi Research expects British online clothing sales to double in the next six years. “There are no glass ceilings on any particular category,” says Robin Terrell, head of Tesco’s online business.

For Tesco, the world’s third-biggest retailer, the challenge of mastering online grocery while shoring up its traditional business is acute. The company outsells all other British grocers on the internet; but its market share has been slipping both online and off and a recent poll rated its shops lower in quality than those of any other British grocer. Like Carrefour, the French firm that is retail’s global number two, Tesco has pulled back from some attempts to expand internationally in order to win back lost ground at home.

Change in store

Around 40% of Tesco’s British floorspace is in hypermarkets which seem ill suited to new trends, based as they partly are on the idea of selling things that people would rather buy online, such as televisions, alongside food. The Institute of Grocery Distribution, an industry think-tank, sees sales in Britain’s big shops growing by just 6.4% between 2012 and 2017. The growth that is not found online is going to come from neighbourhood convenience shops, which the institute sees as growing by 28.5% over the same time. So that is where Tesco, like Carrefour and Walmart elsewhere, is heading. In April Tesco took an £804m write down on the value of its British property as it scaled back plans for future big supermarkets.

After a decade spent bringing its shops online Tesco now sees it as time to “bring the internet into stores”, says Mike McNamara, the company’s technology chief. The idea is that this will make shops both more productive and more popular. Tesco’s in-store cafés could have interactive tabletops, which, prompted by a customer’s cellphone, would suggest recipes based on his shopping list. Similar wizardry could tell staff which fruit and vegetables need replenishment. The hypermarkets will also sell more clothing and cosmetics, which have higher margins than electronics and seem a more natural fit with food.

Online sales are the fastest-growing part of Tesco’s business, but analysts doubt they bring much profit. “On a fully costed basis no one makes money” in online grocery, says Andrew Gwynn of Exane, an investment company. But online offers a real advantage in serving Tesco’s most loyal and profitable customers. Tesco has been hoovering up information through its Clubcard loyalty scheme for years; computers can take that further. “We are teetering on the brink of an era of mass personalisation,” says the retailer’s boss, Mr Clarke. Loyal customers are worth far more to Tesco than footloose ones.

Deep personalisation could have disruptive consequences. Retailers are beginning to see profit per household, rather than per square metre, as the thing they should target, according to the Boston Consulting Group. Safeway, an American supermarket, offers individualised pricing through its “just for u” loyalty scheme. Mr Clarke seems wary. Tesco “should be classless”, he says, meaning it should not discriminate among its customers. But the temptation will be there. Tesco still uses traditional yardsticks but “customer-level metrics” will challenge the way the company thinks, says Mr Terrell.

Many chains are going through similar change, looking again at every aspect of their logistics (a 95% accuracy rate is acceptable for shipments to grocery shops but anything short of 100% risks turning off a customer), their staff training, the number, size and location of their shops and what they offer the customer. Asda, a competitor to Tesco in Britain that is owned by Walmart, is transforming big supermarkets into “mini high streets”, bringing in Disney shops and shoe repairs (Tesco has bought Giraffe, a restaurant chain, for similar purposes). John Lewis, a British omnichannel role model, takes the view that targeting individual shoppers rather than single channels is the way to profitability. “Click and collect” services let shoppers pick up online purchases at a convenient store where they might also buy something else.

The future shopscape will be emptier, but more attractive. Shoppers can expect new rewards for simply showing up. Shopkick, a mobile-phone app, gives American shoppers points that earn them goodies like iTunes songs just for stepping across the threshold of a participating store. Inspired by Apple, shops promise “experience” and hope that sales will follow. Germany’s Kochhaus claims to be the first food store organised around recipes rather than grocery categories. The ingredients are strewn across tables, not stacked on shelves. Some shops will opt to sell nothing at all on the premises. Desigual, a Spanish fashion merchant, has shops in Barcelona and Paris that carry only samples. Shoppers are helped to assemble them into outfits that they then buy online.

Shopping centres are reallocating space from the classic form of retailing to leisure and entertainment. In Britain the non-retail share of shopping-centre revenue has risen from the 5% once seen as standard to 10-15% and could rise to 20% over the next five years, says the British Council of Shopping Centres. The same trend holds across much of Europe. In America nearly a quarter of the space in shopping centres is occupied by businesses other than shops and restaurants. Medical services may become principal attractions, says Michael Niemira of the International Council of Shopping Centres. Health care accounts for just 1% of space now but Mr Niemira and others expect it to “explode”.

Room for improvement

Nothing is settled. The bundles assembled by Dixons and its kind may be brutally unpicked by online competitors. A logistical arms race is heating up. Amazon, having given up its resistance to collecting state sales tax in America, is building fulfilment centres near cities to speed delivery. Bricks-and-mortar shops are striking back with services such as Shutl, which arranges fast home deliveries from store networks. And all retailers are competing increasingly with suppliers seeking new direct routes to market. Last year online sales by companies that make their own products grew faster than those of both shops and online-only retailers in America.

And new hybrids are emerging. Yihaodian, a Chinese company owned by Walmart, has used an app to let phone users visit 1,000 “virtual stores” accessible only at specific sites—many of which, rather cheekily, were on the doorsteps of rival retailers. Tesco’s Korean subsidiary, Homeplus, puts up images of products on posters in the subway; commuters can scan them to get the products delivered. Tangible and virtual retailing may meld in all sorts of unaccustomed ways. Even Amazon has flirted with the idea of opening physical stores. Consumers have reason to cheer the survival of the sexiest.

Pingback: Alane