Hedge Fund Alpha is Negative; Down Around 1700 BPs in 11 Years

July 20, 2013 Leave a comment

Hedge Fund Alpha is Negative; Down Around 1700 BPs in 11 Years

July 11, 2013

Adam Parker of Morgan Stanley is out with a new report on the S&P 500. He notes that hedge fund alpha has tanked since early 200s and today is still negative, with a drop of about 1700 basis points. At the same time correlation is up making many hedge funds appear to be nothing more than closet index funds.

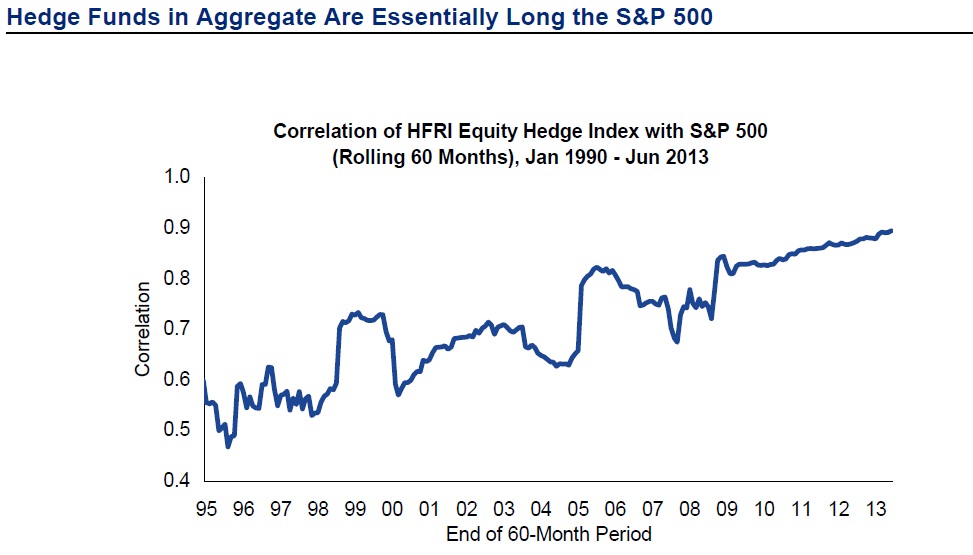

Adam S. Parker, Ph.D., Chief US Equity Strategist, Morgan Stanley, is out with a great new report titled ‘US Equity Strategy’. In the 99 page report Parker has nearly a hundred interesting charts. Morgan Stanley sees the S&P 500 (.INX) in 2014 at 1600 in the base case scenario . However, the most interesting data is on hedge fund alpha and hedge fund correlation with the S&P 500 (.INX). HFRI and S&P 500 Correlation

In terms of correlation, the S&P 500 correlation with the HFRI Equity Hedge Index is moving up. Basically,investors are paying 2/20 to buy a closet index fund. As Parker puts it (in a much more eloquent fashion) ‘Hedge Funds in Aggregate Are Essentially Long the S&P 500′. See the chart below.

Although there is no explanation given, the rise in correlation is likely due to the macro dominated news atmosphere. Many investors have complained that stocks are not moving based on fundamentals, but rather based on what Ben Bernanke said (or didn’t say). With the stock market riding the QE gravy train most stocks are moving in tandem with the S&P 500 and broader market. This makes it an especially tough environment for value investors who have lamented in the past few years that investors have been ignoring fundamentals.

The other piece of data has to do with hedge fund alpha. The chart below speaks for itself and is another sad tale. Hedge fund alpha is now negative, meaning (for the large percentage who find alpha to be a useful metric) that hedge funds are underperforming.

When you put the two facts together you see how truly sad the situation is. Not only are many hedge funds just closet index funds with enormous fees, but investors are paying for both the underperformance (and risk adjusted underperformance).

Hedge Fund Alpha Abysmal

The final nail in the coffin, hedge fund alpha ( see chart at the top). Alpha was very high in the 1990s and up to about 2002 (it appears to have hit about 16 percent). Since then alpha has gone downhill and is now in the negative territory for quite some time (it appears to be negative one currently). While Parker notes that it is difficult for hedge funds to outperform in big up years alpha was high in the late 1990s. Furthermore, even though long biased hedge funds are having a better year than short biased funds, the numbers are still abysmal.

I would guess that alpha has fallen 1. Because there are so many more hedge funds with guys living in their parents basements charging 2/20 who might not be great money managers 2. Increasing correlation due to the large role central banks are playing in today’s market. Whatever the reason, it is hard to argue that investors would have been far better off putting their money in a hedge fund the past few years, as opposed to an S&P 500 index.