Beijing Lending Shift May Force Banks to Raise Capital; China’s banks will need up to $100 billion in new funding over the next two years following Beijing’s move to shake up lending

July 22, 2013 Leave a comment

July 21, 2013, 12:06 p.m. ET

Beijing Lending Shift May Force Banks to Raise Capital

Removal of Floor on Loan Rates Is Seen Hitting Smaller Lenders Hardest

BEIJING—China’s banks will need up to $100 billion in new funding over the next two years following Beijing’s move to shake up lending, according to an analysis by a research firm, and that could spur banks to tap investors for capital even amid growing worries over the strength of their balance sheets. China’s central bank on Saturday removed a government floor on the interest rates banks can charge their clients for credit, allowing financial institutions to price loans at whatever level they want. Authorities hope the action will foster competition among banks and result in easier access to loans for businesses and individual borrowers, especially small and private manufacturers long shunned by big state-owned lenders. On Saturday, the People’s Bank of China 601988.SH -0.38% followed its policy announcement with instructions to the banks to take active advantage of their new freedom.

Bankers and analysts say the step is unlikely to immediately result in cheaper loans for China’s borrowers, because few banks were lending at interest rates close to the floor. But in the long run, many inside and outside the banking industry say, increased competition will hurt lending profitability, increase banks’ need for capital and prod them to develop businesses that are less susceptible to swings in interest rates.

The move is part of a broader effort by China to overhaul its financial system, which many economists say must change to sustain economic growth.

Lending accounts for the vast majority of Chinese banks’ profits. Assuming a 10% decline in net interest income—or the difference between what banks charge on loans and pay on deposits—and a 15% increase in assets, Chinese banks would have to raise between $50 billion and $100 billion in the next two years to maintain their current capital-adequacy levels, according to an analysis by ChinaScope Financial, a Shanghai-based research and data firm partly owned by Moody’s Corp. MCO +0.02%Chinese banks have raised about $50 billion in capital through equity sales in the last three years.

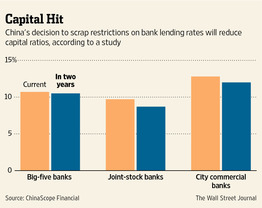

The study, to be released Monday, is based on an examination of some 140 Chinese banks. It found that city-level commercial banks would have the biggest need for capital, while the country’s big banks would have relatively small needs.

So far, Chinese banks have largely maintained enough capital to absorb losses from bad loans. According to the ChinaScope study, their Tier 1 capital ratio, or the amount of common stock and retained earnings as a percentage of total assets, currently stands at an average of 12.8% for the country’s city commercial banks, 9.7% for joint-stock banks, and 10.7% for the country’s five largest banks by assets, which areIndustrial & Commercial Bank of China Ltd., 601398.SH -0.76% China Construction Bank Corp., 601939.SH -1.38% Agricultural Bank of China Ltd., 601288.SH -0.79%Bank of China Ltd. and Bank of Communications Co. 601328.SH -1.30% Those figures are all above the minimum capital ratios required by Chinese regulators, which are 7.5% for big banks and 8.5% for small ones.

But because Chinese banks are expected in the ChinaScope study and by others to see their lending income drop over time due to Saturday’s move, they would have lower earnings to sustain their capital base. That, combined with the potential for more soured loans as China’s economy slows, “could cause a severe capital shortfall for the banks in the longer term,” said Tom Liu, chief executive of ChinaScope. “Chinese banks would have greater needs for capital as banks will have less interest income to cover the losses from increasing nonperforming loans.”

The need for capital could lead Chinese banks to step up their efforts to raise funds by selling securities, even as investors have grown increasingly wary of Chinese banks. While nonperforming loans remain low, concerns over asset quality are mounting amid the country’s weakening economic growth and banks’ exposure to riskier borrowers such as property developers, local governments and manufacturers that are suffering from overcapacity.

In a sign of investors’ belief that more stress is ahead for Chinese banks, many hedge funds and other alternative funds are sticking to heavy bets against Chinese banks listed in Hong Kong, even as a cash crunch that gripped China’s financial system has eased significantly. Just three of China’s nine largest banks by assets are trading above book value, or what the assets on their balance sheet are worth, according to FactSet Research.

“It’s very difficult to raise money now,” said a Beijing-based senior executive at one of China’s top four banks. The executive said the bank currently doesn’t have any plan to raise funds through equity sales, but is looking at potentially tapping bond markets to strengthen its capital base.

China’s government has long maintained strict controls on bank lending and deposit rates, imposing a ceiling on what banks can pay on deposits and a floor on what they can charge on loans. That system helped supercharge China’s growth by channeling loans to state-owned enterprises and other big businesses while maintaining wide profit margins for banks. The central bank cautioned that Chinese banks will need more time to gear up for other steps, such as the removal of controls on bank deposit rates.

Prior to the latest move, Chinese banks could already lend at 30% below the benchmark rate, which stands at 6% for one-year loans, but few took advantage of that freedom. A banker at ICBC’s branch in the southern Chinese city of Guangzhou said the bank is unlikely to offer “a bigger discount” to its borrowers in the short term. “But some small lenders may grab this opportunity to vie with big state banks for good clients such as state-owned enterprises,” the banker said.

Because big state-owned companies are likely to maintain their bargaining power, some banks, including Bank of China, indicated that they will shift more of their lending to small and medium-size businesses. “If you only lend to big companies, your interest income is bound to decline,” Li Lihui, Bank of China’s president, told state broadcaster China Central Television on Saturday.