Green Mountain’s Buzz Poised to Wear Off; The Coffee Company’s Shares Have Had an Epic Comeback, but the Question Is How Much That Reflects Fundamentals

August 8, 2013 Leave a comment

August 6, 2013, 7:26 p.m. ET

Green Mountain’s Buzz Poised to Wear Off

The Coffee Company’s Shares Have Had an Epic Comeback, but the Question Is How Much That Reflects Fundamentals

High praise has a way of preceding big stumbles. In earlier, headier times, Green Mountain Coffee Roasters Inc.’s GMCR -2.53%machines were occasionally referred to as the iPods of coffee. Then, in the fall of 2011, questions about its growth prospects sent its shares tumbling from nearly $116 to less than $18 by the next summer. Like Apple Inc.’s music players, competition and the onward march of technology was to blame.

But the coffee company’s shares have had an epic comeback, rallying 276% in the past year to $81.32 a share. The question is how much that reflects fundamentals and how much the wild rally of recently maligned companies. Other “battleground stocks” such asTesla Motors Inc. TSLA -5.57% andNetflix Inc. NFLX -2.61% are up by 350% and 412%, respectively, over the same period. Herbalife Ltd., HLF -0.53%pilloried by short sellers late last year, is up by 164% since January.

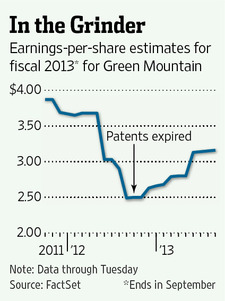

Even if Green Mountain’s fiscal third-quarter earnings, due to be released Wednesday, meet expectations, the rally could sputter. Earnings per share are seen at 73 cents, against 46 cents a year earlier. But the figures of most concern are 5,325,765 and 5,840,189. Those are the two key patent numbers for its K-Cup technology that expired last September, allowing competitors to make pods for its Keurig machines.

Earnings expectations fell through the spring but have since recovered as the loss of those patents initially proved inconsequential. Now, though, rivals may be gaining momentum. Green Mountain estimated late last year that unlicensed K-Cups would be about 5% of the market this year, rising to 15% by 2014 to 2015. Independent market research has since put that share near the high end of that range.

While Green Mountain’s share of it may be smaller, the K-Cup pie is still rising. Some 90 million U.S. households have coffee machines, and Green Mountain estimates its line will be in 16 million to 17 million of them by the end of this year.

Of course, industry growth doesn’t have to proceed at the same pace as profits. Fat margins—Green Mountain is still more profitable on an operating basis than Starbucks Corp.—attract copycats. Now trading at 27 times this year’s projected earnings, Green Mountain’s valuation doesn’t fully reflect that threat.

Investors may want switch to decaf.