Restaurant Boom Bodes Ill for Korea Economy; fried chicken joints started by families who used their homes as collateral for loans is part of a broader swelling of the nation’s household debt to levels approaching those in the U.S. before the housing bust

September 14, 2013 Leave a comment

September 13, 2013, 6:45 p.m. ET

Restaurant Boom Bodes Ill for Korea Economy

ALEX FRANGOS and KWANWOO JUN

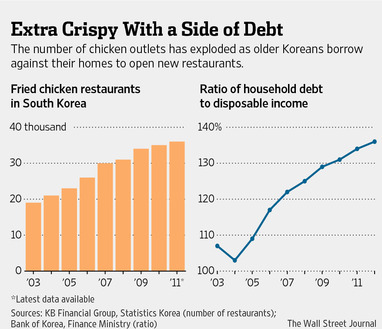

SEOUL—Korean fried chicken—crunchy, tasty and usually served with pitchers of cold beer—has become a culinary phenomenon far beyond the country’s shores. But at home, it is a source of worry for the struggling economy. In neighborhood after neighborhood, South Korean cities are crowded with greasy fried chicken joints started by families who used their homes as collateral for loans. Chicken-fueled credit is part of a broader swelling of the nation’s household debt to levels approaching those in the U.S. before the housing bust. “If anyone would start doing this business, I would stop him by all means,” says Kang Hyo-seon, who at 51 years old speeds around Seoul on a motorcycle delivering boxes of fried chicken.His family’s cubbyhole-size restaurant was the second in his neighborhood when it opened eight years ago. Now there are four. “Things got worse as people began cramming into the market,” he says.

The Korean government is trying to slow the growth of chicken restaurants—which tripled to 36,000 over the past 10 years—amid concern about the rising household debt burden, which is seen as a drag on economic growth.

While it is unlikely a burst fried chicken bubble alone would take down Korea’s financial system, a sharp rise in defaults would damp consumer spending and make banks reluctant to lend.

Gross domestic product grew just 2% last year, its slowest rate since the 2009 financial crisis, partly as a result of poor domestic demand on top of weaker demand for Korean exports.

Similar trends can be seen across Asia, where debt levels are rising to record highs thanks to historically low interest rates, raising concerns that some countries are using debt to fuel unsustainable growth.

Malaysia has recently clamped down on mortgage lending, as have Singapore and Hong Kong, where property booms since 2009 have come with sharp increases in consumer debt.

In Korea, though, many people are borrowing not for new cars or appliances but out of necessity, because of a quirk in the country’s retirement system.

Employees of big companies are often forced to retire in their 50s, yet pensions are too small to live on, so many open up small businesses. A quarter of Korea’s 24 million workers are self-employed, compared with about 6% in the U.S., but among working Koreans in their 50s, the number jumps to 32%.

Seoul-based KB Financial Group says 7,400 new fried chicken restaurants open each year in South Korea, while 5,000 existing ones go bankrupt. Nearly half fail within three years and 80% go out of business within 10 years.

The government this spring introduced a plan to help low-income borrowers who fall six months or more behind on debts of 100 million won (roughly $100,000) or less. A $1.3 billion fund covers the cost for banks to extend their loans by up to 10 years or write off up to half of their debt.

So far, 155,000 people have taken advantage of the program, but the number is considered a drop in the bucket.

Household debt in Korea rose to a record 136% of disposable income at the end of 2012 compared with 103% in 2004. (U.S. household debt has declined to 105% of disposable income, from 140% in 2007.)

“It is significant, and it’s dangerous,” says Joon-Ho Hahm, an economist at Korea’s Yonsei University who has studied household debt.

“Lots of baby-boomer retirees are using property as collateral to open chicken and pizza places,” he said. “They are using household debt to open noncompetitive small businesses.”

Korea has 12 restaurants per 1,000 people, more than twice the concentration of Japan and six times as many as the U.S., according to the Korea Foodservice Industry Association.

Korean fried chicken, fried twice to make it extra crispy and often served with pickled radish, took off during the 2002 soccer World Cup, which Korea co-hosted with Japan. Many fried chicken joints, known as “chimaek” a combination of the Korean words for chicken and beer, rolled out big-screen television sets for fans to watch the games.

Last year, the government banned restaurant franchises from opening two outlets within 800 meters, or half a mile, of each other.

Similar rules apply to bakeries, pizzerias and coffee houses, which fill city blocks because of all the mom-and-pop shops.

In her 13 years running a fried chicken business, Seong Myeong-sik, 65 years old, has observed no public holidays and works 15 hours a day, until midnight. She still can’t pay her debts, and has missed payments to her government-backed lenders.

“Many retirees may have jumped into this business so easily, but success will never come that easily,” she said.

When she opened in 2000, there were only three chicken joints in her western Seoul neighborhood. Today there are 11. She’s lucky, though: The government is redeveloping her neighborhood and is paying her to move out.

“No more fried chicken business,” she says, sitting in her cramped restaurant.