Japan Tells Firms: Stop Sitting on Cash; Government Wants Companies to Invest More at Home

July 20, 2013 Leave a comment

July 19, 2013, 6:12 p.m. ET

Japan Tells Firms: Stop Sitting on Cash

Government Wants Companies to Invest More at Home

YOREE KOH, MITSURU OBE and MAYUMI NEGISHI

TOKYO—Okuma Corp., 6103.TO -3.64% a Japanese machine-tool maker, has seen its stock price rise around 30% this year. Its customers have outdated machinery that needs replacing. But, for now, the company isn’t investing. Instead, it is sitting on a pile of cash worth about $280 million—50% higher than its pile a decade ago, equivalent to one-fifth its annual sales, and more than twice the level required for the firm to be deemed loan-worthy by a bank. Why? Senior director Chikashi Horie says the answer is simple. Okuma’s clients “are not investing, not even to raise efficiency, so we are not investing either,” he says.Okuma’s thinking embodies one of the key challenges for Prime Minister Shinzo Abe’s ambitious growth plan: persuading Japan’s famously stingy companies to stop stashing their earnings in the bank, and putting the money to more productive use, helping complete—rather than short-circuit—the virtuous economic cycle.

For so-called Abenomics to create a sustainable recovery, companies need to use the gains they’ve enjoyed from market movements—rising stocks, and a weaker yen that has boosted export profits—to start spending, on capital expenditure or higher worker wages, so the money moves further through the economy.

But battered into parsimony by a two-decade-long slump, Japan’s executives say they aren’t planning to shed their caution after just a few good months.

“Nobody expected the stock market would go up so much, and nobody is sure if this trend will continue,” says Yasuo Takaha, a spokesman for Seven & i Holdings Co.,3382.TO -1.13% operator of 7-Eleven convenience stores—one of 11 Japanese nonfinancial companies holding $10 billion or more in cash and short-term investments.

“Economic recovery is hardly felt by ordinary people or small-business operators,” says Mr. Takaha, explaining why the retailer has no plans to draw down its savings or ease a long-standing policy of keeping new investments within cash flow.

Overall, Japanese companies control ¥225 trillion in cash, or $2.27 trillion, according to the Bank of Japan 8301.TO -0.17% . That’s 26% more than the $1.8 trillion in cash and liquid assets that U.S. nonfinancial firms have stashed away, according to the Federal Reserve, even though the American economy is 2.5 times bigger than Japan’s.

While a flush balance sheet is a sign of financial health, Japan’s economy has long suffered from too much of a good thing. The high corporate savings rate has resulted in part from—and aggravated—a long period of deflation and decline, when executives saw little investment opportunity in a home market of shrinking demand.

Mr. Abe and central bank Gov. Haruhiko Kuroda are trying to create economic conditions that change the so-called deflationary mind-set in the executive suites, either by spurring more domestic demand for Japanese-made products—or by forcing companies to stop parking money in the bank by creating an inflation that would erode the value of those savings.

“Investment is the key to Japan’s recovery,” wrote Martin Schulz, a Fujitsu Research Institute economist, in a presentation this month. He noted that capital investment accounts for about 65% of Japan’s economic growth.

Japan’s capital expenditures fell sharply after the global financial crisis in 2008 and have never fully recovered; they’re still 10% below pre-shock levels. Despite the economic rebound that started late last year, capital spending remains a question mark. The government expects capital outlays to fall 1.5% in the April-June period from the previous quarter, despite a 10.5% jump reported in May over April.

There is some sign of improvement. The mood among businesses improved sharply in the three months to June, according to the Bank of Japan’s latest quarterly corporate survey released July 1. It showed big manufacturers and non-manufacturers revised their combined business-investment plans for the current fiscal year started April to a 5.5% rise from the 2% drop they predicted in the March survey. A rise of that magnitude would be the biggest annual increase since the fiscal year ended March 2007.

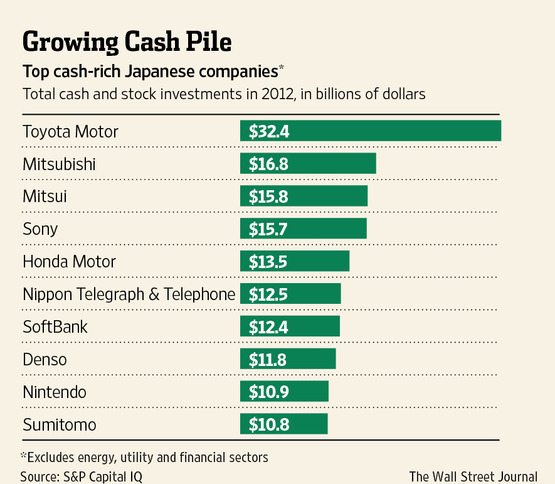

But Japan’s biggest manufacturer, Toyota Motor Corp., 7203.TO -0.15% has no plans to spend more. Peppered by questions from reporters last week about how Abenomics was affecting the auto industry, President Akio Toyoda noted that car sales in Japan have fallen 8% so far this year, after subsidies for eco-friendly models expired. “In that situation, it would be hard to increase spending to ramp up production,” he said.

Long nicknamed “Bank of Toyota,” the world’s No. 1 auto maker epitomizes Japan’s cash-rich challenge. Toyota held the most cash among nonfinancial Japanese firms last year, according to data provider S&P Capital IQ: about ¥3.16 trillion in cash, cash equivalents and short-term marketable securities in the fiscal year that ended March 31.

Toyota agreed to pay an annual dividend of ¥90 per share for the just-ended fiscal year, an 80% increase from a year earlier. But that still left the auto maker’s dividend yield at 1.5%—bringing it to the average level of Japanese companies trading on the Nikkei 225, but well below the 2% average for the U.S.’s S&P 500.

And that amount—about 30% of the auto maker’s net profit, which tripled to ¥962.1 billion in the last fiscal year—is still “just a drop in the bucket” says Christopher Richter, a senior auto analyst at CLSA Asia-Pacific Markets, compared with the massive amount of cash Toyota has in the company vault. It hasn’t repurchased shares for four years.

“We want to use our money in a clever way,” Toyota executive vice president Nobuyori Kodaira, who oversees the company’s accounting, told reporters at a news conference this month. He defined “clever” as, essentially, keeping spending at a minimum, letting the money accumulate while the manufacturer lowers its break-even point by squeezing spending.

He said Toyota is still cautious after a rush to indulge in large-scale investments and rapid expansion before the 2008 global financial crisis boosted fixed costs. That led to the company’s first-ever operating loss, and paused construction of a halfway-completed Mississippi factory, which eventually opened two years later than initially planned.

Toyota’s cautious message is handed down from Mr. Toyoda, who has vowed to adhere to a low-risk strategy to attain sustainable long-term growth. He preaches the need for caution and readiness to cope with future crises as the company comes off several years beset by unforeseen challenges, including an embarrassing product recall and a string of natural disasters.

The painful experience of the financial crisis has left many Japan companies scarred. “The investment cycle used to be every three years in Japan, but after 2008, it has gone all out of sync,” says Okuma’s Mr. Horie. A recent study by the Ministry of Economy, Trade and Industry shows that 60% of equipment at Japanese factories is at least 10 years old. Mr. Horie says most factories have been due some kind of upgrade for at least three years.

Meanwhile, the government is having trouble coaxing companies that are ready to dip into their cash reserves to keep the money in Japan. Instead, companies are continuing their overseas shopping spree to combat a shrinking domestic market.

Seasoning maker Ajinomoto Co. 2802.TO -1.70% said it has about $3 billion earmarked for a possible acquisition, but it is only looking to make acquisitions abroad. “We need to be ready for any opportunity to acquire a company that will help us expand our range of products,” said Masatoshi Ito, president of the maker of monosodium glutamate and aspartame. “That money is for M&A only.”

As SoftBank Corp. 9984.TO -0.31% embarked on its $21.6 billion takeover of U.S. wireless carrier Sprint Nextel Corp., S +0.33% the biggest-ever overseas acquisition by a Japanese company, CEO Masayoshi Son said he plans to slow down capital expenditures on its Japan network, because it is already better than domestic rivals.

Unicharm Corp., 8113.TO +0.53% a Tokyo-based diaper and sanitary napkin maker, has been raising investments the past few years—but only 30% stayed in Japan, with the rest going to emerging markets like China and India.

“The government is now saying it’s the companies’ turn to take action. But it also needs to create an environment where companies feel that it might be interesting or profitable to spend,” Atsushi Saito, chief executive of Japan Exchange Group Inc.,operator of the Tokyo Stock Exchange, said in an interview.

In a March survey conducted by the METI of over 1,000 manufacturers, a little more than half the respondents said they don’t plan to bring production back to Japan.

Finance ministry officials said that Japan hadn’t been attractive for investment because of the strong yen and high electricity prices. But the yen’s recent weakening has officials hopeful that companies may look to invest in Japan and even bring production back home, especially as domestic business conditions improve.

“We believe that, with one more push—such as through tax cuts—we could actually make that happen,” said a METI official.

But Finance Minister Taro Aso also said the government can only do so much. “The government can provide incentives,” said Mr. Aso last month. “But it’s ultimately the company president who makes the final decision.”

Updated July 19, 2013, 8:56 a.m. ET

Japan’s Growth Outlook Remains Tenuous Despite Rebound

Economic growth is expected to fizzle unless Prime Minister Abe uses momentum from an expected win in Sunday’s election to accelerate policy changes.

By PHRED DVORAK and MAYUMI NEGISHI

TOKYO—Japan’s remarkable economic rebound is likely to give Prime Minister Shinzo Abe a landslide victory in Sunday’s elections. But that growth is expected to fizzle within a year or two, unless Mr. Abe uses his momentum from that win to accelerate some wrenching policy changes.

Economists are already projecting a big drop in growth as early as next year, citing everything from Japan’s stubbornly depressed wages and slow business investment to a plunge in the amount of government spending that is expected to flow through the economy.

Japan’s legislative gridlock means “economic recovery isn’t moving quickly, nor are reforms,” said Mr. Abe, in the July 4 stump speech that officially opened his party’s campaign. “Please help us fix that.”

At first glance, Japan’s long-stagnant economy does seem to be steaming ahead. In the seven months since Mr. Abe took power, Japan’s cripplingly strong currency has weakened 21%, its stock market has risen 68%, and housing starts have climbed for nine straight months as of May, as a tidal wave of easy money from the central bank swept into the markets, pushing up asset prices and lifting profits at exporters like Toyota Motor Corp. 7203.TO -0.15%

The boost from the market surge—as well as an increase in government spending—is starting to seep into the economy at large. Japan has jumped from recession to become the fastest-growing economy among major developed nations; a key government survey showed consumer sentiment rising for five months before falling slightly in June; next week, a survey of prices is expected to show an increase for the first time in 14 months.

But economists warn that many of the factors that should underpin a stable economic recovery haven’t budged. Some big, global firms benefiting from Abenomics, as Mr. Abe’s economy-boosting policies are called, have announced increases in investment and bonuses. But most smaller companies—or those strongly dependent on domestic demand—are still hoarding their cash, and see capital spending falling 8% this year. Base wages overall are still dropping, with the latest report showing a 1.3% drop in May. Consumers are also bracing for a hit from an expected rise in the consumption tax to 8% from 5%, in April.

Mr. Abe and his supporters say they can still coax out growth and spending, pointing to a massive slate of proposed measures, from deregulating drug sales to cutting taxes on investment. Other ideas include loosening labor laws and scrapping rules that keep big industry out of agriculture. But none of those measures are in effect yet, and some are hotly resisted by groups ranging from farmers to doctors.

And the outlook for long-term growth in the country is tenuous. The International Monetary Fund, for instance, in its July World Economic Outlook, raised its estimate for Japan’s economic growth in 2013 by 0.4 percentage point to 2%, but lowered its forecast for next year by 0.2 point to 1.2%.

Fast Retailing, 9983.TO -1.63% operator of the Uniqlo clothing chain, said last week that per-person spending in Japan fell in the three months ended May, and the country’s consumers remain wary. “Japanese shoppers are still looking for discounts, and are extremely price savvy,” said Chief Financial Officer Takeshi Okazaki. On the prospects for inflation, a fundamental goal of Abenomics, he said, “We don’t see signs.”

Tokyo-based construction staffing agency Yumeshin Holdings Co.2362.TO -4.40% is one of the big beneficiaries of the Abe government’s largess: ¥5 trillion-plus ($50 billion) in public-works spending this year, and a planned ¥15 trillion over the next three years, on projects to rebuild Japan’s tsunami-ravaged northeast and shore up quake-resistance in roads and public buildings.

Yumeshin director Shigeo Tomomatsu says that since Mr. Abe became prime minister in December, the company has been besieged by requests from general contractors and subcontracting firms looking for people to help oversee construction sites. The number of projects Yumeshin handles is up by as much as 30% from a year ago.

Yumeshin, whose share price has doubled since the start of the calendar year, plans to increase staff by 60% and crank up new hires—tripling its hiring rate to more than 1,200 in the year to September and by a further 16% the following year. “Even then, that is not going to be enough to meet demand,” Mr. Tomomatsu said.

The good times have made Yumeshin one of the rare firms to raise salaries—by 3%—as customers pay increasingly higher premiums for engineers with more experience.

Developer and home builder Daiwa House Industry Co. 1925.TO -0.89% is toeing a more cautious line.

The Osaka-based company saw construction orders climb 20% year-over-year in the three months through June, largely spurred by would-be home buyers rushing to buy now, ahead of an expected rise in interest and tax rates, as the government’s inflation-inducing policies take hold. The surge in investment raises hope that Japan’s 23-year land-price slump may finally be ending, and Daiwa House is in a fever to buy more property now, before prices rise. Earlier this month, the company announced plans to raise as much as ¥138 billion in new shares to help fund its purchases.

Yet Daiwa House has also been holding back, in case the Abenomics boom—like others in the past two decades—is followed by a bust that pummels demand. “Investors asked us why we didn’t raise more money, given our strong finances, but we don’t want to jeopardize our AA-credit rating,” said Chief Financial Officer Tetsuji Ogawa. “Should Abenomics wear off and the numbers fall next fiscal year, we will be able to ride it out by simply selling off some property.”

In central Tokyo, broker Nomura Holdings Inc. 8604.TO -1.21% has been celebrating the markets renaissance. The broker’s profit in the quarter ended March—the last for which results are available—was its best in seven years. “Whether it be stocks or foreign exchange, the market is starting to think that there could be a huge shift in the trend,” says senior managing director Satoshi Arai. “Our sense is that if you compare last November [before Mr. Abe came to power] with April or May, investors’ mind-sets have completely changed.”

But stock rallies have dissolved quickly in Japan in the past, and the country’s benchmark index is still nearly two-thirds below its 1989 peak. The country’s wary mom-and-pop investors tend to run when the market moves against them. Many have been seeing holdings recover value in recent months, but they are worried about other things like income or retirement savings, so they aren’t increasing the amount they are spending, says Keiko Yatsui, an independent consultant in Tokyo, who specializes in poring over household-savings plans, looking for ways to save money.

Ms. Yatsui’s clients tend to be members of Japan’s middle class, who haven’t seen many tangible benefits from Abenomics yet. Although she has seen an increase in the number of clients asking whether they should start investing now, Ms. Yatsui says she tells them that scrimping will often get better returns than putting money in stocks. You can get the equivalent of a 1% return on ¥1 million—with a lot less risk—merely by cutting household spending around ¥833 a month, she points out.”I don’t think investment is a must. Holding down expenses is better,” she says. “Actually, the stock-price movements under Abenomics have been rough—it’s hard to go into the market.”The government is rolling out one solution for wooing more ordinary people into stocks, in a foreshadowing of the type of measures that Mr. Abe could take to encourage long-term growth and investment. From next year, retail customers will be able to invest up to ¥1 million a year in a special tax-free account, for at least five years. The government hopes to collect some ¥25 trillion in such accounts by 2020.

Financial institutions are busy holding seminars and signing up customers.

Nomura alone has conducted around 500 classes since the beginning of May and is planning 120 more; it is offering ¥2,000 to people who open an account with them before September.

On a recent afternoon, in a suburb east of Tokyo, about 35 people—mostly retirees—gathered to hear Nomura’s spiel, scribbling notes and asking questions.

Retiree Shoichi Saesu, 78, said he is thinking of moving some money into a tax-free account. Mr. Saesu already has a portfolio of 2,000 stocks, and he has made ¥1.8 million on his shareholdings since the start of the year—much of which is going into medical care for his ailing wife. He has been a relatively savvy investor, cashing in before Japan’s asset bubble collapsed in the early 1990s, but losing some money after the fall of a big Internet company in the late 2000s. “The bubble taught me to cash in when you can,” he said.

Mr. Saesu said he would ideally like to put much more of his assets in stocks, but won’t do that until Japan’s economy and markets stabilize.

As for Abenomics, “I support the Communist Party,” he said, reeling off a list of gripes—from increasing nursing costs to stagnant salaries—that he said Mr. Abe’s ruling Liberal Democratic Party wasn’t addressing. “There are too many uncertainties in the Japanese economy right now.”

July 19, 2013, 10:36 p.m. ET

Next Economic Step for Japan’s Abe Could Be Toughest

Prime Minister Faces Challenges Enacting Third Plank of Abenomics—Structural Reform

MITSURU OBE

TOKYO—As the campaign for Sunday’s upper house election enters its final stretch, calls from politicians for painful structural reforms have largely been drowned out by promises of tax breaks, casting doubt over how far Japanese Prime Minister Shinzo Abe will go with his economic overhauls.

While Mr. Abe’s policies of short-term spending and aggressive monetary easing have helped lift stock prices, weaken the yen and spark growth, it is the third plank of his economic strategy—structural reform—that is seen as the key to securing an expansion of the economy over the longer term.

An expected victory for Mr. Abe’s Liberal Democratic Party in the election should strengthen his hand to act, but the lingering question on the minds of some economists and government officials is whether he will seize the opportunity to implement truly drastic reform steps.

“With no other national elections slated in the next three years, the time has come to carry out reforms. It’s now or never,” a senior Finance Ministry official said.

Koya Miyamae, an economist with SMBC Nikko Securities, is among those who see Mr. Abe capitalizing on an election victory. He believes Mr. Abe will start talking about the “bitter pills” the nation needs to swallow, such as fiscal reform and tax increases, once the election is behind him.

Among issues the administration is under pressure to address are agricultural and labor reforms. Faced with growing overseas competition and foreign political pressure, Japan’s inaction on these two issues has been the subject of intense scrutiny.

“If Japan’s labor market was allowed to become more flexible, then more bright and experienced workers at big corporations would be made available to small and startup firms, promoting the growth of new industries and create more new jobs,” said Yasuyuki Nambu, president of job placement firm Pasona Inc., expressing hope that Mr. Abe’s structural reforms will go beyond what was announced in June.

But given the high risk associated with taking such steps, some observers say Mr. Abe will stick with easier options.

“Structural reforms are often put on the back burner to tax breaks or monetary easing because their benefits are much less obvious,” said Yoshihito Kaneda, president of Tokyo-based technology company Fact-Real Inc. Mr. Kaneda, a startup mentor who helps college students and young graduates start their own firms, is among those who have been sounded out by the government for ideas on reform.

Mr. Kaneda notes that for all Mr. Abe’s talk of structural reform, no visible progress has been made since these strategies were unveiled nearly two months ago.

He gives the example of the personal guarantees required by banks for about 80% of loans to small businesses in Japan. To promote risk-taking by budding entrepreneurs, the premier has talked about phasing out such requirements, but nothing has happened yet, Mr. Kaneda said.

What’s more, Mr. Abe looks set to restrict this relaxation to startups, excluding the many small business owners already struggling with debts they have personally guaranteed, according to Osamu Nakajima, a local government official in charge of business assistance in Tokyo’s Itabashi ward. Such guarantees prevent entrepreneurs from winding down failing businesses and starting over.

Mr. Abe wants to raise Japan’s growth rate to 2% a year in real terms for the next 10 years, up from 0.8% in the past 20 years, by implementing his growth strategies, which include spurring entrepreneurship, innovation, and investments in new business fields.

In order to do this the government will have to take significant steps to reconfigure Japan’s rigid industrial structure, which helped drive the nation’s postwar growth but has become outdated as the manufacturing sector shifts to other parts of Asia.

Japan’s highly restrictive dismissal rules, for example, have led to firms limiting their hiring of permanent, full-time workers in favor of part-timers. Last week, the government announced that the number of non-regular workers topped 20 million for the first time ever, accounting for a record 38.2% of the total workforce.

Still, labor unions are determined to block any attempt by the government to allow “labor market flexibility,” which Mr. Abe says is necessary to grow new industries and wind down inefficient ones. “It’ll be very difficult to strip away the job security” that has already been awarded to regular workers, said Kyoji Fukao, an economics professor at Hitotsubashi University and an adviser to Mr. Abe’s LDP.

“Reforming dismissal rules will take a couple of years of intense discussions,” added Kotaro Tsuru, professor of Keio University and head of the government’s labor reform panel. Mr. Tsuru said the government will focus on legislating and promoting a new category of workers with limited employment protection, which he hopes would reduce the number of part-timers and increase jobs for women returning to the labor market after giving birth.

Agricultural reform is another difficult challenge. Mr. Abe vows to raise the competitiveness of Japanese farmers by tackling their main problem—small scale—through the consolidation of fragmented farmland. Mr. Abe envisions local governments as helping consolidate small pieces of land into large lots and renting them to businesses and large-scale farmers.

But such a move “directly infringes on the interests of small farmers,” a senior government official said. Small farmers—a key support base of Mr. Abe’s LDP—are holding on to their land in the hope that it could be used to make money in the future. Japan’s lax zoning regulations and low property taxes on unused farm land have encouraged such behavior. “There’s no sign yet Mr. Abe will tackle these issues,” the official said.

Some officials hope that the stalemate could be broken by the U.S.-led Trans-Pacific Partnership, which would be Japan’s first, genuine free trade pact covering all areas including agriculture. “The TPP could be the catalyst for agricultural reform,” a senior official involved in the talks said.

July 19, 2013 4:02 pm

This time there is a case to buy Japan

By John Authers

Corporate reporting season will be test of profitability

This is Japan’s moment of truth. Sunday’s election, whether premier Shinzo Abegains a two-thirds majority in the upper house or, as appears more likely, he has to settle for a strong position just short of that, should give the country three election-free years. That will be one of the longest periods of political calm since the war. Meanwhile, the “third arrow” of so-called Abenomics is about to fire. Is there still value in Japan’s stock market?

An initial reaction is to scream “no”. First, there is the “Charlie Brown and the football” syndrome. Investors have had a tempting Japanese value proposition put in front of them many times since 1990. It is always pulled away leaving them on their back.

Second, there is the “tide is high” issue. Japanese stocks have rallied 42 per cent this year, in yen terms. Even in dollars, which make it look more similar to the US, Japan has beaten the rest of the world by some 18 per cent since Mr Abe’s arrival, according to FTSE indices. Jumping in when the tide has already surged in to this extent is seldom wise.

Yet there is a case to buy Japan. But it rests less on politics, and more on the corporate reporting season which is about to start, and it may rely less on Mr Abe and more on the earthquake and tsunami of early 2011. That human tragedy forced companies to restructure, slowly and unwillingly. We should now begin to see whether this can transform Japan’s profitability.

As the chart shows, Japan’s earnings have followed a fitful and erratic path over the past 20 years, particularly compared to the US. That is partly because the Japanese do not play the game of “shareholder value”, or attempt to maximise value for shareholders. But it also has to do with endemic over-capacity, while the sharp dip in recent years was driven by the disaster of the tsunami.

Jesper Koll, head of equity research for JPMorgan in Tokyo and a cheerful bull, points out that five years ago there were 11 major department store chains in Japan. Now there are four. This took out a layer of selling and administrative expenses, leaving them far more leveraged to a rise in sales.

By Mr Koll’s arithmetic, a 1 per cent increase in sales would once have driven a 10 per cent rise in profits; it would now push a 30 per cent profit rise.

Banks also benefit from gearing; they can still get away with zero interest on deposits, but the interest they can charge is growing nicely in response to rising loan demand – perhaps helped by post-tsunami reconstruction efforts.

Further, the yen has devalued in response to the first arrows of Abenomics, which involve aggressively lenient monetary policy. That boosts the profits of exporters, and should provide a catalyst.

Overall, the Topix trades at a multiple of 13.7 times 2015 consensus forecast earnings. If Mr Koll – or other Japan bulls with similar hopes – is right, then profits could be 30 per cent higher, which would still only be about 15 per cent above their high for the past 10 years. On this basis, the market is on a multiple of 10.4 times 2015 profits – and there is room for a drastic rise in prices.

While these trends pre-date Abenomics, its third arrow, if fired effectively, could accelerate this process. The next wave of changes, the hardest politically, involve structural reforms – a euphemism for measures that will hurt many, such as labour reform.

If the third arrow lands on target, then corporation tax will be slashed, from 40 per cent to somewhere closer to international norms, of maybe 20 or 25 per cent. That will directly boost companies’ bottom lines. Moves to make it easier to fire workers would also boost profits, as well as continue the process of reducing Japan’s excess capacity.

Cutting capacity would be good for stocks, and also fulfil Mr Abe’s aim of reviving inflation by restoring companies’ pricing power. What is good for companies and investors would not be so great for consumers.

There are still, however, plenty of risks, with the most significant lying across the China Sea. China accounts for more than 20 per cent of Japan’s exports, and more than the US. A slowdown at the worse end of current forecasts would be terrible news. A Chinese hard landing could also start a “risk-off” wave in markets, which would push up the yen, damaging exporters.

At home, the risk is that next year’s scheduled rise in sales tax from 5 per cent to 8 per cent is already accelerating the business cycle. Rising consumption could go back into reverse once the new tax rate comes into effect. Tetsufumi Yamakawa, Barclays’ head of research in Japan, suggests this could mean a fiscal contraction of as much as 1.5 per cent of gross domestic product – almost a Japanese “fiscal cliff”.

But the critical question is how much the cuts in capacity that have taken place so far have improved Japan’s endemic problem of poor profitability. Markets are betting that the consensus forecasts are pessimistic. Will Japan’s next earnings season prove them right?