Unfolding Washington Post’s Inner Value; newspaper-publishing segment of Washington Post represented just 13% of revenue and an operating loss of $49 million

August 8, 2013 Leave a comment

August 6, 2013, 5:11 p.m. ET

Unfolding Washington Post’s Inner Value

Company May Want to Consider Even Deeper Changes

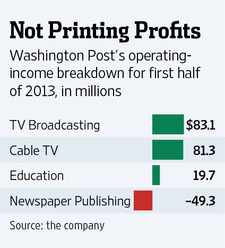

What is the Washington Post Co. WPO -0.91% without the Washington Post? Quite a lot, actually. The announcement Monday that Amazon.com Chief ExecutiveJeff Bezos will buy the Post for $250 million generated speculation about his intentions for the paper. But the sale is small in the context of Washington Post’s $4 billion enterprise value. What matters more for investors is the value, and future, of what is left. In the first half of 2013, the newspaper-publishing segment of Washington Post represented just 13% of revenue. But that segment reported an operating loss of $49 million. Selling it removes the overhang of a business in decline.In a post-Post world, the company, which will get a new name, will be primarily composed of the Kaplan education unit, the company’s Phoenix-based cable provider and its six local broadcast stations. These accounted for 54%, 20% and 9% of revenue, respectively, during the first half of 2013, with the remainder coming from other digital initiatives.

Looking at the units in terms of profits reveals a different hierarchy. Education accounted for only 17% of operating profit over the period, while cable and broadcasting delivered 70% and 72%, respectively, in part because of losses elsewhere. Indeed, local broadcasting and cable have been largely carrying the show at the Washington Post, accounting for the vast majority of operating profit over the past six quarters. Broadcasting has been particularly robust, benefiting from rising, high-margin retransmission revenue, the fees pay-TV operators fork over to carry local-station signals.

Kaplan, meanwhile, was once the profit driver of Washington Post, accounting for 31% of operating profit—the largest chunk—in 2005. But the U.S. government stepped up its scrutiny of for-profit schools, which rely disproportionately on federal loans and grants. More recently, enrollment has suffered at Kaplan and peers amid heightened competition from nonprofit and state schools. The latter have launched more online-education initiatives, capturing more of the for-profit target market. (Washington Post competes with News Corp, publisher of The Wall Street Journal.)

A further breakup of the Washington Post conglomerate, by separating broadcast and cable from education, might be the real key to unlocking value for shareholders. Based on recent deals, broadcast stations carry a valuation multiple of roughly eight times 2013 estimated Ebitda, while cable assets trade at around seven times, according to Gabelli. For-profit education once carried a double-digit multiple. But the firm says it is now worth about six times.

Washington Post might be able to garner an even higher multiple without Kaplan, while also making itself more appealing to media investors—especially as consolidation continues among local broadcast stations. Of course, spinning off Kaplan might incur additional regulatory oversight. There might be fewer hurdles to a spinoff of the broadcast and cable businesses.

Washington Post shares got a lift from the sale of its namesake newspaper. To release further value, it may want to consider an even more radical redesign.