Asia: Storm defences tested

August 29, 2013 Leave a comment

August 28, 2013 7:23 pm

Asia: Storm defences tested

By David Pilling and Josh Noble

Emerging markets are less vulnerable to shocks than they were in the late 1990s

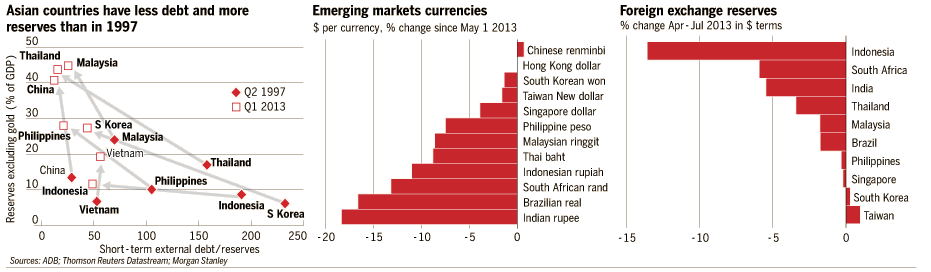

These days it seems practically everything is made in Asia. Everything, that is, apart from economic crises. For the moment, at least, those can still be produced in the US. Ever since Ben Bernanke, chairman of the US Federal Reserve, hinted in May that there may be an end in sight to the policy of aggressive monetary easing, emerging markets have been severely tested. Talk of tapering the Fed’s purchase of $85bn a month in government bonds from as early as September has pushed up long-term US interest rates. That in turn appears to have triggered a partial reversal of the carry trade in which investors borrow in dollars to purchase higher-yielding assets, often in emerging markets. Currencies and stock markets around the world, especially in countries with current account deficits financed by fickle capital inflows, have tumbled.In Asia, which came through the 2008 financial crisis seemingly unscathed, questions have been raised about economies that, until fairly recently, were counted as success stories. Indonesia, a country of 240m people with a 10-year record of solid growth, is in the spotlight as its currency and stock market slide. Between April and July, its central bank spent nearly $15bn, or 14 per cent of its total reserves, defending the rupiah, according to Morgan Stanley. In spite of that, the rupiah has fallen nearly 15 per cent against the dollar since May.

India, where problems have been brewing for some time, has become the focal point of market concernsabout countries with twin current account and fiscal deficits. Heavily dependent on energy imports and with only a limited manufacturing capability, India runs a current account deficit of about 5 per cent of gross domestic product and a fiscal deficit approaching 10 per cent of GDP if regional government debt is included. Concern about an Indian economy whose growth has halved to 5 per cent since 2010 has knocked about 20 per cent off the value of its currency in a matter of months. The rupee on Wednesday recorded its largest single-day fall in 18 years on worries that its oil import bill would rise as a result of threatened western intervention in Syria.

Even Thailand, which had been growing at about 5 per cent after recovering from devastating floods in 2011, has moved into a technical recession because of weak exports. There has also been concern about the cost of its generous rice subsidy. Since May, Bangkok’s equity market has fallen about 15 per cent.

Just as the Asian financial crisis of 1997 began with an assault on the Thai baht, so some fear that pressure on several Asian currencies could spell a new period of turmoil in a region that many thought was building up immunity. Investors had put faith in what was described as self-sustaining growth driven by urbanisation and the rise of the middle class.

Many investors are keeping faith with that long-term trend but the short-term outlook has darkened. Not only is capital being repatriated to the US, some Asian economies are also feeling the effects of a slowing China, which has been the engine of regional growth and the main factor in a commodity supercycle that now appears to have ended. The resulting turbulence is by no means limited to Asia. Countries from South Africa to Turkey and from Brazil to Australia have also been buffeted. Investors, however, will be scrutinising Asia to see whether its long, uninterrupted growth streak is now at risk.

“If the global shifts are large enough, there’s very little an emerging market economy can do about it,” says Jonathan Pincus, director of the Jakarta-based Center for Policy Research and Education, referring to the expected outflows of capital from Asia as the US economy improves.

In some ways, today’s Asian economies have little in common with their 1997 incarnations. Back then, many countries had fixed exchange rates and their companies were heavily exposed to foreign debt. As currencies came under pressure, central banks desperately spent reserves to defend them. When the peg finally broke, currencies collapsed and companies’ foreign-denominated debts soared.

Thailand, Indonesia and South Korea had to seek help from the International Monetary Fund. Partly as a result of now largely discredited IMF austerity packages, they subsequently plunged into deep recession. Indonesia, the worst affected, lost 13.5 per cent of GDP in a single year. Suharto, the dictator, was toppled.

. . .

If the global shifts are large enough, there’s little an emerging market can do about it

– Jonathan Pincus, director of the Jakarta-based Center for Policy Research and Education

Today the picture is very different. Asian economies have flexible exchange rates, much higher reserves and sounder banking systems. India, for example, has reserves to cover seven months of imports compared with only about three weeks when it had its own “come-to-IMF” moment in 1991. Nor, this time around, has India’s central bank wasted much firepower on defending the currency. Instead, it has largely allowed the rupee to slide. A weaker currency should boost exports and slow imports, closing the current account deficit automatically.

“Some of this stuff about a repeat of 1997 is well off the mark in our opinion,” says Paul Gruenwald, an economist at Standard & Poor’s. “No one’s defending the exchange rates. They’ve got more reserves than they used to. I don’t think anyone’s going to be going hat in hand to the IMF in the foreseeable future.”

Most economists agree that this will not be a rerun of 1997. But that does not mean that a different type of crisis can be excluded. “Every crisis is different,” says Ruchir Sharma of Morgan Stanley. “We only learn about the factors behind each new crisis post facto.”

One concern is that much Asian growth since 2008 has been bought on credit. Most of China’s huge 2009 stimulus package was paid for by credit expansion. Loans were sluiced through compliant, state-owned banks to favoured projects and businesses, many of them unproductive.

Public debt in China looks relatively modest, but when all debt – including private and corporate – is counted, it reaches about 200 per cent of GDP, according to HSBC. That is approaching US levels of 233 per cent. China is not alone in ratcheting up the credit. In Thailand, consumer debt has risen from 55 per cent of GDP to 77 per cent since 2008, while in Singapore it has risen from less than half of GDP to more than two-thirds. Malaysia’s household debt is at 80 per cent of GDP.

The danger of a bubble could be exacerbated in some economies by the fact that, until recently, currencies were exceptionally strong. That was the result of big inflows of money from the US that are now reversing. One consequence was that central banks kept monetary policy as loose as possible, encouraging the build-up of more credit.

“History tells us that when policy normalises, a certain amount of this debt will not be serviceable,” says Michael Spencer, an economist at Deutsche Bank. “There are people who have never had a loan before and may not fully understand what happens when interest rates go up.”

Fred Neumann, chief Asian economist at HSBC, is also concerned about the build-up of debt. “In virtually all of the Asian economies, we’re at leverage levels which make these economies very sensitive to a margin change in the cost of capital. From that perspective, it’s actually quite worrying,” he says of the prospect of further rises in US interest rates.

Some take a more alarmist view. Kevin Lai, an economist at Daiwa Securities, predicts an unfolding debt crisis. “We are talking about a huge credit bubble because in Asia we didn’t need quantitative easing in the first place,” he says. “We are talking about a potential balance of payments crisis, currency crisis and debt crisis.”

That is a minority view but even those who rule out a systemic crisis concede that some emerging economies will be stress-tested by sharp reversals in interest rates and capital flows. That could put companies under pressure if they have borrowed cheaply, particularly if, as in 1997, they are exposed to unhedged foreign currency risk.

. . .

In Asia, the spotlight has fallen on India and Indonesia. In an ideal world, says Mr Gruenwald of S&P, those countries would respond to market concern not by tinkering with capital controls, as India has done, but by pushing through bold economic reforms. Such measures could take the form of reducing budget deficits, for example by scaling back subsidies on things such as fuel or food, he says. Alternatively, they could aim to attract more capital inflows, particularly by improving the environment for foreign direct investment.

Both India and Indonesia, however, are counting down to a general election, making it far less likely that they will adopt unpopular measures. India has recently taken some steps to attract foreign investment but even if it succeeds, money is unlikely to flow in rapidly enough to offset any immediate funding needs. Walmart, the US retail group, recently put its Indian expansion plans on hold, partly because of unpredictable regulations.

Mr Sharma argues that the recent wobble is more than a market glitch. He says across-the-board growth in emerging markets in the past decade was an aberration. That has lured pundits and policy makers into believing the “convergence myth”, the process through which living standards of poorer countries inexorably close the gap with richer ones. Over the course of any given decade since the 1950s, he says, only a third of emerging markets have been able to grow consistently at 5 per cent. Only one in 10 developing countries has managed to grow by that amount for three straight decades.

In Mr Sharma’s view, many countries have failed to capitalise on a once-in-a-generation confluence of easy money and souped-up Chinese demand. As those factors wane, he suspects old patterns of growth will reassert themselves. In other words, some emerging economies will continue to grow fast but most will not. Those less geared to Chinese commodity demand will do better.

Christopher Wood, chief strategist of CLSA, a broker, says that countries are likely to be buffeted by outflows of capital if the Fed ends quantitative easing and raises short-term rates. However, he says, most Asian economies, including Indonesia, which has public debt of approximately 30 per cent of GDP, ought to be able to weather that kind of storm.

Far more worrying, he says, is the matter of whether China will be able to maintain reasonable levels of growth as it attempts to wean itself off credit-led investment. “Whether China pulls off this rebalancing is to me a million times more important than all this tapering neurosis,” he says. Asian economies, Mr Wood concludes, are strong enough to withstand economic headwinds emanating from Washington. Events that could unfold in Beijing, he says, are a different matter.