Silicon Valley: Feel the Froth: Tech Valuations Stir Memories of 1999, but There Are Some Differences

October 28, 2013 Leave a comment

Silicon Valley: Feel the Froth: Tech Valuations Stir Memories of 1999, but There Are Some Differences

ROLFE WINKLER and MATT JARZEMSKY

Updated Oct. 27, 2013 7:56 p.m. ET

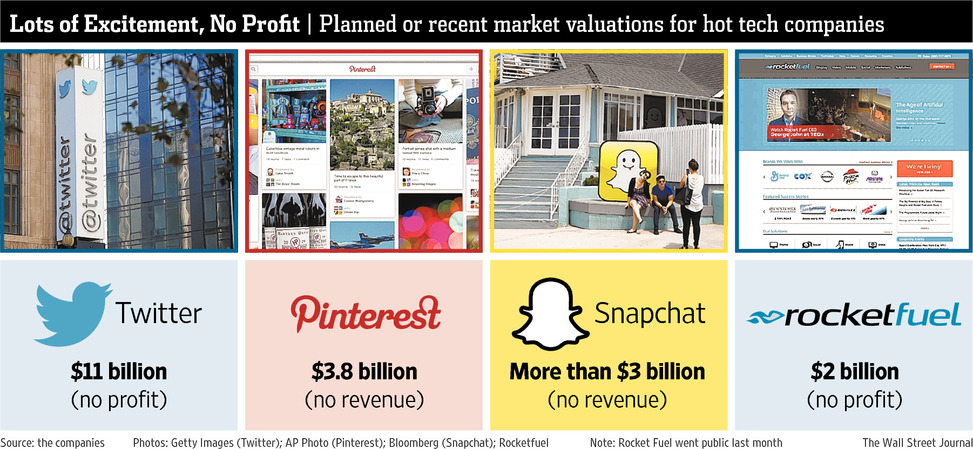

Twitter Inc. plans to go public at a value of $11 billion, without turning a profit. Venture capitalists just valued Pinterest Inc., which generates no revenue, at nearly $4 billion, and an even younger, revenue-deprived company, Snapchat Inc., is angling for a similar price tag. It isn’t quite 1999, when dot-com companies with scant revenue made initial public offerings and tripled in price on their first days of trading. When that bubble popped in 2000, scores of companies went bust, and millions of small investors suffered losses.Now, shares of Internet companies are soaring again, and signs of pre-2000 exuberance can be seen in Silicon Valley and the nearby area. Home prices in San Francisco and surrounding counties rose more than 15% in the past year. Office rents in San Francisco are 23% above their 2008 peak.

“It’s gotten pretty frothy,” says Daniel Cole, a senior portfolio manager at Manulife Asset Management who has invested in highflying IPOs, including for Rocket Fuel Inc.FUEL +1.93% The Redwood City, Calif., online-advertising company sold shares to the public last month at $29 each. They traded at $61.72 a share Friday, giving Rocket Fuel a market valuation of $2 billion, without having recorded a profit.

Technology and finance veterans say this time is different—and it is. Companies going public are more mature, the leadership teams more seasoned, the business models more proven. Social networks such as Twitter and Pinterest are drafting off the success of Facebook Inc., FB -0.94%which sports a market value of $126.5 billion, or about 70 times next year’s expected earnings.

But the current surge is accelerating, aided by some little-appreciated factors. Big companies are scarcely growing, and interest rates remain near zero, boosting zeal for investment opportunities in companies with high-growth potential. Moreover, a federal law enacted last year will allow startups to raise money from smaller investors, opening a vast new pool of potential funding.

“People are reaching for growth,” says Kenneth Turek, who manages the $850 million Neuberger Berman Mid-Cap Growth Fund, and has passed on this year’s tech IPOs.

Even some executives benefiting from the rally question its underpinnings. Tesla MotorsInc. TSLA -2.02% Chief Executive Elon Musk on Thursday said the electric-car maker’s stock price, which has quintupled this year, “is more than we have any right to deserve.” Tesla, which has reported one profitable quarter since going public in 2010, is valued at $20.6 billion, seven times its expected 2014 sales, according to S&P Capital IQ.

Netflix Inc. NFLX -0.96% Chief ExecutiveReed Hastings this month told investors in a letter that the video service’s stock was benefiting from “euphoria” driven by “momentum” investors. Netflix shares have tripled this year.

By most measures, today’s tech-stock mania falls well short of the dot-com era. Many of the companies going public have substantial revenue. When Pets.com Inc. completed an IPO in early 2000, it had recorded lifetime sales of about $6 million. Less than 11 months later, the company had dissolved.

This year, shares of newly public technology companies are being valued at 5.6 times sales, estimates University of Florida professor Jay Ritter, who tracks IPOs. That is well short of the median of 26.5 times sales in 1999. Shares of this year’s tech IPOs have risen an average of 26% on their first day of trading. In 1999 the average was 87%.

The average tech company to go public this year is 13 years old, compared with four years old for the IPO class in 1999. Tech’s presence in the IPO universe has receded, too. One-fourth of this year’s IPOs have been for tech firms, Mr. Ritter’s data show. In 1999, more than three-fourths were in the tech sector.

“The big difference now, is companies like LinkedIn, Twitter, Facebook have demonstrated an ability to generate sales, and with the exception of Twitter, profits,” Mr. Ritter says. In the dot-com days, “there were all sorts of companies going public that were essentially startups.”

But investor enthusiasm is filtering down to younger, less-proven companies today, too. Pinterest, an electronic-scrapbook service that began testing ads this month, said Wednesday that it had raised $225 million from venture-capital firms. Pinterest didn’t need the money; the company said it hadn’t spent any of the $200 million it raised in February when it was valued at $2.5 billion.

The new investment values the three-year-old company at $3.8 billion, a 52% jump in eight months.

Snapchat, a two-year-old mobile-messaging service popular with teens, is considering raising up to $200 million at a valuation exceeding $3 billion, people briefed on the matter said Friday. That would be more than triple the valuation that venture firms placed on Snapchat in June, when it raised $60 million.

Backers like these revenue-deficient companies for their potential.

Pinterest has 43 million active users in the U.S., according to market-researcher comScore, many of whom are looking for items to buy. Snapchat is just now sketching the outline of its business model.

Dozens of other startups are also in the pipeline, hoping to capitalize on the investor fervor.

“As entrepreneurs, we’ve seen that when the sun is shining, make hay,” says Kevin Hartz, chief executive and co-founder of online-ticketing startup Eventbrite Inc. “For a number of years the capital markets were suppressed, and now they’re opening up.” Eventbrite raised $60 million privately in April, valuing the company at roughly $600 million to $700 million, people familiar with the company said at the time.

One reason why they have opened up is the minimal interest rates on low-risk investments orchestrated by the Federal Reserve, which are prodding investors to place dicier bets in search of bigger returns.

That suggests that the tech surge is vulnerable to higher rates, says Jonathan Tepper, chief executive of research firm Variant Perception. The tech-heavy Nasdaq Composite Index fell 5% in a week after Fed Chairman Ben Bernanke in June indicated that the central bank might reduce bond purchases, which would likely push rates higher. When the Fed started raising interest rates in late 1999, the Nasdaq bubble popped the following March.

Another factor: Last year’s Jumpstart Our Business Startups Act soon will make it easier for less-wealthy individual investors to back startups. Already, the law has made it easier for financiers to pool money from individuals.

Some people worry that the looser rules may end up hurting small investors. Lynn Turner, a former chief accountant for the Securities and Exchange Commission, says the most-successful venture capitalists back winners only about 20% of the time.

As less-sophisticated investors jump into backing embryonic companies, “the odds aren’t in those people’s favor,” he says. A lot of those companies will fail, “then all of a sudden all you have is a piece of paper to stick on the wall.”