Malaysian play in Singapore gone awry

October 12, 2013 Leave a comment

Updated: Saturday October 12, 2013 MYT 7:15:31 AM

Malaysian play in Singapore gone awry

BY RISEN JAYASEELAN AND TEE LIN SAY

WHAT a mess. The fallout stemming from the massive sell-off of Blumont Group Ltd,Asiasons Capital Ltd and LionGold Corp Ltd is rocking the foundation of these companies and raising questions. With such battered share prices and with the billions having been wiped out from their market capitalisation, the model of using their highly liquid SGX-quoted shares, as currency for takeovers, is in jeopardy. Then there’s the stigma to deal with: will bankers, business partners and vendors of assets be as open to deal with them as before?The saga has also got punters (at least those who aren’t sitting on huge losses from holdings in these companies) wondering if there’s a play at these current share prices. After all, Blumont is now trading at 17.1 Singapore cents, a far cry from the near S$2.50 level it was at just weeks ago.

A Singapore-based broker says: “Investors are enquiring. They are examining what are in these companies. Some think it could be a cheap entry, considering the many acquisitions that have been made by these companies.”

Others are staying away. “These companies have to build themselves from scratch. We can’t assess the fallout yet,” said a Malaysian-based investor. Then there are sceptics who reckon that these companies are part of a house of cards that has begun to unravel. From the Malaysian context, they are putting these companies in the same breath of the dramatic falls seen in the share prices of Iris Corp Bhd andHarvest Court Industries Bhd.

Naturally, the concern is whether there was manipulation during the sudden steep acceleration of the share prices of the SGX trio. It is left to be seen if any investigation or charges are brought about on any parties related to this saga.

The last time SGX applied the designated-security framework was in April 2008, when the bourse imposed trading curbs on Jade Technologies, now known as Cedar Strategic Holdings, following a failed bid by its president to buy out the engineering and commodities-services firm. Those curbs were lifted after two days, while the curbs on these three companies have continued for five straight days with little indication of when it is going to end.

The owners and management of Asiasons say that their share price gyrations over the last week or so has got little to do with the business they are in.

Datuk Jared Lim, a former investment banker with Avenue Securities Sdn Bhd who had in 2007 teamed up with former Bursa chairman Datuk Mohammed Azlan Hashimto establish the listed private equity company, Asiasons, offers his explanation of what transpired and his prognosis for his company.

“We appear to be the victims of a very coordinated short-selling effort. There were untrue malicious rumours circulating at the time the short selling started,” he says, adding that operationally, its business as usual.

“It will take time for our stock price to find its equilibrium, post the designation. And once that happens, we will continue life from there,” he says.

The same applies for Blumont and LionGold it seems. Big name mining personalityAlex Molyneux, a Hong-Kong based former Asia pacific head of metals and mining atCitigroup, swooped in with a plan to buy a 5.2% block of Blumont at the depressed indicative price of S$0.40 per share.

Saying that’s there tremendous value in Blumont because of its depressed share price, Molyneux also was the main spokesperson for Blumont at its press conference last Tuesday. While he articulated the position of Blumont exceptionally well, it did give the impression that there was a lack of a strong leadership of the company prior to Molyneux’s appearance. CEO James Hong addressed questions more related to historical earnings and the SGX designation, affirming though that there is no investigation being done on Blumont by any of the Singapore market regulators.

A tenuous link?

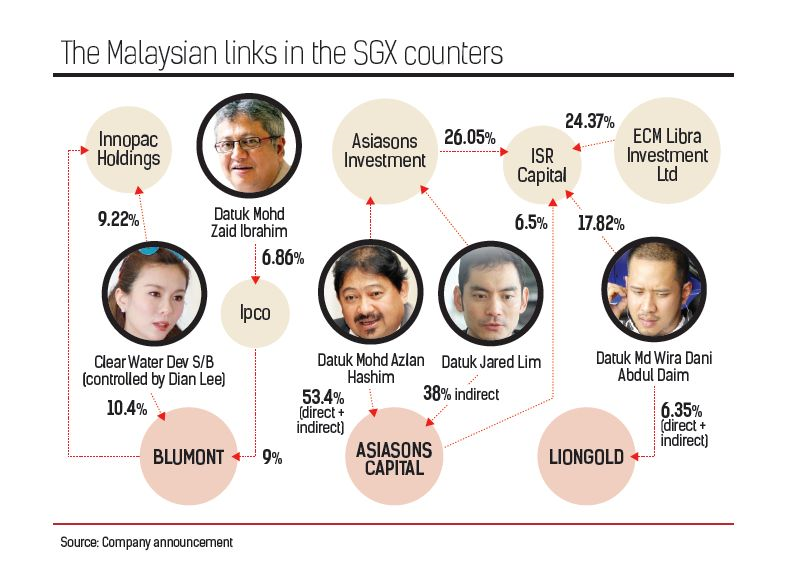

While reports have highlighted that the companies involved in the selldown were linked through a complex web of shareholdings, it is difficult to prove those companies are controlled by one group or party.

As for the links between the companies, Asiason’s Lim, who incidentally is the son-in-law of Tan Sri Lee Kim Yew of Country Heights fame, is flustered with this “mosaic theory”. “The links are tenuous at best. We invested an 8.72% in LionGold when it was in its early growth stage”. As for his wife Dian Lee’s stake in Blumont, he says that was to do with her company Clearwater Development Sdn Bhd selling some units of their project to Blumont, at a time when the latter was active in property. Again that deal was paid for in shares.

Delving deeper, Asiasons has a 26% stake in another SGX-listed company ISR Capital. Datuk Md Wira Dani Daim (son of former finance minister Tun Daim Zainuddin) also owns close to 18% in ISR. Wira Dani also owns 6.35% in LionGold. The explanation: Lim and Azlan had initially invested in ISR, which had a financial advisory license. They later formed Asiasons and decided to whittle down their stake in ISR and the buyer of that stake was Wira Daim, who incidentally also invested in LionGold. “It is more an instance of common shareholders and what’s wrong with that?” quips Lim, adding “We have no involvement in either Blumont or LionGold except for the investments we hold”.

The acquisitive strategy of significant mining assets aboard by LionGold and Blumont have attracted the attention of big name investors. For example, New York-based asset manager Van Eck Associates owns about 6% of LionGold while Australia-based Macquarie Group has another 4.78% of the company. Blackrock and Invesco hold 0.57% and 0.56% respectively of Asiasons while Vanguard Group and Van Eck hold 0.27% and 0.15% of Blumont, Bloomberg reported. All these funds are sitting on significant paper losses, the Bloomberg report stated. In August, LionGold had been included in the MSCI Small Cap Index while Asiasons is on the FTSE ST Small Cap Index.

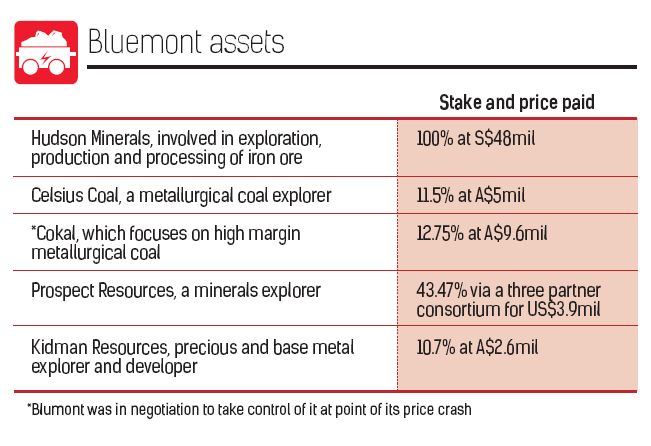

Aside from Molyneux, Blumont has a joint venture with Ines Scotland, said to be one of Australia’s most successful mining executives in the copper sector. The JV called Blumont Copper, seeks to identify investment opportunities in that sector.

LionGold had in fact emerged as some sort of poster boy for the SGX. In a presentation about listing on the SGX dated May this year, LionGold was highlighted as a notable company in SGX’s “minerals cluster”, enjoying a high turnover velocity, a successful trail of acquisitions and rise in market values.

The spectacular collapse after a steep rise in the share prices of the those companies have now caused tongues to wag.

Names of shadowy figures behind the scene are whispered in circles in Malaysia, who are quite used to the idea of “operators” pushing up share prices of stocks onBursa Malaysia in the past.

The rumour mill is in overdrive with the view that one Malaysian-tycoon is the invisible hand behind all the three companies as well as handful of others on the SGX, that are linked to this group.

If indeed that is true, it is an impressive feat.

Stratospheric rises and lofty valuations

Blumont was trading at a mere 6 cents a share last August. But it hit a high of S$2.45 barely a year later and there were recent sharp rises in recent times. The same applied for LionGold and Asiasons.

In Asiason’s case, the spike came after they announced a plan to acquire an oil and gas firm, Black Elk, primarily via share issuances at a price of S$2.19 a share. Prior to that the share price was said to see a steady rise as investors began to take notice of the deals the company was executing.

The deal for Black Elk was at a due diligence stage prior to the panic selling of those three stocks and now would have to be reassessed considering Asiason’s depressed share price. The deal could likely be scuttled although insiders say that discussions are still ongoing.

The fact remains that the spike up in prices of all these stocks had no earnings to support them.

Blumont’s Molyneux had this to say at the recent press conference on the valuation of mineral companies: “Resources in the ground is like having gold bullions in your safe, discounted of course to its extraction cost. Mineral companies have value before they have revenue,” he said, adding that major mining companies were valued this way abroad.

The stocks, nonetheless, were trading at mind-boggling trailing price earnings multiples and book values, caused mainly by a steep and sudden surge in the share prices of those companies.

The lofty and unsubstantiated valuations led these stocks to become targets of short sellers, an activity which is allowed in the SGX market, unlike Malaysia’s regulated version.

Sentiment surrounding these stocks were not helped by the trading restrictions imposed on them by one major Singapore broker, which had placed more than 10 stocks on its restriction list.

That drew attention of the short sellers who went in for blood after the steep rise. The subsequent price collapse then led to the SGX taking notice and designating these stocks.

Reports in the Singapore press have alluded to the fact that the SGX’s move could have exacerbated the situation. There was also a comment that SGX should have acted earlier when the SGX-trio shares prices were reaching stratospheric heights.

The plunge of the three companies has compelled the Singapore Stock Exchange to add circuit breakers into the system by early next year.

Separately, the SGX said that it is investigating the short-selling in shares of Blumont and Asiasons, even with trading curbs imposed on the two stocks.

SGX’s head of market surveillance Kelvin Koh said: “There was short-selling in the two designated counters, Asiasons Capital and Blumont Group, on Monday, contrary to the trading directions given to the designated securities.

“We will be investigating these cases and take the appropriate disciplinary actions as necessary.”

SGX said it will assess the trading conditions of the three stocks and lift the designation, when appropriate.

Earnings impact

For Asiasons further damage is yet to come. The company will likely suffer an impairment loss from having to mark-to-market the decreased value of its 8.72% in LionGold, which some reckon could be in the range of S$50mil or S$60mil. This hit would in turn negatively impact its shareholders funds and book value.

But Lim points out that it would only be a one-off impairment. “LionGold continues to hold one of the largest gold reserves in the region and its price too will find its equilibrium once this force selling and panic is over,” Lim says, adding “In the meantime Asiasons continues to go about its business of investing.”

Another impact though is that vendors of assets who had taken the shares of Blumont and LionGold as payment would now be in a bad spot. However, insiders say that such investors had a lot of opportunity to liquidate their positions, considering that the share prices of Blumont and LionGold had appreciated post most of the deals and that those stocks had enjoyed highly liquid trading activity. However it is unknown how many of such holders were fortunate enough to have exited then.

Sentiment had been strong

Sceptics reckon that the recent sell down of these Malaysian-controlled stocks leave a bad taste among investors in Singapore. And they speculate that this incident will impact other Malaysian stocks listed there.

Interestingly, some investors point out that all three stocks were in fact part of a recent Malaysian-themed run up. The proposed takeover of Albedo Ltd, the company that is aiming to be an Iskandar Development Region property player through a reverse takeover deal by Malaysian tycoon Tan Sri Danny Tan, was also in the limelight in August.

Investors were touting it as ‘another Rowsley Ltd in the making’. Rowsley is controlled by Singaporean billionaire Peter Lim.

Loss-making steel trader Albedo was actively traded in August, with volumes surpassing the billion mark.

Albedo said it would be able to continue, citing its fund raising exercises and continued support from its principal bankers

In June, the company said it had entered into a MOU to buy Coeur Gold Armenia Ltd, a gold miner in Armenia. It aborted the purchase on Aug 16 and four days later announced its intention to buy land in Iskandar, Johor.

Albedo’s shares quadrupled from 2 cents to about 7.6 cents in August.

About the same time that the Blumont, Asiasons and LionGold started tumbling, Albedo also fell sharply, and is now hovering at the 4.6 cents level. But says one Singapore broker, “I wouldn’t say that this saga has cast a shadow on Malaysia companies per se. Investors are honing in on whether these companies had real, legitimate businesses”.

Brokers also said that prior to the designation of the stocks on Oct 4, sentiment had been strong.

“People were crazy for these stocks. These were known companies. On and off, there would be news articles on the mergers and acquisitions done by these companies,” said one Singaporean broker. Now that all stocks have plummeted, he said that questions were kicking in, and investors were starting to pay more attention to the businesses of these companies.

“Of course people are panicking. These stocks took a year to go up, and lost 90% of that value in 3 days.”