Small Stocks Are in Eye of the Index; Inclusion in Russell 2000 May Distort Some Stock Values

July 29, 2013 Leave a comment

July 28, 2013, 6:46 p.m. ET

Small Stocks Are in Eye of the Index

Inclusion in Russell 2000 May Distort Some Stock Values

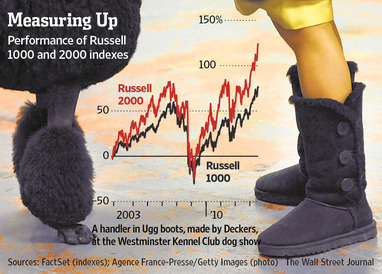

The Russell 2000 is the benchmark for small-capitalization stocks. But some stocks in it aren’t that small. This may pose a problem for investors, even as the index has been hitting all-time highs. The argument for small stocks is clear. Research has consistently shown that over long stretches small-cap stocks beat their bigger brethren. A driver has been the fraction of fast-expanding small companies on their way to becoming large ones. Yet some of them may no longer be in the Russell 2000. Which stocks Russell designates as small cap counts. The iShares Russell 2000 ETF, IWM -0.40% the ninth largest of all exchange-traded funds, has about $25 billion under management. More than 400 mutual-fund portfolios, with over $370 billion under management, use the Russell 2000, or its subindexes, as benchmarks, said Morningstar.Each June, Russell Investments rebalances its indexes. Ranking U.S. companies by market value as of May 31, it aims to assign the 1,000 largest companies to the Russell 1000 index, with the next 2,000 assigned to the Russell 2000. It sounds straightforward. But transportation and agricultural company Seaboard SEB -1.66%had a market value of $3.3 billion as of May 31 and was placed in the Russell 2000 this year. There were about 170 companies in the Russell 1000 with lower market values, according to Credit Suisse.

On the other hand, shoemaker Deckers Outdoor,DECK -9.04% in the Russell 1000, had a market value of $1.8 billion. That was lower than about 210 companies in the Russell 2000.

The inclusion of outsize companies atop the Russell 2000 may distort stock values, suggests New York money manager Horizon Kinetics.

Russell’s indexes are weighted by market float, so the more a company’s publicly available shares are worth, the more heft it carries. When the indexes were rebalanced on June 28, the top 50 stocks in the Russell 2000 counted for about 10% of its total weighting, according to Credit Suisse.

In contrast, the bottom 50 of the Russell 1000 counted for about 0.2% of that index’s weighting. As a result, a large stock that remains in the Russell 2000 rather than migrating upward is receiving an outsize flow of cash from funds that track and are benchmarked to the index.

This may be affecting valuations. As of early July, the forward price/earnings multiple for the Russell 2000’s 50 largest stocks, excluding those with expected losses, was 20.3 times versus just 16.6 times for the 50 stocks at the bottom of the Russell 1000, a Horizon Kinetics analysis found.

The less-than-clear distinction over what stocks get put into what index reflects a 2007 rule change. Before then, the largest 1,000 companies were in the Russell 1000, the 2,000 that followed were in the Russell 2000. This generated a lot of turnover as stocks flipped back and forth over the 1000th company breakpoint each year, inflicting heavy trading costs on funds tracking the indexes.

So Russell began using a calculation that places bands around the breakpoint, effectively creating a buffer that makes it harder for companies to switch indexes. The change significantly reduced turnover.

How much this affects performance isn’t clear. Russell wouldn’t provide yearly returns of the banded and unbanded indexes, saying it has historically been uncomfortable “putting simulated annual returns into the public domain because there could be comparison with actual index returns and the data may be taken out of context.”

It did offer that the annualized return differences between the banded and unbanded indexes over the period it analyzed was 1.02%. This indicates that, over 13 years, one index outperformed the other by about 14%.

That isn’t a huge difference, but it sheds no light on how the two indexes got there and potentially large swings in the intervening years.

Russell also published research in 2010 that suggested banding had little impact on performance. For the 13-year period ending in 2009, Russell said, the tracking error between a banded and nonbanded index, the annualized measure of how differences in daily returns between the indexes tended to swing from average, was 0.0163 percentage point. Asked to verify this, Russell said there was a mistake: The correct figure was 1.63 percentage points, or 100 times higher. That is still low. But tracking error doesn’t directly gauge performance. And the mistake shows the need for greater transparency. Providing daily returns would be a good start.

The original purpose of indexes was to gauge how the stock market, or a segment of it, performed. They later became benchmarks for judging managers’ performance. Most recently, they have functioned as investment products.

Simultaneously serving these three purposes—gauge, benchmark and investment—may create more problems for investors than they solve.