Omnichannel Alchemy: Turning Online Grocery Sales to Gold

October 22, 2013 Leave a comment

Omnichannel Alchemy: Turning Online Grocery Sales to Gold

by Chris Biggs and Julian Suhren

OCTOBER 02, 2013

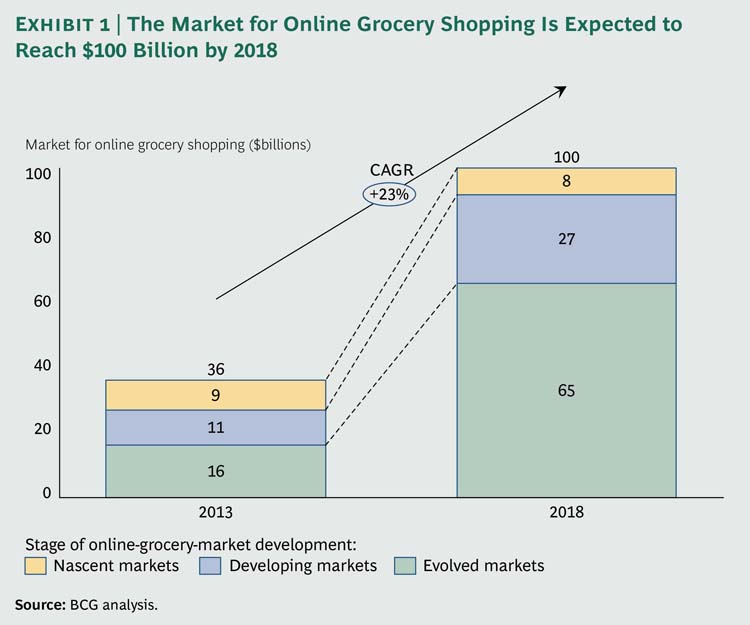

Ask most industry executives about the prospects for online grocery shopping, and you’ll encounter hesitancy, if not skepticism. Ask consumers—especially younger, more affluent consumers and families—and they’ll tell you that they are excited by the idea. They wonder why the industry has been slow to deliver. Online grocery shopping has yet to take off in most countries for many reasons—cost, logistical complexity, and the prospects for profitability key among them. There’s also the fact that many of the business’s early pioneers went bust. We believe that the prevailing doubtful view is about to hit its expiration date. We expect the global online grocery market to reach $100 billion by 2018. (See Exhibit 1.) Based onnew consumer research in eight countries1, as well as on our experience with leading companies around the world, we also believe that establishing profitable online grocery operations is not only possible, it is essential for those that want to continue to grow and maintain market leadership. Early movers will seize a significant competitive advantage over those that come late to the game.

Skeptics will point to the early failures and the fact that even today plenty of players still struggle to hit volume and profitability targets. High costs for delivery and the picking and packing of orders, combined with the need for flawless execution to keep customers coming back, make the online game challenging, to say the least. Cannibalization and different ways of accounting for costs complicate fair comparisons. Still, we believe that grocers in most markets can establish profitable, substantial online businesses with positive returns on investment and healthy margins within a period of a few years. Companies as diverse as Tesco and Fresh Direct have done it. And even if a grocer does not believe that it can drive incremental profits through an online service, it nonetheless needs to act or risk losing out in a race for omnichannel sales.

Skeptics will point to the early failures and the fact that even today plenty of players still struggle to hit volume and profitability targets. High costs for delivery and the picking and packing of orders, combined with the need for flawless execution to keep customers coming back, make the online game challenging, to say the least. Cannibalization and different ways of accounting for costs complicate fair comparisons. Still, we believe that grocers in most markets can establish profitable, substantial online businesses with positive returns on investment and healthy margins within a period of a few years. Companies as diverse as Tesco and Fresh Direct have done it. And even if a grocer does not believe that it can drive incremental profits through an online service, it nonetheless needs to act or risk losing out in a race for omnichannel sales.

Grocers are pursuing a broad range of models and approaches, but we have identified four fundamental imperatives for building a successful online grocery business. This game plan can be applied to most markets and company circumstances:

Don’t wait. Seize the opportunity now to lock in core customers and drive share.

Avoid the costly last mile. Start out with the “click and collect” model, in which a customer chooses goods online and then picks them up at a store or a dedicated facility, and add home delivery in selected areas only after sufficient local scale has been achieved.

Target affordable differentiation. Invest in the drivers of online satisfaction. Focus on the elements of the customer value proposition that will attract and retain shoppers while keeping a careful eye on the economics of execution.

Evolve and adapt. Whatever model a grocer begins with will need to evolve over time as the market and customer base—and the company’s own capabilities—develop. Plan a journey with a realistic timetable and return targets.

Don’t Wait

Our research indicates that there’s plenty of pent-up demand in major markets, even after factoring in the tendency of respondents in surveys such as this one to overstate demand.

Consumers in the countries we surveyed said that they would expect to use an online grocery service offering either a click-and-collect option or home delivery an average of 13.5 times a year—more than once a month. In some markets, such as Brazil and China, consumers would shop for groceries online nearly twice a month. In the United States, approximately half of the respondents said that they would try home delivery or a click-and-collect service. Our research also shows that grocers’ most important customers—young families and affluent couples—are especially ready to take advantage of online grocery shopping. (See Exhibit 2.) And when they do move online, they are likely to spend far more across all channels than they would have done by shopping only in the traditional way—the uplift often ranges from 30 to 50 percent.

The difference in penetration rates among markets is much more about supply than demand. Any market in which two or three grocers engage in an online fight for customers sees a substantial rise in online penetration as the competing companies invest in building and marketing their offers. Online grocery shopping has already reached a substantial size in several countries: 5 percent of the total grocery market in the U.K., for example, 3 percent in France, and 4 percent in South Korea. The online share of grocery shopping is growing at rates of 20 to 50 percent per year in leading markets and should double in many markets by 2016. The difference between the leaders and the countries in which online grocery shopping has yet to establish a significant presence has a lot more to do with the reluctance of retailers than the desires of consumers.

Big players in countries with developed online markets, such as Tesco in the U.K., already attribute a substantial proportion of their overall grocery sales to online purchasing—8 percent in Tesco’s case. An even higher percentage of these companies’ yearly growth is driven by online sales. In large and competitive grocery markets, such as the U.S. and Germany, the competition for share is intense and becoming more so, thus limiting the ability to grow by adding stores. Moreover, in most instances, an online grocery operation is a much lower-cost growth option, and it can help grocers address current drivers of dissatisfaction among customers, such as the lack of assistance with carrying packed bags and boxes to their cars.

Even so, many grocers are taking a wait-and-see approach to moving online, and they are doing so for three key reasons: cost, cannibalization, and complacency. Companies and markets vary, of course, but we believe that in countries with widespread Internet access and fast-rising mobile penetration, the viability of online grocery shopping is a question of how soon rather than if. The advantages of moving early outweigh those of waiting to see what happens.

Cost. In the decade or so since the first pioneers tried to make online grocery shopping work, costs have come down. New models, such as a click-and-collect service, are cheaper to operate at low volumes. Technology has advanced significantly; efficient automated picking systems enable some dedicated fulfillment centers to operate at a cost well below 10 percent of sales—and a few approach 5 percent. Better routing and delivery software has resulted in fuel savings and optimal fleet utilization, lowering delivery costs. At the same time, consumers are growing more accustomed to shopping online, websites and mobile applications are easier to use, and online payments are more secure.

Cannibalization. Our experience has shown that fears of cannibalization are overstated. Indeed, the dynamics of online marketing allow first movers to increase share aggressively, develop customer loyalty, and lock in the most attractive customer segments. Moreover, early movers climb the learning curve ahead of the pack, building scale and improving service, operations, and marketing. The experience of companies such as Tesco, LeShop, and Fresh Direct demonstrate that online operations can achieve profitability relatively quickly while establishing strong market positions. On the other hand, companies that allow competitors to establish an unchallenged online service risk losing customers—perhaps permanently.

Complacency. A false sense of security about the strength of a company’s current position in the market can lead to underestimating the threats from both traditional and nontraditional competitors. Many traditional grocers are testing online grocery shopping through trials in almost all major markets. There are also a host of mounting threats, including:

Nontraditional competitors, including e-retailers such as Ocado and Fresh Direct.

Online marketplaces, such as Amazon.com and Soap.com, that sell ambient, or nonperishable, goods. Amazon.com recently expanded its fresh-food offering to Los Angeles from its original trial city of Seattle.

Over-the-border competitors, such as Peapod, owned by Ahold of the Netherlands, which has introduced a mobile shopping service for rail commuters in Philadelphia. Customers use their smartphones to scan product codes on train station billboards and have the groceries delivered to their homes later that day.

Consumer goods companies looking to sell directly through various online channels, which can include third parties such as Amazon.com; their own online stores—P&G eStore, for example; or potentially their own click-and-collect types of service. We are already seeing more expensive, higher-margin, long-tail ambient goods going online through online marketplaces.

Avoid the Costly Last Mile

As BCG has observed before, click-and-collect services are gaining popularity in many markets, particularly where home delivery is problematic. (See “Digital’s Disruption of Consumer Goods and Retail (https://www.bcgperspectives.com/content/articles/retail_consumer_products_digitals_disruption/),” BCG article, November 2012.) Major grocers in France, the largest market for click-and-collect services, have established more than 2,000 such physical sites, many operated as drive-throughs. (See “Click-and-Collect Services Gain Favor in France,” below.) These sites have fueled online-sales growth of 50 percent per year for the past several years. Groupe Auchan offers an innovative combination model based on a dedicated facility that allows customers to shop for fresh goods when they pick up their online orders. Asda, the number-two U.K. grocer by size, is investing £700 million in 2013, much of it in the company’s online operation, and plans to offer a same-day click-and-collect service, a first for the U.K. market.

Click-and-Collect Services Gain Favor in France

In the French online grocery market, as in many others, the early pioneers stumbled—in large part because of the high costs of home delivery.

In 2004, Groupe Auchan and Système U piloted the click-and-collect concept, known in France as “the drive”; in fact, Intermarché has branded its service “Le Drive.” Auchan rolled it out across France later that year. E-retailer Chronodrive was founded in the same year and operates a system using regional-warehouse picking and packing and designated customer pickup points. French grocers were quick to respond; the click-and-collect model was adapted by many others, although companies continue to experiment with different forms of the collection half of the equation.

The online grocery market grew at about 30 percent per year until 2008 when, thanks to aggressive competition from new entrants, the overall growth rate accelerated to 50 percent per year from 2008 to 2013. In 2012, the online grocery market represented 2.9 percent of the total French grocery market. It is projected to reach €3 billion to €3.5 billion in 2013, and forecasts show that it will grow to about 7 percent of the total grocery market by 2016. Home delivery is not yet a factor. French grocers also are taking the click-and-collect concept to other countries, including Auchan in China and Carrefour in Indonesia.

The question of which will be the winning collection model—pickup points in or near stores or free-standing dedicated facilities—remains unanswered. There is a strong argument that dedicated facilities reduce the risk of substantial cannibalization of existing stores.

It is especially important for new entrants to select one delivery channel, or one channel in each region of operation, so they can build volume quickly without fragmenting sales between click-and-collect services and home delivery. We believe that the click-and-collect model is the best for markets in which home delivery has yet to be established. Our research shows that customers in most markets consider the service attractive and are willing to drive up to 13 minutes, on average, to pick up an order—a figure that was remarkably consistent across the eight countries we surveyed. Our research also indicates that consumers are not willing to pay delivery fees that are high enough to cover the last-mile cost of a new entrant. In the U.S., for example, consumers are willing to pay from $5 to $10 per delivery, while our models show that the actual cost to grocers can run as high as $20 per delivery in low-penetration areas.

In part for historical reasons, the U.K. has become the leading home-delivery market. Some innovative companies in other countries, such as Fresh Direct in the U.S. and LeShop in Switzerland, are also demonstrating success. But they are doing so in markets with high gross margins and particular characteristics: densely populated, supermarket-unfriendly New York City, for example, or Switzerland, where supermarkets’ hours of operation are often restricted by law. These companies have built scale quickly, and they employ innovative models. Like many successful companies, they also offer short delivery windows of an hour or two—one of the most important considerations for consumers. We expect to see more innovation in delivery models in the near future. For example, some companies have started to combine multiple deliveries in locations convenient for both the grocer and its customers, such as office buildings, to help reduce last-mile costs.

Fresh Direct has hundreds of thousands of customers and delivers fresh, high-quality foods and grocery items to homes and offices in the New York City and Philadelphia metropolitan areas. The company is profitable, generating revenues of $400 million in 2012. LeShop offers a full range of products from Migros, Switzerland’s biggest supermarket chain, and uses the Swiss post-office fleet during downtimes—from approximately 6:00 p.m. to 8:00 p.m. on weekdays and 7:00 a.m. to 1:00 p.m. on Saturdays—to handle deliveries. The company has developed special packaging that helps keep fresh and frozen foods cool to allow for delivery when no one is home.

Home delivery will continue to develop as major players experiment with new models. Google is testing same-day home delivery of groceries with various partners in the San Francisco Bay area in the U.S. Executives of Wal-Mart Stores have said that a crowdsourced solution may be possible within a year or two, with customers taking on the task of delivering to others in return for a discount. In the near to medium term, however, grocers in most markets are likely to pursue the click-and-collect model.

Target Affordable Differentiation

Succeeding in the online world takes more than a website with a mobile app and a fulfillment facility. It is critical to understand what elements are really important to customers and how you can differentiate your services from the competition without straining your economics. Customers tend to be even more demanding online than in the store. Our research shows that customers in two of the most developed online grocery markets, the U.K. and France, look for grocers to meet four basic expectations: the right range and quality of products; consistent delivery of the expected basket of goods, with low rates of substitution and high levels of freshness; punctual delivery in convenient time slots; and ease of use of the service, especially on the website. (See Exhibit 3.) One key for success is satisfying these drivers of demand on a continuing basis. Another is meeting expectations while maintaining profitable economics. Doing both means thinking through the customer value proposition and the back-end operating model in parallel.

Product Range and Quality. Most online grocers will need to find the right tradeoff between offering an attractive range of products and providing fast delivery. Because consumers like choice, adding variety normally boosts sales—and it’s easy to offer an almost endless selection online: Amazon.com, for example, lists thousands of SKUs of facial moisturizer. But providing groceries is as much about efficiency as selection; each company needs to find its own balance. For Auchan, that means listing fewer than 8,000 SKUs online but offering same-day click-and-collect pickup.

Faster delivery is one reason to limit selection; reducing complexity is another. Ordering groceries online is often a time-consuming task—placing an order can take up to an hour—and consumers who must wade through too many SKUs online often become exasperated and abandon the process. Many grocers are trying to reduce order time by, for example, maintaining loyalty-card records of previous shopping visits and giving customers overviews of both online and offline purchases. This practice has the added benefit of allowing companies to combine customer insights from both channels. Some companies offer suggested shopping lists for families based on criteria such as the number and ages of children. One online grocer even allows customers to import shopping lists from competitors’ sites.

Perhaps more important, from the grocer’s perspective, adding SKUs increases the inefficiency of the picking operation. Companies fulfilling online orders by picking in stores will have a built-in check on the number of SKUs they offer: the online selection is about the same as the range of goods in the store. Grocers using regional warehouses should resist the temptation to increase their available selection too much. They will find that stocking and picking a large range of products can come at a significant cost.

Delivering What Customers Want. Product availability is one of the key satisfaction drivers for online customers, and a high level of availability can be a big differentiator. But providing such a level of availability, like offering an extensive selection, can be costly. It also requires near-seamless supply-chain execution. Fulfilling orders from stores makes availability especially challenging. In-store customers are much more willing to decide on a good substitute or adapt their shopping lists. Online shoppers often are not satisfied with substitutes or find that they’ve received all the ingredients for a meal—except the most important one. It doesn’t take many such frustrations before they decide not to come back. Online grocers need to focus on building a back-end model that enables them to deliver on their value proposition from the beginning.

Delivering When Customers Want—and at a Fair Charge. Meeting customers’ delivery expectations with regard to timing is one of the trickiest aspects of the online operation. It’s a big driver of satisfaction, and it can be an even bigger factor in a company’s costs. Many online grocers use free delivery to attract customers—a critical mistake, in our view. Not only do such offers undercut profitability, but they also take away key levers for controlling when customers book their deliveries, an important key to managing delivery costs. Time-constrained discounts or digital coupons can provide similar incentives and shift order volume from busy to slower periods in stores or fulfillment centers.

Addressing the delivery conundrum is still an immature science, and companies have shown limited innovation so far. However, some grocers have started to differentiate their delivery pricing to increase customer loyalty. Amazon.com’s Prime Fresh, which offers benefits such as free grocery shipping in return for an annual subscription fee of $299 in the U.S., is one example. The company’s Big Radish customer-recognition program is another. It sets spending thresholds and order minimums to qualify for free delivery. Ocado’s Smart Pass offers a package of benefits that include free delivery and product discounts with a pricing structure that rewards customers for placing their orders midweek instead of on weekends. Waitrose, in the U.K., recently announced the launch of temperature-controlled delivery lockers for click-and-collect customers both in stores and at remote locations. We expect to see greater innovation in the future as companies seek to reward loyal customers and expand the use of pricing to influence customer behavior in ways that benefit the economics of the business. Personalization of service is likely to be at the heart of such efforts.

Ease of Use. It may seem self-evident, but customers respond to a state-of-the-art website that is easy and intuitive to use. Good design can be a strong tool for creating customer loyalty and avoiding churn. Increasingly, the same goes for an easy-to-use mobile app. Ocado reports that 28 percent of its online orders in 2012 were placed through a mobile device. Furthermore, best-in-class companies leverage their easy-to-use websites to encourage impulse buying. One technique, for example, is to make a small number of relevant product suggestions during the check-out process based on the customer’s profile and shopping history.

We have argued previously that two demographic realities—the maturing of the Millennial generation and the fact that the vast majority of the world’s population lives in developing markets—mean that for a large and growing share of users, especially younger ones, the digital experience will be entirely mobile. (See Through the Mobile Looking Glass: The Transformative Potential of Mobile Technologies(https://www.bcgperspectives.com/content/articles/telecommunications_digital_economy_through_the_mobile_looking_glass/), BCG Focus, April 2013.) This is a phenomenon that very few companies, in all industries, have adequately addressed and for which most are poorly prepared.

Meeting Expectations on a Continuing Basis. A significant percentage of customers try out online grocery offers once and once only; if the experience disappoints, they do not return. The best companies make sure that they deliver flawless service to all first-time customers—especially in the startup phase.

Satisfaction is an ongoing challenge, however. Established players spend two to three times more on retaining customers than on attracting new ones. The once linear route through the classic purchasing funnel has morphed into a fluid and dynamic process; the purchase pathway is often quite complex. The phenomenon known as “e-influence”—continuous input from multiple sources—also has become increasingly pervasive, further blurring boundaries between marketing and selling, both online and offline. Companies that fail to offer—or do a poor job of delivering—satisfying omnichannel experiences risk the rapid erosion of their customer base as users migrate to the firms that do deliver. Established online players look for cost-effective innovations at each step of the purchase pathway to keep customers coming back. (See Exhibit 4.)

Evolve and Adapt

It’s still early days in almost all online grocery markets. Established companies and newcomers alike should expect their models to evolve as their markets and customer bases—and their own capabilities—develop. For one thing, there is no single picking model that is right for all companies and situations. Efficiency depends in large part on individual market circumstances and where a grocer stands on the online growth curve. Most players currently focus on four models: a click-and-collect service with in-store picking, a click-and-collect service with picking performed at regional fulfillment centers, home delivery from the store, and home delivery from regional warehouses. They vary in how they got to where they are today, however.

Tesco, for example, started with home delivery from the store and then moved to regional-warehouse picking and click-and-collect models once it had built sufficient scale. (See “Tesco’s U.K. Journey,” below.) Others have begun with a click-and-collect service from the store and moved to regional fulfillment centers in locations where volume merits the shift. Tesco’s approach required a small initial investment and gave the company low delivery costs to start. Ocado has invested in large, cross-regional or national warehouses, trading off highly efficient picking at big facilities with the significantly higher last-mile delivery costs that arise because of the distance that orders must travel.

Tesco’s U.K. Journey

Tesco is an early pioneer in online grocery shopping and was the first U.K. grocer to offer an online service that featured home delivery. More than a decade ago, the company rapidly rolled out its store-based approach, achieving 97 percent coverage of the country while its competitors were still piloting or ramping up their own online offers. Tesco has continuously developed its model to improve efficiency, and the company purposely invested only in core areas of the proposition that really mattered to customers. Both of those moves were key to the company’s becoming the first online grocery provider to achieve profitability only a few years after setting up the service.

All of Tesco’s major competitors have followed the company online in the past decade, with the exception of Wm Morrison Supermarkets. Ocado was the first pure e-retailer to enter the market in 2002. Morrisons and Ocado recently announced a partnership in which Ocado will license its technology and infrastructure to Morrisons to help the latter accelerate its access to the market. The new Morrisons online grocery service is expected to launch in 2014.

Tesco started the transition from in-store to regional-warehouse picking and fulfillment in 2005 in areas where the store-based model could no longer meet demand. The company remains the market leader, with a share of approximately 45 percent. Even with increased competition, Tesco is still achieving profitability. The company has now started rolling out its online model internationally, including to China and Thailand.

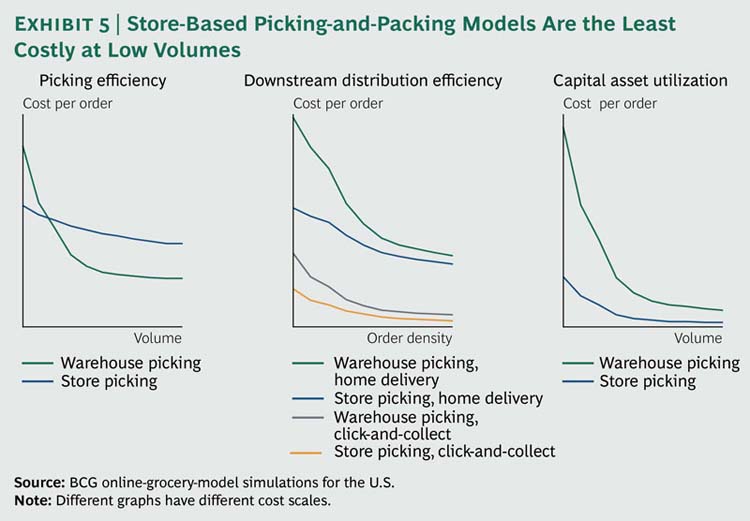

For companies getting into the online game early, in-store picking most effectively leverages existing assets as the business ramps up. For grocers piloting home delivery, having stores located close to customers helps keep delivery costs down. But as volumes grow and stores become strained to provide efficient picking and consistent service levels, grocers can move to regional warehouses. (See Exhibit 5.) We believe that, in the medium-to-longer term, regional warehouses will be the winning picking model—not just because they are efficient but also because they can provide higher service levels. National warehouses in larger countries supported by regional spokes, in our view, come with prohibitively high delivery costs.

Whatever the model, a strong link between the online operation and the company’s existing supply chain is critical because it is the key to providing fresh products through the online channel. The efficiency of the picking operation will also depend on the front-end value proposition. For example, order cutoff times drive picking efficiency, while complex substitution criteria can reduce it.

Smart grocers moving online will let the market, customer base, and the speed at which they can develop their own capabilities dictate the pace of their evolution. In markets where there is significant pent-up demand, companies can grow more aggressively. The key question is whether the company is willing to make substantial upfront investments, primarily in infrastructure, or whether it prefers to use existing assets for as long as possible while growing at a more moderate pace. In our view, absent a competitive imperative to build scale quickly, brick-and-mortar grocers expanding online should leverage existing assets and build their capabilities over time. Nobody learns to play like an expert in a complex new game right away. Learning curves are key. Service quality is likely to rise significantly in the initial years of a new operation.

We believe that first movers following our roadmap can reach profitability in a few years’ time. Once markets become more competitive and service levels rise, profitability becomes more challenging, but companies that target realistic returns are successful even in more advanced markets. (See “The Big Opportunity in the Nascent U.S. Market,” below.)

The Big Opportunity in the Nascent U.S. Market

The United States is the world’s largest e-commerce market, and it is still growing fast: spending is expected to rise by more than 13 percent to some $260 billion in 2013, according to Forrester Research. Online grocery shopping, however, remains an exception: penetration in the U.S. trails that of many other countries.

Few of the large players in the U.S. have established online operations, but notable exceptions include Peapod, which is owned by the Dutch company Ahold, and Safeway. Some niche players have also established profitable businesses; the best known is probably Fresh Direct in and around New York City and Philadelphia.

This situation could be ripe for change. BCG research shows substantial pent-up demand—more than 40 percent of U.S. consumers want to do more online grocery shopping. At the same time, large players are experimenting with different online formats. Two of the biggest, Wal-Mart Stores and Amazon.com, have sufficient scale to transform the market.

Wal-Mart is testing multiple online business models through trials, including same-day and next-day delivery of online groceries and general merchandise in the San Francisco Bay area.

Amazon.com, under its Subscribe & Save program, will deliver a standing order of consumer staples at regular, customer-specified intervals. The company recently expanded its AmazonFresh grocery-delivery service to parts of Los Angeles, where it offers same-day delivery on orders of $35 or more. Customers can choose from more than 500,000 items. Amazon.com is also testing delivery from centralized distribution facilities to “parcel lockers”—temporary storage facilities for nonperishable goods in convenient locations where individual online orders are held for pickup. The company piloted the concept in New York, Seattle, and London and has now expanded to additional markets. BCG estimates that parcel lockers can reduce the cost of delivery by as much as 30 to 40 percent compared with direct delivery to the home.

Ahold has moved beyond home delivery and is now offering a store-based click-and-collect service that allows customers to order online at Peapod.com and then collect their groceries at selected Stop & Shop stores.

The prize is substantial. Applying current U.K. penetration growth and penetration rates to the U.S. indicates a market potential of more than $24 billion in a few years’ time. While home delivery is likely to be profitable only in the densest cities, we are convinced that the click-and-collect service can be profitable across the U.S. With the right model, we believe that early movers can achieve an attractive profit margin within about five years after startup.

Grocery stores aren’t going away. Consumers around the world like them, and grocers do a good job of meeting customer demand and expectations. But the rise of omnichannel retailing—the interaction of consumers and retailers anytime, anywhere, on any kind of digital device—is the most significant and far-reaching development shaping the retail industry today. Grocers will not be spared its impact.

Successful companies have already shown how to harness this trend to their advantage. The experience of grocers in countries such as the U.K. and France demonstrates that even in their youthful days, online markets can quickly become highly competitive. The question for major players in nascent markets is whether they want to leverage their existing assets now to establish strong and defensible online businesses or wait until the market develops and they have to claw back share from others—when they are already behind the online curve.