Mao-era thrift shunned for good life on credit

August 29, 2013 Leave a comment

August 28, 2013 5:00 pm

China’s consumers take eagerly to credit

By Simon Rabinovitch in Shanghai

A few years after finishing university, Jack Dai thought he had scored the holy trinity of success for a young Chinese man: a government job, an apartment and a wife. But he had not counted on one additional factor, less visible from the surface, that soon drove a wedge between him and his conception of the good life. To buy his Shanghai house, Mr Dai, 30, took out a hefty mortgage. Monthly repayments now swallow up half his salary. Plus he has the other expenses of Chinese middle-classdom – overseas holidays, shopping excursions, movies and restaurants.Mr Dai is hemmed in by debt. “Every second month or so, I can’t pay off my credit card bill. I save nothing,” he sighs.

This experience for a young professional, hardly unusual in the west, is a radical departure for China. The older generation, that of Mr Dai’s parents, was famous for its saving prowess. Memories of deprived childhoods in the Maoist era led them to squirrel away most of their earnings even as their fortunes improved alongside China’s fast-growing economy from the 1980s on.

But the young urban Chinese who have entered the workforce over the past decade grew up amid plenty, and their views about saving and spending bear little resemblance to those of their parents. Their willingness to borrow for today and worry about repayment tomorrow is beginning to reshape China’s debt dynamics.

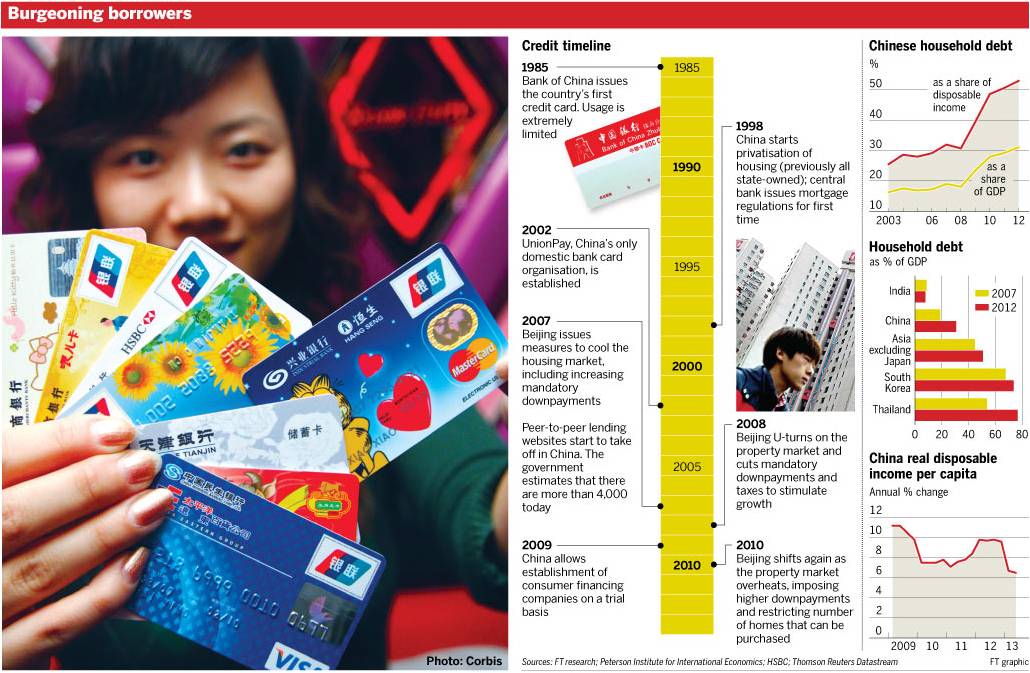

Of the three kinds of debt – government, corporate and household – the latter is barely on the radar as a risk in China. Household debt is about Rmb15tn ($2.5tn), or a third of gross domestic product, according to RBS. That is roughly half of what the government owes and a quarter of corporate debt.

Yet this snapshot misses the dramatic changes afoot. The stock of household debt has tripled over the past five years. Average household debt jumped from 30 per cent of disposable income in 2008 to 50 per cent by the end of 2011, according to the Peterson Institute for International Economics. China still has a long way to go to catch up to personal debt levels in the US or Europe – where it exceeds 100 per cent of income – but many Chinese households are making up for lost time.

“My thinking is, if you can get a loan, you should take it,” says Ray Chang, 29, a ship inspector at the port of Shanghai. “Money is worth less and less because of inflation, so it makes sense to spend it now and pay it back later.”

Nursing a mochaccino during a break from his Sunday afternoon English class (paid by credit card), the cheerful Mr Chang was sure he had his finances under control. He had only once failed to make his credit card payment on time, after a shopping binge in Hong Kong when he spent Rmb15,000 ($2,450) – more than his monthly salary – on a Longines watch. “A man needs a good watch,” he says.

By far the biggest expenditure for young Chinese is their house, with home ownership seen by many as a prerequisite for marriage. Nearly 90 per cent of Chinese own their own homes, according to a survey by the Southwestern University of Finance and Economics, well above the global average of 63 per cent.

The government has strict rules in place to limit the amount of debt that can be incurred in buying a house. Homebuyers must make at least 30 per cent of their purchase up front in cash to obtain a mortgage, far less risky than the US before the subprime crisis when zero down payment mortgages were widely available.

But it is rare for new professionals in China to stump up so much money on their own. Both Mr Dai and Mr Chang, like many of their peers, relied on their parents for the entirety of their downpayments.

Beyond turning to their elders for deposits or other purchases, Chinese have a growing array of options to borrow cash. Banks are getting into consumer financing; small-loan companies have taken off; online peer-to-peer lending companies are also booming. The central bank says the small-loan sector has now pumped out more than Rmb700bn in credit, a tenfold rise since 2009.

Regulators have so far been tolerant, even encouraging the development of these new lending platforms. It hopes the surge of consumer credit will help wean the Chinese economy off its addiction to investment and make consumption a bigger driver of growth.

“It’s like the wild west,” says Roger Ying, who last year founded Pandai, one of the 200-plus peer-to-peer lending websites established since 2007. These sites let people with surplus funds lend to others who want money, whether to buy a computer or a car, or simply as extra capital. “Consumer financing could become a bubble. People are doing reckless lending.”

Annualised lending rates average roughly 15 per cent in the small-loan sector, more than twice benchmark bank loan rates. A Stanford graduate, Mr Ying has developed a system that takes a small cut from each deal to create an insurance fund in case a borrower can’t repay a loan. While default rates among small Chinese lenders are still low at just about 1 per cent of their total loan books, they are beginning to creep up.

Money is worth less and less because of inflation, so it makes sense to spend it now and pay it back later

– Ray Chang, ship inspector

Disputes over defaults can end up in courts, but the Chinese legal system struggles to enforce judgments. So for particularly tough cases, some lenders are instead turning to collection agencies like the one run by Wang Taifu out of a suburban Shanghai law office. He used to receive one or two enquiries a day from prospective clients; that’s up to five or six now.

With his law degree, rimless glasses and short-sleeve dress shirt, Mr Wang doesn’t look like a heavy. He only employs them. “If you want to collect debt in China, you have to be tough. You’ve got to push people. My speciality is that I do this within the bounds of the law.”

He refuses to divulge his techniques, apart from saying that he typically sends four people to collect cash and, unlike some competitors, does not bundle debtors into a van, drive them to the countryside and douse them in cold water.

Mercifully, very few Chinese have had a collection agency knock on their door. But many are now facing an equally unfamiliar, if slightly less nerve-racking, challenge of slowing economic growth.

Both Mr Dai, the Shanghai bureaucrat, and Mr Chang, the ship inspector, had assumed things could only get better, with wages steadily increasing. But the government froze Mr Dai’s pay, while Mr Chang’s company cut his this year. Across China, white-collar incomes are increasing at their slowest rate since the global financial crisis.

Mr Dai’s response was to quit his government job last month, giving up the stability of a civil service career for a more uncertain but potentially more lucrative future with an insurance company.

Mr Chang is not changing jobs. In fact, he remains unflappable in his optimism. Having seen his current apartment rise in value, he is thinking about upgrading to a bigger house. The downpayment will once again be beyond his reach and will even stretch his parents’ savings. But he has thought of a solution.

“We can use my parents’ house as collateral for a loan.”