Are You Overpaying for Your Parents’ Care? Overseeing home health care for loved ones can be as big a drain on families’ resources as paying for institutional care.

July 20, 2013 1 Comment

July 19, 2013, 6:21 p.m. ET

Are You Overpaying for Your Parents’ Care?

Overseeing home health care for loved ones can be as big a drain on families’ resources as paying for institutional care. Here are some overlooked ways to trim the bill.

KELLY GREENE

A child’s work is never done—especially when it comes to caring for an elderly parent. Time isn’t the only cost. Families often spend a small fortune even before their loved ones check into a long-term-care facility. Making matters worse, adult children juggling jobs, caregiving and their own kids often miss ways to mitigate costs, from tax breaks to hiring home caregivers on their own. All told, needless expenditures can add up to thousands of dollars a year.In 2011 alone, the most recent data available, so-called informal caregivers provided at least 11.2 billion hours of unpaid care to family members and friends, according to a Congressional Budget Office report released in June. That commitment is expected to escalate: In 2010, about 4% of adults under age 65 were providing unpaid care to relatives or friends who were 65 and older. By 2050, demand for informal caregivers could double to 8% as the younger population shrinks relative to the elderly population.

Elderly people and their families also spent at least $3 billion on their own in 2011 on long-term care in the community, mainly at home, in addition to $36 billion on nursing homes and other long-term-care facilities, according to the CBO.

And those figures don’t necessarily include drugs not covered by Medicare and other unreimbursed expenses, such as food for special diets, increased utility costs, home renovations and special supplies.

One-third of adults 65 or older—and two-thirds of those who have reached their mid-80s—have functional limitations, ranging from needing help with eating and bathing to preparing meals or paying bills. Four out of five older adults who fit that description still are living in the community, rather than a nursing home, including many with three or more such needs, according to the CBO report.

Gary and Phyllis Hansen, who run a plumbing-and-heating business in Tracy, Minn., spent 11 years caring in their home for Ms. Hansen’s mother, who suffered from heart failure and dementia and died in June at age 95.

They installed a walk-in shower, paid other caregivers when Ms. Hansen needed to be in the office and temporarily checked her into a facility a few times—but they didn’t even seek out any tax breaks for the home renovations or medical expenses.

“If there were any deductions or anything like that we could have used, we didn’t know about it, and we didn’t have time to figure it out,” Mr. Hansen says. “We just paid for it.”

How can families cope with paying for more care at the same time they are stretched by the unpaid time they are spending providing it themselves? Here are some shortcuts for finding relief:

• Hire your own home-care professionals—or become one yourself.

Grown children turned caregivers who rely on paid help to fill in gaps when they have to work or sleep, or whose loved ones need round-the-clock care to help with tough physical tasks, often turn to an agency first. Then, when they have a feel for what they want in such workers and how to find them, many do the hiring directly.

That way, they have more control over the people taking intimate care of their family member, and they also can cut costs, since there are no administrative fees.

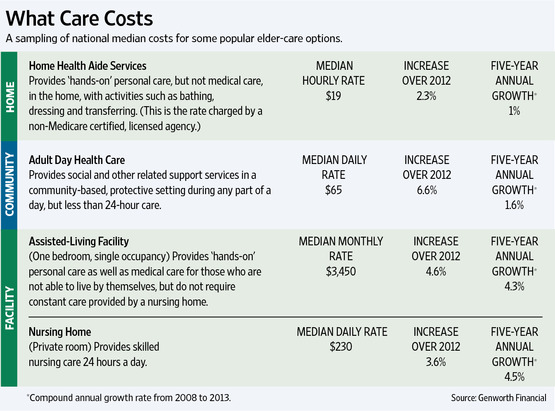

The national median rate for home care through a licensed agency is $19 an hour, up 2.3% from 2012, according to insurer Genworth Financial‘s GNW +0.30% annual survey of long-term-care costs.

Tom Meyer had taken out long-term-care insurance on his in-laws through his printing company in Walnut Creek, Calif., so he had some help paying for their home health care. Still, his in-laws wound up needing home care for about seven years, so Mr. Meyer and his wife sought ways to save money.

At first, the couple hired caregivers through two local agencies. But they went through about 20 workers before finding one who was qualified and personable, Mr. Meyer says. When she was transferred with no explanation, they decided to do the hiring themselves.

That alone cut their cost to $160 a day from $280, Mr. Meyer says.

There are caveats: Background checks are important, as is following state laws about working hours, disability insurance and payroll taxes, says William Upson, Mr. Meyer’s financial adviser.

If you provide caregiving help to your parents or in-laws and they have long-term-care insurance, you also may qualify for reimbursement, Mr. Upson says.

Mr. Meyer’s in-laws had a policy that said a blood relative couldn’t get paid for that work—but relatives by marriage could. He had kept notes on a calendar of all the time he had spent caring for their home, mowing the yard and doing other chores, and Mr. Upson helped him make a case for payment.

Eventually, Mr. Meyer won some reimbursement for his time, he says.

• Take the tax breaks.

Many elder-care expenses qualify for a medical-expense deduction from federal income taxes. Although the threshold for taking that deduction rose to 10% from 7.5% of adjusted gross income this year, it remains 7.5% for people 65 and older. So it may make sense to have those expenses come from the older patient’s bank account, rather than an adult child’s, says Frank Salandra, a certified public accountant in Harrison, N.Y.

But note: If you hire paid caregivers on your own, rather than working through an agency, the parent has to report that caregiver’s income, either on a W-2 or 1099 form, to be able to deduct the expense, he says. The adult child can take deductions only if the parent is a dependent and the child pays, he adds.

Home improvements made with a doctor’s prescription are tax-deductible as well, and few families realize that, Mr. Salandra says.

Such remodeling could include adding an elevator, swimming pool, central air-conditioning or ramps, he says. The key: getting the doctor’s note and deducting only the amount “over and above the amount it increases the home’s value,” he says.

For example, if installing an elevator costs $50,000 but adds $10,000 to the home’s value, you could take a $40,000 deduction. That means either getting an appraisal of the total house before and after the improvement or getting a professional real-estate opinion, he says.

One other possible medical-expense deduction: entrance fees to a continuing-care retirement community, which provides care ranging from independent living to skilled nursing. The fees can run to more than $100,000.

• Designate a bookkeeper.

Just as people making a will need to decide who would handle their estate, people planning for later life should decide who should handle their finances in a health crisis, says Patricia Seaman, senior director of the National Endowment for Financial Education, a nonprofit group in Denver.

Among the elements the plan should include: designating who in the family should take control of the parent’s finances when needed; taking inventory of the parent’s resources; making sure the parent’s will and power of attorney are current; and pinpointing resources to pay for care costs.

• Remember the veterans.

One often-overlooked source of help available to millions of families of wartime veterans is the “aid and attendance” benefit, which pays up to $2,054 a month to married veterans who qualify. Single veterans and surviving spouses can qualify for smaller payments.

To qualify, veterans generally must have served at least 90 days of active military service, including at least one day during a war. There also are thresholds for medical and financial need, and the rules are stricter for younger veterans.

The good news: The income limits are met after deducting unreimbursed medical expenses, including any long-term-care expenses. So a middle-class family paying assisted-living or home-care costs frequently still qualifies, says Kevin Olison, a financial adviser in San Ramon, Calif.

Mr. Upson has helped a number of clients qualify, as well as his own father, a World War II veteran who had a stroke at age 71 and needed care for seven years, he says. “It’s been out there for years, and most people, especially veterans, don’t even know about it,” Mr. Upson says.

For help applying, go to www.va.gov, click on “Locations,” then on “State Veterans Affairs offices,” “Veterans Service Organizations” or “Regional Benefits Offices.”

• Embrace respite care.

In the last two years that Ms. Hansen, 61 years old, cared for her mother, she sometimes would take her mother to a hospice facility for a week for what is called respite care, which is short-term care designed to give the regular caregiver a break.

Respite programs are available nationwide through social-service agencies, nonprofit groups and long-term-care providers. A good starting place for families is the Eldercare Locator, a federal-government service (go to eldercare.gov or call 800-677-1116).

Some families also could use hospice care, generally meant for patients in the last stages of a serious illness, earlier than they realize, since the goal is to keep the patient comfortable and as pain-free as possible. Medicare provides some coverage for hospice care.

• Know when to consider a permanent facility.

Home care works best “if you need a visiting nurse three or four times a week. But with dementia, it’s round-the-clock care,” says Lee Courtright, a certified financial planner in Stevens Point, Wis. At $17 an hour, the bill can top $140,000 a year. “A nursing home or assisted-living facility can be considerably less expensive,” he says.

Mary Merrell Bailey, an elder-law attorney in Maitland, Fla., arranged round-the-clock home care for her parents, because her father was reluctant to move.

But when she and her mother finally persuaded him, they found that their overall monthly expenses dropped “and their quality of life was far better.” The national median rate for a one-bedroom assisted-living apartment for one person is $3,450 a month, up 4.6% from 2012, according to Genworth.

Still, there are expenses families don’t anticipate that government programs, insurance and institutions don’t cover. Ms. Bailey’s mother, who has diabetes, has drug expenses beyond what Medicare will cover every year, along with prescriptions that aren’t paid for by insurance. Dental work also isn’t covered, the daughter says.

Now, Ms. Bailey urges clients with $200,000 to $1 million in assets—too much wealth to qualify quickly for Medicaid, which pays for long-term care for people with very few assets, but too little to pay for long-term care indefinitely—to consider moving before they have serious health problems to a continuing-care retirement community where they can tap care later.

Thank you for sharing superb informations. Your internet site is very cool. I am impressed by the details that you’ve here. It unveils how perfectly you perceive this specific subject. Bookmarked this site, will come back for additional articles. You, my pal, Good ole’! I found exactly the info My partner and i already searched all over the place and merely couldn’t come across. That of a perfect web-site.