Building the Cloud: Who Wins, Who Loses; Traditional IT suppliers, including EMC, Cisco, and NetApp, are under siege from cloud operators like Amazon and Google. Pricey start-ups abound. A second chance for VMware

October 13, 2013 Leave a comment

SATURDAY, OCTOBER 12, 2013

Building the Cloud: Who Wins, Who Loses

By TIERNAN RAY | MORE ARTICLES BY AUTHOR

Traditional IT suppliers, including EMC, Cisco, and NetApp, are under siege from cloud operators like Amazon and Google. Pricey start-ups abound. A second chance for VMware.

The cloud changes everything. The technology leaders of the past, including Hewlett-Packard , Cisco Systems , and EMC ,face unprecedented threats as computing moves out of corporate data centers and onto the cloud that companies like Google ,Amazon.com , and others have created. Over the past decade, these large Web companies have figured out how to build more-efficient computing facilities than the information-technology teams within large companies could ever imagine. Now these firms are renting their vast computing firepower to companies large and small. Amazon has multiple customers who run SAP(ticker: SAP) enterprise resource planning software, among the heaviest of traditional enterprise applications, for their critical planning. Social networking application SnapChat runs on Google’s App Engine.And as cloud computing rises, the market for enterprise wares is shrinking. It started with server computers, which became more of a commodity as so-called virtualization software allowed workloads to be easily moved from one box to another. Networking equipment could be the next segment of IT gear to be commoditized, eventually followed by storage equipment.

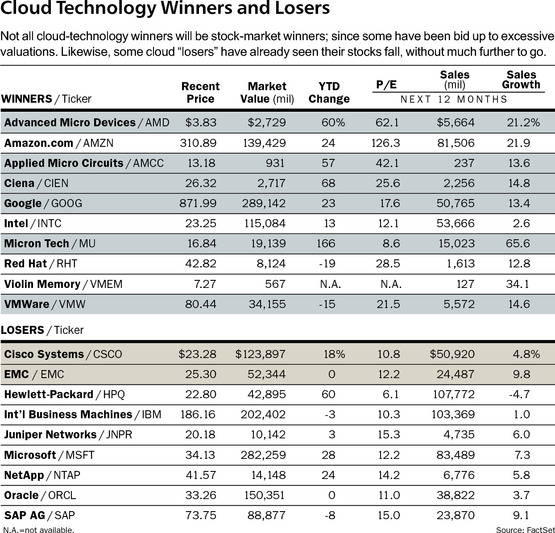

Winners, in addition to Google (GOOG) and Amazon (AMZN), could be chip makersAdvanced Micro Devices (AMD) and Applied Micro Circuits (AMCC), networkerCiena (CIEN), younger firms such as Splunk (SPLK), and service providers like Verizon Communications (VZ). Losers could include Juniper Networks (JNPR), NetApp(NTAP), Oracle (ORCL), and SAP.

Not all of the technology winners will be stock-market winners because some have been bid up to excessive valuations. And not all the losers will be market losers, because investors have already tossed them in the ash heap. The table below highlights opportunities in both groups.

THE NIGHTMARE SCENARIO for technology vendors is that Amazon and Google and other cloud operators could end up as the new IT shop, replacing the internal data centers that enterprises have traditionally built. After all, a company like Amazon that buys software and hardware to support tens of billions of dollars in commerce will ultimately offer more-cost-efficient computing than even the best IT shops can build themselves.

Not only would that reduce the amount of software and hardware that enterprises buy, but also it puts Google and Amazon and other cloud providers in a far more powerful position as buyers of that gear, pressuring vendors’ prices and profit margins.

“Large organizations have tended to buy high-end machines that have lots of resources and features for tasks,” observes long-time industry watcher Dan Kusnetzky, director of the eponymous Kusnetzky Group consulting firm. “If more and more tasks are being moved into data centers of service providers, those providers will start to control what is purchased, and they will tend not to want the high-end machines.” Meaning, the companies that are building the cloud are buying less of the leading name-brand equipment in favor of simple servers, network switches, and disk drives.

The cloud’s threat to the already-struggling enterprise market has some longtime tech investors spooked. “I am cautious about overall IT spending growth rates going forward, especially for the major names such as Oracle, SAP, and Microsoft [MSFT],” says portfolio manager Dan Niles of AlphaOne Capital Partners. “This is due to the trend of slowing gross-domestic-product growth, the cloud making more efficient use of resources, and companies switching to a subscription model for IT, which slows near-term spending.”

ONE THING THE CLOUD underscores is that the value of the technology is in the software, not hardware. Software is what gives Microsoft its 74% gross profit margin. And it’s software wrapped in a pretty box—not chips and transceivers and sheet metal wrapped around the outside—that gives Cisco (CSCO) a healthy 60% gross margin. But they may not be able to transition fast enough—and that makes them ripe for attack.

The cloud is already sucking some value out of traditional IT products. Google has designed sophisticated software of its own that lets it bundle together cheap, off-the-shelf disk drives, servers, and network switches to achieve the same—if not greater—performance and reliability as pricey equipment and software from EMC, Cisco, and Oracle. Amazon, too, uses proprietary software to tie together a lot of commodity hardware for its Amazon Web Services, or AWS, which is the purest example of cloud computing as a public service.

One of the most potentially significant of the new cloud builders is Verizon Cloud. The telecom giant eschews traditional server computers from Hewlett-Packard (HPQ) andDell (DELL) in favor of custom-built boxes designed in partnership with AMD. Instead of Cisco switches, Verizon has designed its own networking software that runs on those servers. Instead of traditional storage systems from EMC (EMC) and NetApp, which control the many disk drives that hold data, Verizon wrote its own storage code to manage drives connected to each server.

Although only a speck on the company’s $116 billion in revenue, Verizon Cloud holds the promise of growth for a company in a slow-growth industry.

AWS and Verizon and other service providers could gain more momentum from new programming tools that are making it easier to move software applications out of a company’s data center and into the cloud. There are a wide range of start-ups, OpenShift software from Linux vendor Red Hat (RHT), and tools vendor Pivotal Labs, a joint venture between EMC and VMware (VMW). OpenShift and Linux are open-source software, meaning they require no license fees, though companies do pay for support.

While server vendors are under siege, there’s still value in chip suppliers lntel (INTC) and AMD, which continue to power computing, no matter how generic the server used. Intel has 90% of the market for the processors that run the servers, but AMD could move up next year with deals such as helping to construct the Verizon Cloud.

Another name to watch is networking-chip maker Applied Micro Circuits, which is moving into server chips. Because of its networking expertise, some believe its processors could make servers more adept at moving computing tasks throughout the cloud.

NETWORK EQUIPMENT, FROM the likes of market leaders Cisco and Juniper Networks, is being teed up. New software technologies from a host of start-ups are “pulling apart the switch to the point where the network-control functions are just an app running on a server,” says Alan Weckel, a networking analyst at the Dell’Oro Group, a market research firm. Using these programs, an enterprise could buy inexpensive white-box networking gear in place of complex switching equipment, just as Verizon is doing. Verizon Cloud is in beta now, rolling out through 2014.

Some wonder if Cisco can maintain the premium its software has garnered in the wake of this attack. “Cisco has an installed base and a revenue stream and a margin model they are trying to protect,” says Joe Skorupa of Gartner. “That revenue model went away in servers years ago, when customers moved away from Sun Microsystems, and it could go away here, too.”

Competitors argue that Cisco is vulnerable because its gear doesn’t fit the cloud. The most prominent competitor is closely held Arista Networks, which is supplying Verizon Cloud’s data center. Wall Street analysts speculate that it could go public next year at a valuation of $2.5 billion.

“Traditional networking software has too much unneeded bloat and lacks programmability,” argues Arista CEO Jayshree Ullal, who was a Cisco executive for 15 years. “Cisco gear has a tangle of spaghetti code with multiple software versions, she says. Arista’s switches, by contrast, run Linux, which can be more easily programmed than a Cisco box.

Cisco CEO John Chambers acknowledges the threat from cloud providers using white-box switch gear. As for Arista, he told Barron’s that his company has faced 100 start-ups like Arista over the years, and always come out on top. Just wait, he says, till Cisco next month takes the wraps off its Arista killer, the start-up called Insieme, which Cisco funded.

One vendor that may have bright prospects is Ciena. The provider of fiber-optic equipment has positioned its gear as a fast connection between data centers. As more and more communication happens between clouds, that could give a lift to Ciena’s sales.

THE LAST PIECE OF the data center to face commoditization will be data storage, the domain of EMC and NetApp. Storage is arguably the area of the data center most resistant to change because disk drives hold all of a company’s priceless data, which isn’t something to be tampered with cavalierly.

That hasn’t discouraged a raft of storage start-ups, such as Violin Memory (VMEM), that argue that EMC’s and NetApp’s software, much like Cisco’s, is overly complicated and not well adapted to the mix of cheap hard drives and flash-memory chips that will increasingly make up the private cloud. Violin already has beaten EMC to the punch in sales of storage arrays built entirely out of flash memory chips.

One beneficiary of the flash craze could be chip maker Micron Technology (MU), a premier supplier of chips.

The start-ups point to the fact that open-source software is already changing the way data are stored on disks and flash chips. A widely used program called Hadoop scatters copies of data across scores of drives. The disk drive becomes the ultimate commodity: If it fails, a company can swap it for another. That erodes some of the value of the storage array, with its robust protections against failure.

EMC’s head of product operations, Jeremy Burton, maintains the company is at heart a software firm. He insists EMC can do just fine if customers buy disk drives from someone else and let EMC’s technology manage it all. “Increasingly, yes, we will support our software on other people’s [storage] hardware. We’ve proved over 30 years we are better at storage software than anyone,” he says.

Gartner analyst Gene Ruth agrees the start-up threat is overblown, but not to be ignored. The cloud does bring at least one real risk for EMC and NetApp: To hold on to their enterprise franchise, they must build software that lets companies move their data into the cloud, and that’s a double-edged sword. “Customers really want a NetApp or EMC box that provisions local storage, but also cloud storage—like a gateway between the two,” he says. That’s technically possible, but “the moment NetApp or EMC do that is the moment they start selling fewer drives, because the data that go into the cloud never come back.”

Another established enterprise player whose fate hangs in the balance is VMware. Its virtualization software made enterprise IT more efficient and has drastically reduced the importance of the underlying servers, sucking the value out of servers from Hewlett-Packard and Dell. But some alternate software programs are trying to beat it at its own game. One is KVM, which is built into every copy of the Linux operating system. Another, Xen, is the software that Verizon is using.

Critics say VMware has almost no share in the public-cloud market, and the saturation of its enterprise market has slowed its sales growth to perhaps just 13% this year from 22% last year.

VMware CEO Pat Gelsinger retorts that one way of measuring its penetration into the cloud is to look at how many virtual computers use VMware’s code versus KVM and Xen. He notes that there are perhaps 40 million virtual computers in the world running on VMware, compared with a mere 2.5 million running inside Amazon. Gelsinger’s next goal is to expand into virtualizing storage and networking.

THE SO-CALLED PRIVATE CLOUD—data centers built inside the enterprise that have the desirable attributes of Amazon, Google, or Verizon—will help support some traditional players. Many companies aren’t yet willing to turn their IT departments over to someone else, but still want the kind of efficiencies that the cloud brings, such as lower maintenance and expansion costs. Cisco, EMC, and VMware hope those enterprise customers will keep buying as they build their own private clouds.

Over time, however, companies will move their computing work to public-cloud providers such as Amazon. The economics are just too compelling. And that’s why investors have fallen all over themselves to bid up shares of more than a dozen tiny cloud companies, including FireEye (FEYE) and Textura (TXTR), which trade for 42 times and 31 times trailing revenue, respectively. Experience shows that not all of these companies will thrive—or even survive.

Meanwhile, some firms that have been tossed aside could still be winners for investors. EMC, for one, “has tremendous customer loyalty, and it has been adept at jumping on every new tech trend,” says Tony Ursillo, an analyst with Loomis Sayles. The fact that EMC owns 80% of VMware means its storage business is undervalued at a forward price/earnings ratio of just 12. Cisco’s multiple of 10 times forward earnings estimates, and its 3% dividend yield, makes it an intriguing value investment, even though its glory days are well past.