Working late at the office, milking it too; White-collar criminals are often dedicated employees with a problem they can’t share, but are they getting off lightly?

July 20, 2013 Leave a comment

Working late at the office, milking it too

July 20, 2013

White-collar criminals are often dedicated employees with a problem they can’t share, but are they getting off lightly? Ben Butler reports.

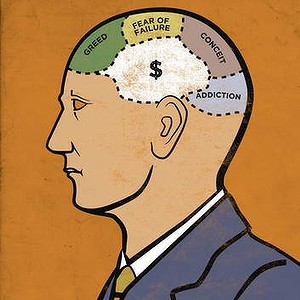

They are quietly beavering away at the accounts, stalwart senior managers willing to shoulder more than their share of the management load, trusted members of the team who have put in plenty of years and are perhaps a little overdue for a pay rise, but don’t complain. And they’re stealing from the company. Forget the portrait of embezzlers as snakes in suits, sharp operators and office psychopaths who talk fast and bully others to get their way. New research based on interviews with convicted white-collar criminals shows the average person who decides to steal a substantial amount of money from work is a self-sacrificing hard worker with a problem he or she can’t share. Usually it’s gambling, but the pressure to maintain appearances can also drive managers and company owners – especially men – to dip their fingers in the till.The surprising findings of the study, conducted by Monash University forensic psychologist researchers David Curnow and James Ogloff, have big implications for the way companies try to deal with fraud.

And there are also implications for the justice system, which has been grappling with the issue in recent years after criticism that judges have been far softer on white-collar offenders than they are on blue-collar crooks.

Megha Mizerni, a facilities manager at the Reserve Bank, pleaded guilty this week to swindling about $600,000 from his employer by falsifying invoices for about 18 months. He is yet to be sentenced.

To find out what makes white-collar criminals tick, Curnow interviewed 30 prison inmates, 18 men and 12 women, who were serving time for taking between $100,000 and $22 million from their employers.

”We didn’t want people who’d been stealing the office paper clips or the milk money,” Curnow says.

They were typically senior management in their 40s who had been working for their organisations for at least five years.

”There were some interesting facets, especially in smaller organisations, where they were the book-keeper, the secretary – they had lots of different roles and that was half the problem,” Curnow says.

”They were quite underpaid in many ways, those people.

”But at the same time, we had senior accountants, in a couple of cases CEOs, so a pretty wide variety.”

These were not scammers like Graeme Hoy and Ian Rau, who ran a Ponzi scheme that took more than $82 million from the people of industrial Geelong.

Nor were they the former high-flyers who pushed their way to the top of the business world only to see it all come unstuck when the global financial crisis hit in 2008.

The inmates were subjected to a barrage of psychological tests that confirmed they were not workplace psychopaths – people who deliberately inflict harm on their colleagues for their own advantage.

”They [psychopaths] may well bully people, they may well be fairly ruthless with other staff – they don’t tend to steal the money, that’s something that this group does,” Curnow says.

The study group scored so high on a test of personal morality that ”it was basically a useless score”.

”They perceived themselves to be very, very moral people.”

They owned their own homes, raised families and contributed to the community through church groups or Rotary International – from the outside, the offenders Curnow studied looked utterly respectable.

”When you’re working with offenders, you spend a lot of time wondering how someone could do what they’ve done, like an armed robbery or murdering somebody, whereas with white-collar crime what really stuck out to you was how similar they were and in some cases much more successful than you were – and yet still decided to offend,” Curnow says.

”It’s an odd behaviour from someone apparently so successful.”

At the root of this odd behaviour, the researchers found what they called a ”non-shareable financial problem”.

Typically, that was gambling, but some men in the study were also motivated by a need to keep up appearances.

In those cases, money pilfered from work was spent on things such as maintaining the expensive lifestyle appropriate to a successful businessman, or papering over financial holes caused by bad investment decisions.

But while status was important to some, ”over half the people involved had significant problems with gambling”, Curnow says.

”Horseracing came up a couple of times but without a doubt pokies was the No.1 issue.”

He said high-roller rooms, such as the one maintained by James Packer’s Crown casino in Melbourne, were mentioned by some participants in the research.

”The respondents said that organisations like casinos never ask how you got the money, and so people start to perceive themselves to be successful gamblers – ‘I’m really quite good at this’ – and start to spend larger and larger amounts of money there.

”That becomes part of their status as well, to maintain preferential treatment at places like casinos.

”Sometimes work and the gambling seemed to inter-relate. So they were really angry at something that was going on at work and the way to deal with it was going to pokie locations and zoning out, with all the things that such places do, like not having clocks in there, quite deliberately making you feel a bit special, through free drinks, etc.”

Curnow’s interest in white-collar offenders was sparked 14 years ago, when he noticed they were receiving shorter sentences than their blue-collar counterparts, despite ”stealing a great deal more than armed robbers would get”.

One of the reasons often given for the disparity is that while the victims of a robbery are living, breathing people whose lives have been bent out of shape by an encounter with crime, corporations are bloodless abstractions – difficult victims when a judge comes to assess the damage done.

And yet the damage is real.

Famous for the ”e-e-easy” catchphrase it used in its TV advertising, Clive Peeters was once a 50-strong chain of electrical goods stores, employing more than 1000 people.

But from 2007, it suffered a bewildering decline in cash flow, even apparently missing out on the millions pumped into retail when the federal government handed out cash to people following the global financial crisis.

The company blamed everything from cool weather to rising petrol costs and a flat housing market for the problem, but the real cause emerged in 2009: senior accountant Sonya Causer has been defrauding the company for years, fiddling with the books to hide her crime.

While some of the $20 million Causer took went on cars and Beanie Babies – collectible stuffed toys that can fetch thousands of dollars on eBay – most went on a property binge in which she snapped up more than 50 houses and units across Melbourne and even Queensland.

Causer went to jail and Clive Peeters was able to recover much of the money by selling the properties. But, buffeted by the increasingly harsh retail environment, it was unable to recover and fell into insolvency in 2011.

One voice criticising the lenient sentencing of white-collar criminals has come from within the judiciary itself, in the shape of Federal Court judge Ray Finkelstein.

Now retired from the bench, Finkelstein made his views on white-collar crime clear when he handed down a ruling against former Telstra director Steve Vizard in a 2005 civil penalty case over insider trading.

”Those convicted of such offences rarely have a criminal record,” he said. ”It is their good character that has enabled them to occupy the position of trust which they have ultimately breached. Indeed, it is their good character that is often used to facilitate the offence.

”So while good character cannot be ignored, it should only play a minor role in sentencing for most white-collar corporate crime.”

While Finkelstein admitted that the public shaming of a well-known figure such as Vizard was a form of punishment, he said it was not enough.

”Formal retribution is a necessary element in imposing a proper punishment because it ensures that punishment is just and appropriate to the circumstances.”

He went on to disqualify Vizard from being a company director for 10 years – double the penalty agreed on by Vizard and the Australian Securities and Investments Commission.

Finkelstein was travelling this week and unable to comment. However, he provided Weekend Business with the text of a speech he gave at a conference at the University of South Australia in 2010, in which he said ”the past leniency of courts is slowly being addressed by the courts themselves and, with the aid of parliamentary intervention, through increased penalties”.

Data from the Victorian Sentencing Advisory Council lends weight to Finkelstein’s argument, showing that over the past decade there has been a gradual increase in the proportion of fraudsters sent to jail.

In 2003-04, the proportion of people guilty of the classic fraud offence – obtaining a financial advantage by deception – who were immediately sent to jail dipped to as low as 26 per cent.

But by 2010-11, the imprisonment rate had clawed back up to 48 per cent, a return to its 2002-03 level. In 2011-12, an even half of people sentenced for the offence were sent straight to jail.

The average jail term imposed has made a more dramatic increase, climbing from one year and six months in 2001-02 to two years and three months in 2011-12.

In NSW, more than 60 per cent of offenders convicted of obtaining a benefit by deception have been sent to jail since 2008. The rate hit as much as 74 per cent in 2011 before falling back to 63 per cent last year.

But before offenders can be brought to trial, they have to be charged – and, according to Dean Newlan, a partner at specialist advisory and insolvency firm McGrathNicol, companies are often reluctant to take legal action ”because of the embarrassment internally within the organisation, but also externally in terms of embarrassment to the organisation”.

”It’s not good policy because one thing that often happens is that if you try to keep the lid on something, the public find out about it by some other means, and then you’ve compounded the problem by concealing it,” he says.

The lack of reporting means nobody really knows how much employee fraud costs Australian business.

While there are estimates that it costs the community billions of dollars a year, these figures include everything from credit card rip-offs to welfare cheats.

When police do become involved, it can take years for cases to wend their way through the court system.

Owain Stone, who heads the forensic department of McGrathNicol’s competitor, KordaMentha, says he gave evidence in a fraud trial that related to events that occurred five years earlier.

Companies would ”rather just forget about it”, he says.

The delay also weighs heavily on those accused of white-collar crime.

”For the last three years I’ve effectively been in home detention,” says a former executive who is facing multiple charges. ”It’s a big game for the lawyers who want to suck money out of this process.”

While the events over which the executive was charged happened more than three years ago, he is yet to come to trial.

He says prosecution lawyers, used to dealing with crimes such as murder, struggle to comprehend white-collar offences.

Meanwhile, life has been ”horrendous”. He has been unable to work because potential employers find out about his past through a Google search of his name, which has been splashed across the media.

”I get that people are angry,” he says. ”I’m not asking for pity, that people should feel sorry for me – but if you look at the process of how things are done, it’s not right.”

Back at the cubicle farm, it seems that today’s leaner, meaner organisations are leaving themselves open to fraud.

Newlan says companies are often not prepared to spend the money needed to reduce the risk of fraud.

”They take it seriously but they don’t think it will happen to them.

”Often the time we get involved in prevention is just after the horse has bolted – they’ve just had a major incident and they get us in so that it won’t happen again.

”They think the worst that can happen to them is a $500,000 loss, and they have a $15 million fraud and that comes as a complete surprise to them.”

Stone says many cases of fraud are discovered ”by accident” – for example, when the perpetrator goes on holiday. Both he and Newlan recommend that organisations end the taboo around recognising workplace fraud and encourage employees to report suspicious behaviour by colleagues.

But for Curnow, it could be as simple as getting managers to ask their workers simple questions: ”How are you working with people, how do you think the organisation is going?

”Organisations need to ensure they complete criminal records checks, especially for high-trust positions and not do things like let people never take holidays or work to 8 o’clock at night.

”Tell people to go home.”