Dover is spinning off a glitzy tech unit and refocusing on heavy manufacturing. Why the strategy should pay off

July 28, 2013 Leave a comment

SATURDAY, JULY 27, 2013

Cooler Than Smartphones

By LAWRENCE C. STRAUSS | MORE ARTICLES BY AUTHOR

Dover is spinning off a glitzy tech unit and refocusing on heavy manufacturing. Why the strategy should pay off.

At first glance, you’d think the hot business at Dover is selling smartphone components. The global manufacturing conglomerate makes microphones, speakers, and other key parts for both Apple and Samsung, the dueling titans of mobility. Dover, it would seem, has found a classic sweet spot. Right? Actually, the company is exiting that business. In a laudable move to put long-term profit ahead of short-term sizzle, Dover (ticker: DOV) next year will spin off to shareholders a large chunk of its communication-technologies unit, which accounts for nearly 20% of total revenue.

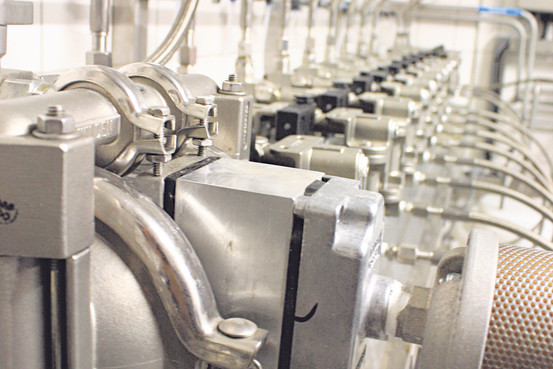

Industrial Strength: Pumps from a Dover unit transfer chemical cleaning agents at Rotterdam harbor.

You won’t find Dover’s remaining product lines in the Apple Store. They include industrial-strength fluid pumps, drilling gear for energy-exploration companies, commercial refrigeration systems, and bar-code printers. But those businesses could delight shareholders. They require less capital investment than gadget parts do, and, taken together, could produce steady, double-digit profit growth.

“The remaining businesses are more homogenous, allowing for revenue and earnings growth that is less variable,” says Nicholas Heymann, an analyst at William Blair who rates the shares Outperform. “So you don’t end up having to make a bet that this year, two out of the four businesses will have home-run years.”

The prospects for the revamped company look especially compelling when you look beyond the spinoff of the communications business, to be called Knowles. Heymann reckons that Knowles can earn 90 cents a share in 2014, and he values that company at $14 a share. Subtract that from Dover’s recent stock price of around $85 and you get $71 for the main business, or a reasonable 13 times Heymann’s 2014 earnings estimate of $5.50 per share. As earnings increase, the stock could climb about 15%—and more if the profit gains are consistent enough to win a higher multiple.

Says Vincent Sellecchia, co-manager of the Delafield fund (DEFIX), which holds the shares, “This is a better-than-average company with above-average returns and a smart management team, and it deserves a premium to its peers.” The industrial companies within the Standard & Poor’s 500 trade at about 14 times earnings.

Long-term investors can also expect some decent income. Dover’s dividend of $1.40 a share yields 1.64%, and the company has raised its payout every year for 57 straight years, evidence of strong free cash flow, a solid balance sheet, and a commitment to shareholder value. Late last year, Dover’s board authorized a $1 billion stock buyback, or about 7% of outstanding shares. Most of the buyback plan is expected to be completed this year.

BASED IN DOWNERS GROVE, Ill., Dover has built itself into a major industrial company with the help of brisk acquisitions in far-flung fields. It has bulked up strikingly well in energy-related businesses, which last year accounted for 27% of the company’s revenue but 39% of its segment profit. In a drilling technology known as artificial lift, Dover has gone from about $250 million in sales five years ago to roughly $1 billion today.

As wells age, they often need artificial pressure to harvest the resource. Dover specializes in providing equipment, such as rods and pumps, that can bring oil and gas to the surface. “Artificial lift has a long runway with recurring revenue,” says Colin Hudson, a portfolio manager of the Oakmark Equity and Income fund (OAKBX), which holds the shares. “A lot of wells are being depleted and are getting to the phase where they need artificial lift.” Hudson puts the stock’s value at $100, or 17% above the recent price.

THE CURRENT BUSINESS portfolio is largely the handiwork of Robert Livingston, CEO since 2008. His most recent big acquisition came this past December, with Dover paying $602 million for Anthony International, a California company specializing in glass doors for commercial refrigerators and freezers, among other products.

Right now, Livingston says, Dover is looking at much smaller, bolt-on deals to bolster businesses like energy and commercial refrigeration. He’ll have money for deals as a result of the spinoff, which will send some $400 million to Dover’s coffers.

The Bottom Line

Dover’s shares are poised to rise by 15% or more next year, as shrewd acquisitions pay off. Look for continued hikes in the dividend, too.

Already the Anthony International acquisition is adding to earnings, thanks to a nice fit with a longtime Dover holding called Hillphoenix. That unit specializes in refrigeration cases and back-room refrigeration systems used by retailers such as Target (TGT). Anthony also gives the company more heft in markets such as Mexico and South America, and an entrée into U.S. convenience stores.

Dover is now well-positioned to capitalize on the trend among food retailers to retrofit open refrigeration areas with doors in order to save energy. There is an estimated $2.5 billion market to retrofit the unenclosed cases in North America, and that trend “has long legs for the next eight to 10 years or longer,” Livingston tells Barron’s.

All of which helps explain why Dover’s refrigeration and food-equipment business increased revenue 26% in the second quarter from a year earlier. It was a strong quarter overall, as adjusted earnings came in at $1.36 a share, up 24% from a year earlier on a revenue gain of 9% to $2.2 billion. Confident about second-half prospects and organic growth, management raised its 2013 earnings guidance range to $5.56 to $5.71 a share, up from $5.05 to $5.35 a share.

Who needs smartphones, anyway?