Corporate armistice: Can South Korea’s big and small companies thrive together?

October 27, 2013 Leave a comment

Corporate armistice: Can South Korea’s big and small companies thrive together?

Oct 26th 2013 |From the print edition

LOTTE WORLD IN the Songpa district of Seoul boasts the world’s biggest indoor theme park. Trolleys shaped like hot-air balloons hang from a rail circumnavigating the glass roof. From this vantage point visitors can survey the ice rink, carousel, rollercoaster and other attractions below. A young couple wearing leopard-ear headbands have come from Yongin, where Samsung has an amusement park of its own. Which is better? They are both good, they say, but Samsung’s also has a zoo.Samsung may be South Korea’s most successful chaebol but Lotte is “probably the most ubiquitous”, says Daniel Tudor, a former correspondent of this newspaper, in his book “Korea: The Impossible Country”. The group employs over 110,000 people in its retail, tourism, petrochemicals, construction and finance affiliates. South Koreans, he writes, can buy Lotte chocolate bars, enjoy a film at a Lotte cinema, shop at a Lotte Mart, pay with one of the group’s credit cards and return home to a Lotte flat protected by Lotte insurance. Even outside its amusement parks, South Koreans can live in a Lotte world.

In South Korea it can be hard not to be a chaebolcustomer. Two out of every three cars sold in the country are made by Hyundai, the country’s second-biggestchaebol, or its affiliate, Kia Motors. And it is highly desirable to be a chaebol employee. But it is tough to be one of their competitors or suppliers. Nor is it all that rewarding to be a chaebol investor, unless you are one of a narrow clique of insiders who often exercise disproportionate control over the group.

The government is making some progress in addressing these complaints, albeit slowly, says Shaun Cochran of CLSA, a broker. President Park’s “genius has been to draw the distinction between the chaebol as institutions and the families that control them”, he explains. That “enables her to straddle left and right”. She is not against the chaebol, but she is opposed to their controlling families enriching their children at the expense of the group.

Giants can’t tiptoe

The problem of chaebol power is not just about family control, however. Even a professionally managedchaebol, run for the benefit of its minority shareholders, could wield undue market power, overcharging customers, underpaying suppliers and buying out entrepreneurial rivals for less than they are worth. Reforms to corporate governance will improve the distribution of the spoils. But is there any way to prevent the chaebolgenerating unfair spoils in the first place?

They build their empires both horizontally, spreading outwards from one industry and sector to the next, and vertically, spreading up and down from one stage of production to another. In some markets the chaebol’s dominance may allow them to stifle competition. Last year the Fair Trade Commission (FTC) collected record fines for collusion and other abuses. The year before it detected price-fixing for a bewildering variety of products, from soyabean milk to cheese, instant coffee, oil, life insurance, wallpaper and karaoke machines.

The chaebol’s customers are no longer as captive as they were. Over the past nine years South Korea has concluded nine free-trade agreements, bringing down tariffs, so consumers have the choice of buying imported goods. The government has also tried to strengthen suppliers by allowing small-business co-operatives to negotiate disputes on their behalf.

Such efforts are welcome, but a second initiative, to reserve some sectors for small firms, is less so. In 2010 nine representatives of the conglomerates (including Lotte and Samsung Electronics) and nine small firms formed a National Commission for Corporate Partnership (NCCP) which earlier this year suggested that big companies tread lightly in about 100 designated sectors, including restaurants, car repair and bicycle sales. Some big firms with plans to invest in those sectors cancelled them, says Yoo Jang-hee of the NCCP.

This is counterproductive. If the service sector remains small-scale and inefficient, it will not provide an attractive alternative outlet for the country’s capital and labour. The chaebol’s size and reach can create the potential for abuse, but that is no reason to forgo the gains from their economies of scale altogether. Indeed, if South Korea is to sustain productivity growth, its chaebol may have to spread themselves even wider. As the country has grown richer, its manufacturers have accounted for a declining share of employment. Between 1995 and 2010 their output increased by an average of 7% a year but their employment fell by 2% annually.

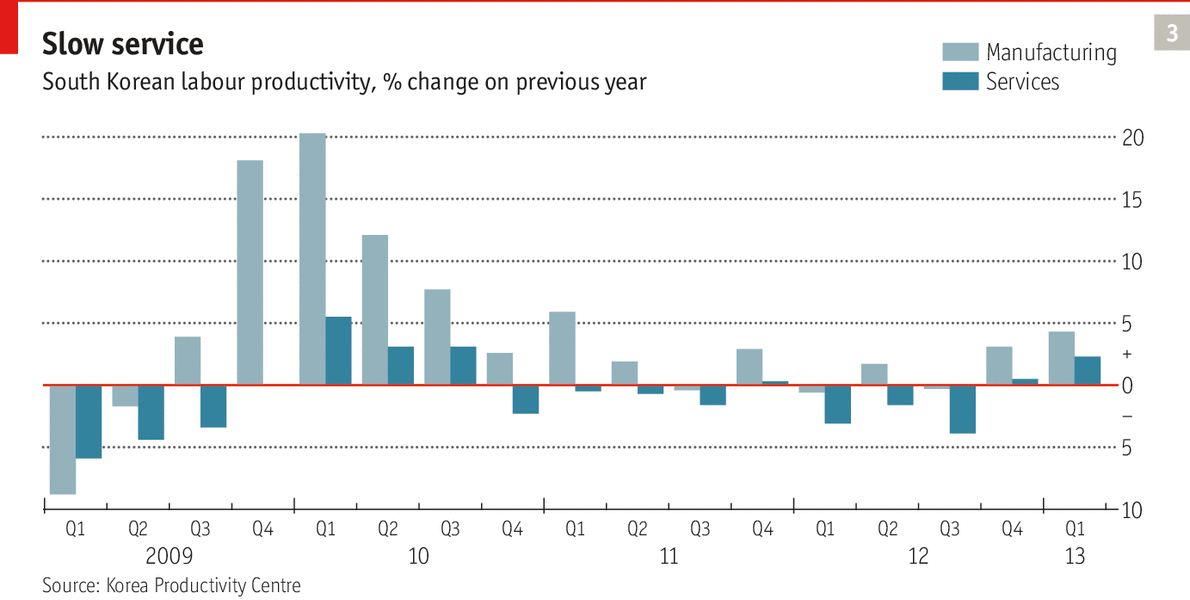

More jobs will instead be created in services, especially those that cannot be imported. But South Korea’s labour productivity in services averages only half its level in manufacturing, according to the OECD. Services may be lagging because the chaebol have not paid enough attention to them, argues Richard Dobbs of the McKinsey Global Institute in Seoul. The chaebol still attract the country’s best minds, managers and workers, so the service sector misses out on these.

Small firms attract a lot of public sympathy. They benefit from over 1,100 support programmes run by 13 central-government agencies and 16 local governments. They get this help because they generate most of the country’s employment. But that is because services, where small firms predominate, are intrinsically labour-intensive, not because the firms that supply them are small. If the chaebol were to move into services, they would also hire a lot of people and boost output per job. “If you look at the vibrant service companies around the world, most of them are largish companies,” says Mr Dobbs.

As the South Korean economy has struggled this year, the government’s energies have shifted from curbing the chaebol to what it calls “the creative economy”. It hopes to draw on South Korea’s twin strengths in technology and popular culture. The South Koreans, once known as the Irish of Asia because of their penchant for singing, carousing and romantic melancholia, have spent the past five decades building a rather German industrial miracle. Now their economic ambitions are turning to the lighter side of their nature.

The government appears to think that some service industries are especially creative and therefore worthy of special help, including film, tourism and computer games, but also health care and conferences. This special pleading is arbitrary. Any industry can benefit from creative twists on old products or processes. Samsung’s phones often show more imagination than South Korean pop songs (see article).

The fortunes of the creative economy are not entirely divorced from the ticklishchaebol question. According to Mr Cochran, the chaebol stifle innovation. They wait for an innovative firm to prove itself, then offer to buy it for a measly sum. If the entrepreneur refuses, they threaten to drive him out of business.

The changes in commercial law passed just before Ms Park took office have somewhat narrowed the scope for abuse. Chaebol often take small stakes in firms that incubate a risky new technology. When the technology begins to mature, thechaebol increases its stake. In the past it has done so at the expense of the subsidiary’s other shareholders. Those shareholders can now hold directors liable if they sell too cheaply.

But some innovative firms have learned to prosper alongside the chaebol. A good example is Vinyl, a hip branding and technology company with about 200 employees, most of them under 40, some of whom wear shorts and decorate their desk with Iron Man action figures. Perhaps its greatest aspiration is that one day people will stop asking why it is called Vinyl. Its signature product is “Translook”, a transparent liquid-crystal display that can serve both as a window for displaying products and as a video screen for advertising them. Convenience stores can install it on the doors of their drinks refrigerators. When a customer approaches, the glass door swirls into life, showing fizzy Coca-Cola being poured into a glass.

One of South Korea’s big electronics companies wanted to buy Vinyl’s “Translook” brand but Vinyl refused, well aware that the bidder’s mass-produced displays were not as good as their own. For a big firm it was not worth making high-quality displays in small quantities, whereas Vinyl could make small batches of top-notch displays to serve a niche market. It concluded that if it sold its “baby” the big firm would ruin the brand, and if it did not sell it could withstand the competition. “They bought our machines several times,” says Gil Kim of Vinyl. “They will improve their version. But we are not afraid. We keep moving.”

The creative use of technology is also proving more effective in democratising Korean capitalism than its politicians have been. Thanks to the internet and mobile phones, small digital companies can now bypass the chaebol’s distribution networks. And when the chaebol take on software companies they do not always win. South Korea’s most successful messaging service is run by an independent firm called KakaoTalk. Many chaebol have released competing services, but none of them could keep up with the scrappy newcomer.

Fail better

In South Korea the biggest obstacle to a more creative economy may be the fear of failure. Creativity in any field requires experimentation, and experimentation necessarily entails mistakes. Unfortunately South Korean society is intolerant of failure, and South Korean finance especially so. It is “impossible” to come back from bankruptcy, says Mr Choi Bok-hee of the Korea Federation of Small and Medium Business. Banks typically hold small businessmen personally responsible for their loans and often require further guarantees as well. If the business fails, the default can spread from the firm to the owner, his family and friends. Banks will not back them again and society will judge them as “losers”, says Mr Choi. Jimmy Kim, the co-founder of Sparklabs, which helps start-up companies, goes further: “You are listed as a criminal if you do not pay back the loan.”

The government is trying to ease this fear of failure. Last year it mostly stopped banks from asking for these guarantees. Mr Kim is delighted: “We always thought the personal guarantees would stay for ever.” But what is still lacking in South Korea, he says, is early “take-off” financing up to the $5m range. Banks are not willing to take that kind of risk. But South Korea is now blessed with a cohort of successful home-grown digital entrepreneurs who are willing to invest capital, know-how and connections in the next generation. Mr Kim attributes this to the South Koreans’ notion of jeong, the strong sense of social obligation that they feel towards members of their circle.

Something similar has prompted the country’s banks to set up a fund for start-ups known as Dream Bank, which will raise 500 billion won by 2015. The government has also urged them to accept a wider range of collateral. Meanwhile it has cut red tape for repeat entrepreneurs. Like South Korea’s K-pop bands, famous for their frequent “comebacks”, entrepreneurs should be able to bounce back from business failure. That might encourage South Koreans to entertain more varied dreams of success.