The Great Deceleration: The most dramatic, and disruptive, period of emerging-market growth the world has ever seen is coming to its close

July 26, 2013 Leave a comment

The Great Deceleration

The emerging-market slowdown is not the beginning of a bust. But it is a turning-point for the world economy

Jul 27th 2013 |From the print edition

WHEN a champion sprinter falls short of his best speeds, it takes a while to determine whether he is temporarily on poor form or has permanently lost his edge. The same is true with emerging markets, the world economy’s 21st-century sprinters. After a decade of surging growth, in which they led a global boom and then helped pull the world economy forwards in the face of the financial crisis, the emerging giants have slowed sharply.China will be lucky if it manages to hit its official target of 7.5% growth in 2013, a far cry from the double-digit rates that the country had come to expect in the 2000s. Growth in India (around 5%), Brazil and Russia (around 2.5%) is barely half what it was at the height of the boom. Collectively, emerging markets may (just) match last year’s pace of 5%. That sounds fast compared with the sluggish rich world, but it is the slowest emerging-economy expansion in a decade, barring 2009 when the rich world slumped.

This marks the end of the dramatic first phase of the emerging-market era, which saw such economies jump from 38% of world output to 50% (measured at purchasing-power parity, or PPP) over the past decade. Over the next ten years emerging economies will still rise, but more gradually. The immediate effect of this deceleration should be manageable. But the longer-term impact on the world economy will be profound.

Running out of puff

In the past, periods of emerging-market boom have tended to be followed by busts (which helps explain why so few poor countries have become rich ones). A determined pessimist can find reasons to fret today, pointing in particular to the risks of an even more drastic deceleration in China or of a sudden global monetary tightening. But this time a broad emerging-market bust looks unlikely.

China is in the midst of a precarious shift from investment-led growth to a more balanced, consumption-based model. Its investment surge has prompted plenty of bad debt. But the central government has the fiscal strength both to absorb losses and to stimulate the economy if necessary. That is a luxury few emerging economies have ever had. It makes disaster much less likely. And with rich-world economies still feeble, there is little chance that monetary conditions will suddenly tighten. Even if they did, most emerging economies have better defences than ever before, with flexible exchange rates, large stashes of foreign-exchange reserves and relatively less debt (much of it in domestic currency).

That’s the good news. The bad news is that the days of record-breaking speed are over. China’s turbocharged investment and export model has run out of puff. Because its population is ageing fast, the country will have fewer workers, and because it is more prosperous, it has less room for catch-up growth. Ten years ago China’s per person GDP measured at PPP was 8% of America’s; now it is 18%. China will keep on catching up, but at a slower clip.

That will hold back other emerging giants. Russia’s burst of speed was propelled by a surge in energy prices driven by Chinese growth. Brazil sprinted ahead with the help of a boom in commodities and domestic credit; its current combination of stubborn inflation and slow growth shows that its underlying economic speed limit is a lot lower than most people thought. The same is true of India, where near-double-digit annual rises in GDP led politicians, and many investors, to confuse the potential for rapid catch-up (a young, poor population) with its inevitability. India’s growth rate could be pushed up again, but not without radical reforms—and almost certainly not to the peak pace of the 2000s.

Many laps ahead

The Great Deceleration means that booming emerging economies will no longer make up for weakness in rich countries. Without a stronger recovery in America or Japan, or a revival in the euro area, the world economy is unlikely to grow much faster than today’s lacklustre pace of 3%. Things will feel rather sluggish.

It will also become increasingly clear how unusual the past decade was (see article). It was dominated by the scale of China’s boom, which was peculiarly disruptive not just as a result of the country’s immense size, but also because of its surge in exports, thirst for commodities and build-up of foreign-exchange reserves. In future, more balanced growth from a broader array of countries will cause smaller ripples around the world. After China and India, the ten next-biggest emerging economies, from Indonesia to Thailand, have a smaller combined population than China alone. Growth will be broader and less reliant on the BRICs (as Goldman Sachs dubbed Brazil, Russia, India and China).

Corporate strategists who assumed that emerging economies were on a straight line of ultra-quick growth will need to revisit their spreadsheets; in some years a rejuvenated, shale-gas-fired America may be a sprightlier bet than some of the BRICs. But the biggest challenge will be for politicians in the emerging world, whose performance will propel—or retard—growth. So far China’s seem the most alert and committed to reform. Vladimir Putin’s Russia, by contrast, is a dozy resource-based kleptocracy whose customers are shifting to shale gas. India has demography on its side, but both it and Brazil need to recover their reformist zeal—or disappoint the rising middle classes who recently took to the streets in Delhi and São Paulo.

There may also be a change in the economic mood music. In the 1990s “the Washington consensus” preached (sometimes arrogantly) economic liberalisation and democracy to the emerging world. For the past few years, with China surging, Wall Street crunched, Washington in gridlock and the euro zone committing suicide, the old liberal verities have been questioned: state capitalism and authoritarian modernisation have been in vogue. “The Beijing consensus” provided an excuse for both autocrats and democrats to abandon liberal reforms. The need for growth may revive interest in them, and the West may even recover a little of its self-confidence

When giants slow down

The most dramatic, and disruptive, period of emerging-market growth the world has ever seen is coming to its close

Jul 27th 2013 |From the print edition

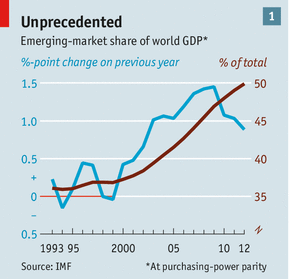

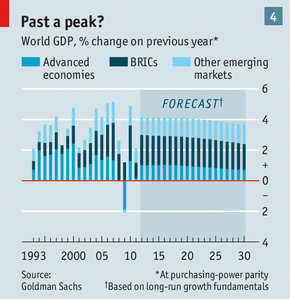

THIS year will be the first in which emerging markets account for more than half of world GDP on the basis of purchasing power, according to the International Monetary Fund (IMF). In 1990 they accounted for less than a third of a much smaller total. From 2003 to 2011 the share of world output provided by the emerging economies grew at more than a percentage point a year (see chart 1). The remarkably rapid growth the world has seen in these two decades marks the biggest economic transformation in modern history. Its like will probably never be seen again.

According to a recent study by Arvind Subramanian and Martin Kessler, of the Peterson Institute, a think-tank, from 1960 to the late 1990s just 30% of countries in the developing world for which figures are available managed to increase their output per person faster than America did, thus achieving what is called “catch-up growth”. That catching up was somewhat lackadaisical: the gap closed at just 1.5% a year. From the late 1990s, however, the tables were turned. The researchers found 73% of developing countries managing to outpace America, and doing so on average by 3.3% a year. Some of this was due to slower growth in America; most was not.

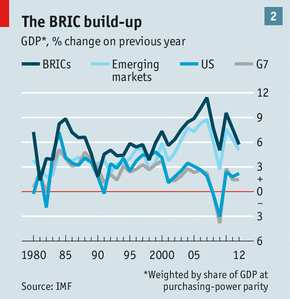

The most impressive growth was in four of the biggest emerging economies: Brazil, Russia, India and China, which Jim O’Neill of Goldman Sachs, an investment bank, acronymed into the BRICs in 2001. These economies have grown in different ways and for different reasons. But their size marked them out as special—on purchasing-power terms they were the only $1 trillion economies outside the OECD, a rich world club—and so did their growth rates (see chart 2). Mr O’Neill reckoned they would, over a decade, become front-rank economies even when measured at market exchange rates, and he was right. Today they are four of the largest ten national economies in the world.

The remarkable growth of emerging markets in general and the BRICs in particular transformed the global economy in many ways, some wrenching. Commodity prices soared and the cost of manufactures and labour sank. Global poverty rates tumbled. Gaping economic imbalances fuelled an era of financial vulnerability and laid the groundwork for global crisis. A growing and vastly more accessible pool of labour in emerging economies played a part in both wage stagnation and rising income inequality in rich ones.

The shift towards the emerging economies will continue. But its most tumultuous phase seems to have more or less reached its end. Growth rates in all the BRICs have dropped. The nature of their growth is in the process of changing, too, and its new mode will have fewer direct effects on the rest of the world. The likelihood of growth in other emerging economies having an effect in the near future comparable to that of the BRICs in the recent past is low; they do not have the potential for catch-up the BRICs had in the 1990s and 2000s. And the BRICs’ growth has changed the rest of the world economy in ways that will dampen the disruptive effects of any similar surge in the future. The emerging giants will grow larger, and their ranks will swell; but their tread will no longer shake the Earth as once it did.

The great return

The BRIC era arrived at the end of a century in which global living standards had diverged remarkably. Towards the end of the 19th century America’s economy overtook China’s to become the largest on the planet. By 1992 China and India—home to 38% of the world’s population—were producing just 7% of the world’s output, while six rich countries which accounted for just 12% of the world’s population produced half of it. In 1890 an average American was about six times better off than the average Chinese or Indian. By the early 1990s he was doing 25 times better.

There followed what Mr Subramanian and Mr Kessler call “convergence with a vengeance”. China’s pivot towards liberalisation and global markets came at a propitious time in terms of politics, business and technology. Rich economies were feeling relatively relaxed about globalisation and current-account deficits. Bill Clinton’s America, booming and confident, was little troubled by the growth of Chinese industry or by offshoring jobs to India. And the technology and managerial nous necessary to assemble and maintain complex supply chains were coming into their own, allowing firms to spread their operations between countries and across oceans.

The tumbling costs of shipping and communication sparked what Richard Baldwin, an economist at the Graduate Institute in Geneva, calls globalisation’s “second unbundling” (the first was the simple ability to provide consumers in one place with goods from another). As longer supply chains infiltrated and connected places with large and fast-growing working-age populations, enormous quantities of cheap new labour became accessible. According to figures from the McKinsey Global Institute, a think-tank, advanced economies added about 160m non-farm jobs between 1980 and 2010. Emerging economies added 900m.

Riding the whirlwind

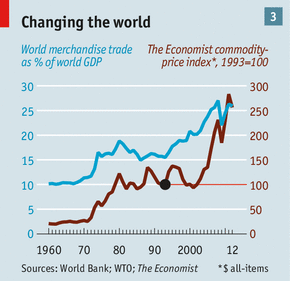

The fruits of this cheap labour were huge steps forward in global trade. Merchandise exports soared from 16% of global GDP in the mid-1990s to 27% in 2008. The Chinese share of global exports topped 11%, with trade accounting for more than half of the country’s GDP. Mr Subramanian and Mr Kessler see China as the first “mega-trader” to grace the world stage since Britain’s imperial heyday.

The growth in trade was matched by a growth in demand for commodities as China and the nations supplying it soaked up energy and raw materials such as iron ore, copper and lead (see chart 3). Prices surged, generating a bonanza for the emerging world’s commodity producers and contributing to a broad-based boom, to the great benefit both of fellow-BRICs Russia and Brazil and of smaller economies, including many in Africa.

From 1993 to 2007 China averaged growth of 10.5% a year. India, with less reliance on trade, managed an average of 6.5%, more than twice America’s average growth rate. The two countries’ combined share of global output more than doubled to nearly 16%. Global financial imbalances ballooned. From 1999 advanced economies ran a current-account deficit which peaked at nearly 1.2% of rich-world GDP in 2006. Emerging economies’ combined current-account surplus peaked in the same year at 4.9% of GDP.

Foreign-exchange interventions made the export surge doubly tricky to manage. After the financial crises of the late 1990s many emerging economies began accumulating dollar reserves to protect themselves against being caught short by big foreign-exchange outflows. Building up reserves helped the growing economies to hold exchange rates below the levels they might otherwise attain, keeping exports relatively cheap. China was a particularly enthusiastic reserve accumulator, and now sits atop a $3.5 trillion hoard, more or less all of it piled up since 2000. All told the BRICs have reserves of about $4.6 trillion.

This reserve accumulation contributed to a global savings glut, and the resulting low interest rates encouraged heavy public and private borrowing in the rich world. Some reckon currency manipulation also repressed consumption in emerging markets, so that their exports to big advanced economies like America were not offset by a corresponding rise in consumption of imports. Daron Acemoglu, David Autor and Brendan Price of the Massachusetts Institute of Technology, David Dorn, of Madrid’s Centre for Monetary and Financial Studies, and Gordon Hanson, of the University of California, San Diego, argue that the “sag” in employment growth in America in the 2000s can be blamed in large part on the country’s unreciprocated taste for Chinese imports.

Not all the effects of the BRICs’ growth were to be felt as promptly; some, for good and ill, will not be experienced in full measure for decades. Bigger economies mean bigger armies. They also mean flourishing universities: in 2030 China may have 50m more science and engineering graduates in its workforce than it did in 2010. And their growth has entailed an historic rise in greenhouse-gas emissions, now a third higher than they were in 1997, as well as heaps of local environmental damage. China is now the world’s largest carbon-dioxide emitter; America is the only non-BRIC in the top four.

But though the impact of the recent rapid change will be felt far into the future, the change itself is moderating. Various signs suggest that an important inflection point has been reached. The emerging world will continue to grow in economic importance. But the pace at which it does so will slow as the BRICs put the days of their steepest ascent behind them.

Take a deep breath

The emerging economies’ share of output is no longer rising as fast as it did in the 2000s. In 2009 the year-on-year increase in that share was almost one and a half percentage points (see chart 1). Now it is back below one percentage point. This tallies with a striking slowdown in BRIC growth rates. In 2007 China’s economy expanded by an eye-popping 14.2%. India managed 10.1% growth, Russia 8.5%, and Brazil 6.1%. The IMF now reckons China will grow by just 7.8% in 2013, India by 5.6%, and Russia and Brazil by 2.5%.

Unsurprisingly, this means that the BRIC economies are contributing less to global growth. In 2008 they accounted for two-thirds of world GDP growth. In 2011 they accounted for half of it, in 2012 a bit less than that. The IMF sees them staying at about that level for the next five years. Goldman Sachs predicts that, based on an analysis of fundamentals, the BRICs share will decline further over the long term. Other emerging markets will pick up some of the slack. Yet those markets are not expected to add enough to prevent a general easing of the pace of world growth (see chart 4).

After two decades of rapid growth the most populous emerging economies have taken advantage of most of the easiest steps on the ladder to prosperity. An illustration: in 1997 none of the fastest 100 supercomputers in the world was to be found in a BRIC. Now six computers in China grace that list, as do six from other BRICs. And one of them tops it: Tianhe-2, designed and built at the National University of Defence Technology in Changsha, crunches numbers faster than any other device in the world. That is an extraordinary achievement, and the potential for growth as such technology spreads wider is clear. But it is also an indication that the country’s growth will not now be as quick as it used to be. Bleeding-edge innovation is harder than catching up.

Other countries have impressive growth potential. Goldman Sachs touts a list of the “Next 11” which includes Bangladesh, Indonesia, Mexico, Nigeria and Turkey. But there are various reasons to think that this N11 cannot have an impact on the same scale as that of the BRICs.

The first is that these economies are smaller. The N11 has a population of just over 1.3 billion. That is less than half that of the BRICs. The N11 is barely more populous than India, which is the BRIC with the greatest possibility for growth still ahead of it, if only it could reform itself enough to put more of those people to work.

The second is that the N11 is richer now than the BRICs were back in the day. Economists reckon that the bigger the gap between a country’s output per person and that of the technological leader, the faster the economy is capable of growing. Weighted by population, the average per person output of the N11 is already 14% of that in America. When the BRIC economies began their economic surge their population-weighted output per person was just 7% of America’s. It is a measure of the continued potential for growth in India, where population has risen fast, that its figure today is still just 8%.

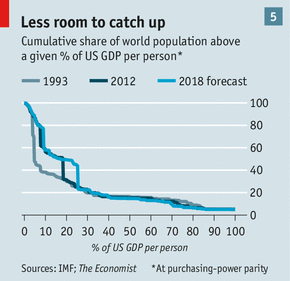

It is not just the N11. The world as a whole has less catch-up potential than it used to. Its most populous countries are no longer all that poor and its poor countries are no longer all that populous. Two decades of BRIC-led growth mean that there are far fewer people earning very little. In 1993 about half the world lived at below 5% of American GDP per person, according to an analysis of IMF figures by The Economist (see chart 5). In 2012 the equivalent figure was 18% of American GDP per person.

The third reason that the performance of the BRICs cannot be repeated is the very success of that performance. The world economy is much larger than it used to be: twice as big in real terms as it was in 1992, according to IMF figures. That means that emerging markets—whether the BRIC economies or the N11 or both—must deliver larger absolute increases in output to generate a marginal economic boost matching that seen in the 1990s and 2000s.

The same maths apply to labour markets. New additions to the workforce will henceforward have a harder time disrupting the global economy. The billion jobs that the McKinsey Global Institute sees as having been added to non-farm employment from 1980 to 2010 boosted it by 115%. If the world were to put on another billion jobs from 2010 to 2040 that would represent just a 51% increase in world employment: impressive but much less dramatic.

Making the best of it

The reality may be a good bit less dramatic still. Some developing economies will add hundreds of millions of new workers in coming years. But some of that contribution will be offset by the ageing of populations elsewhere. China’s working-age population began shrinking in 2012. India, with more favourable demographics, is struggling to create enough employment; it added no net new jobs between 2004-05 and 2009-10, according to a recent survey. Big demographic booms are brewing elsewhere: Nigeria, for example, may be more populous than America in less than 40 years. But such growth will have its peak impact only decades from now.

The way that the world economy reacted to the rise of the BRICs has also made it less prone to further shocks of a similar sort. Markets have responded to soaring commodity demand and prices. Firms and households are saving on inputs; businesses and governments have rushed to develop new resources, as seen in the shale oil-and-gas bonanza now unfolding in North America.

Currency adjustments have narrowed deficits. The Chinese yuan has appreciated by roughly 35% against the dollar since 2005. Emerging-world reserve accumulation has diminished along with current-account imbalances. Since 2011 Chinese reserves have been mostly flat. Indeed in recent years reserve outflows have been a problem for some emerging markets.

An easing in the stride of the emerging-market giants will be cause for anxiety first and foremost for the residents of those countries, where the growth that has delivered higher living standards has also whetted appetites for more. The transition need not be painful. In China a slower overall growth rate may feel fine to workers if the share of consumption in the economy rises relative to investment. In India, though, the picture is not so pretty.

A rising tide may lift all boats; a falling one reveals who has no bathing trunks on. Weaker conditions could place pressure on financial systems in emerging economies about which investors begin to worry. If central banks fail to stem capital outflows then slower growth could give way to outright contraction. Many countries will find that commodities no longer provide a crutch. David Jacks, an economist at Simon Fraser University in British Columbia who studies long-run commodity-price movements, reckons that prices may have already begun a sustained period of below-trend price growth.

Internationally, lower growth could focus leaders on increased co-operation and a new push for liberalisation. The BRIC era took place in the absence of major new trade liberalisation (though China’s entry into the World Trade Organisation was an important landmark); with trade growing so healthily anyway, the rewards were harder to appreciate. A slowdown could bring new focus to global trade talks. A deal that addressed non-tariff trade barriers, and especially those on trade in services, could yield big benefits.

There is a risk, though, that matters may move in the opposite direction. The rich world is more cautious about globalisation than it was a decade or two ago, and more interested in maintaining its export competitiveness. A century ago the world’s last great era of trade integration ended with a war and ushered in a generation of economic nationalism and international conflict. The recent proliferation of regional trade agreements could signal a move towards fractionalisation of the global economy. And slowed growth in the now-large BRICs could lead to the sort of internal tensions that countries can displace by picking external fights. Whether or not the world can build on a remarkable era of growth will depend in large part on whether the new giants tread a path towards greater global co-operation—or stumble, fall and, in the worst case, fight.