The asset-quality review: Close scrutiny of Europe’s banks may turn up unexpected shortfalls

October 6, 2013 Leave a comment

The asset-quality review: Close scrutiny of Europe’s banks may turn up unexpected shortfalls

Oct 5th 2013 |From the print edition

THE ink on the agreements that will hand supervision of the euro area’s biggest banks to the European Central Bank (ECB) is barely dry. Yet the ECB is already enmeshed in squabbles with national banking supervisors over the extent of its powers and the rigour with which it will undertake its first big task, a warts-and-all review of the balance-sheets of the banks it will take charge of in a year’s time.Details over how the ECB will conduct this asset-quality review (AQR) will probably be released in the second half of October, but the outlines are already beginning to emerge. The main aim of the review is to ensure that the ECB is not embarrassed by the revelation of holes in the balance-sheets of its new charges. Fresh in its mind is the example of the European Banking Authority (EBA), a young European regulator that lost much of its credibility after the collapse of banks that had passed its stress tests only months earlier.

To avoid that danger the ECB is emphasising that the AQR is not a stress test, which would simulate the effect of various economic scenarios on banks’ balance-sheets. Instead it is doing a preliminary examination to ensure that it understands what is on banks’ books in the first place. National regulators fret that they will be embarrassed by what it finds. This has prompted some to push back hard to limit the scope of the ECB’s inquiries.

Surprisingly, this resistance is not coming from countries on Europe’s periphery such as Spain (see article), which have much to gain from the imprimatur of ECB supervision. Rather it is coming from core countries such as France and, to a lesser extent, Germany, where seemingly well-capitalised banks may come out of the asset review looking threadbare.

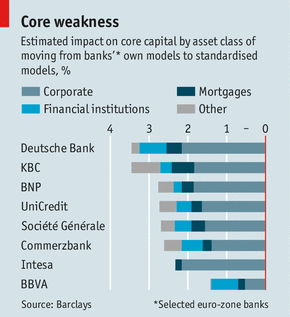

One issue is the “risk weighting” of assets, a process by which banks adjust the size of their capital buffer to account for the riskiness of their lending. Studies by both the Basel Committee, a club of central bankers and supervisors, and the EBA have found wide and unjustifiable variations in the way banks risk-weight their assets, even when asked to do so for identical hypothetical portfolios. The consequences of such variations can be significant. If the euro area’s biggest banks were forced to abandon their internal risk-weighting models and instead apply cruder standardised models, many would see their core-capital ratios decline by several percentage points (see chart). The ECB is likely to push for greater consistency in risk weighting, which could force banks in France, Germany and elsewhere to raise capital.

Informed observers also expect the ECB to find evidence of “regulatory forbearance” in these markets, whereby supervisors have allowed banks to fudge the level of non-performing loans on their books, restructuring loans and easing repayment terms instead of taking write-downs. Adjusting for this could also open up capital holes. A process devised by Germany and France to shore up confidence in weak banks on Europe’s periphery may end up hitting a quite unexpected target.