Rate revolution forces advisers to be bond kings; After Gross and Gundlach, the deluge: It’s no longer a set-it-and-forget-it core world

November 8, 2013 Leave a comment

Rate revolution forces advisers to be bond kings

After Gross and Gundlach, the deluge: It’s no longer a set-it-and-forget-it core world

Nov 7, 2013 @ 1:12 pm (Updated 3:51 pm) EST

Financial advisers got their first real taste of a rising interest rate environment in the second quarter and it’s led to a complete upheaval of the fixed-income landscape. The days of simply handing over a client’s fixed-income assets to a core fund, even those run by bond kings Bill Gross and Jeffrey Gundlach, seem to be over as the threat of further interest rate rises forces advisers to take the crown and rule over their own bond portfolios.“Going forward, you’re going to have to look at fixed income fundamentally different. We’ve had sort of a benign neglect in the past,” said Mike Ryan, chief investment strategist at UBS Wealth Management Americas. “We’re going to have to devote as much time and energy to managing the bond side of a portfolio as we do the on the equity side.”

Core bond funds had grown to more than $1 trillion in assets by the start of the year, led by heavyweights like the $247 billionPimco Total Return Fund (PTTAX) and the $34 billion DoubleLine Total Return Fund (DBLTX). It’s not hard to see why. With interest rates falling for 30 years, they were pretty much all an adviser needed to get by.

“It was easy, it worked well, and you didn’t have to think about it,” said Kathy Jones, a fixed-income strategist at The Charles Schwab Corp. “What investors didn’t realize was, it’s not terribly diversified.”

As advisers learned during the second quarter, when the 10-year Treasury jumped from its sleepy lows of around 1.65% to close to 3%, core bond funds come chock full of interest rate risk.

The Barclays Capital U.S. Aggregate Bond Index, the most popular bond benchmark in the world, fell more than 3% during the interest rate rally. That’s worse than how the index performed during the so-called “bond bloodbath” of 1994.

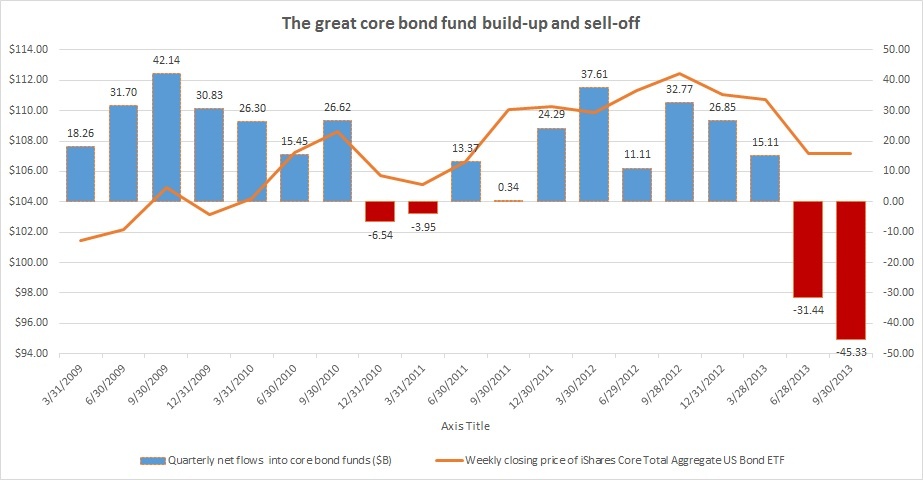

Bonds are supposed to be the boring and safe side of a portfolio, so it’s no surprise that those losses led to a mass exodus from core bond funds. In the third quarter alone,investors pulled out $45 billion from core bond funds, according to Morningstar Inc.

Interest rates have come back down from flirting with 3%, so the bond market has been able to regain some of those second-quarter losses, but advisers are still faced with a dilemma since interest rates are likely to go up again but returns are not at a high-enough level to provide meaningful income.

The core bond fund build-up and sell-off

“Core bonds used to generate 5 to 7% [of income] every year with no downside risk,” said Scott Williams, a partner at registered investment adviser Sanford Financial Services. “Now it’s 2% a year, with lots of downside risk.”

Mr. Williams has taken advantage of the lull in interest rates to move his clients out of core bond funds.

“Now is a second chance to get out of some of this stuff at decent prices, so we’re trying to take advantage of that,” he said.

Mr. Williams is significantly reducing core bond positions in favor of a barbell approach that focuses on short-term debt, to preserve capital, and nontraditional bond funds, to generate income and returns.

“That’s how we’re actually trying to make money in bonds,” he said.

He’s not alone in looking to nontraditional bond funds, which give managers the leeway to invest across all areas of fixed-income — and even short.

The top-selling bond fund in the third quarter was the $11.4 billion Goldman Sachs Strategic Income Fund (GSZAX), which had $4.1 billion of net inflows, according to Morningstar. It had had a 4.5% return year-to-date through Nov. 6, nearly 600 basis points better than the average core bond fund, which lost 0.97%.

The $23 billion JPMorgan Strategic Income Fund (JSOAX) came in second with $4.1 billion of inflows. The $9.6 billion BlackRock Strategic Income Opportunities Fund (BASIX) had $2 billion and the $3.8 billion BlackRock Global Long/Short Credit Fund (BGCAX) had $1.2 billion.

Not everyone is getting on board with such funds, though.

“We’re not believers in anything unconstrained,” said Josh Brown, chief executive of Ritholtz Wealth Management. “There’s too much room for manager error. We don’t feel comfortable that most bond managers really have the ability to time interest rates.”

Mr. Brown is sticking with Mr. Gundlach’s flagship DoubleLine Total Return Fund, which held up better than nearly every other intermediate-term bond fund in the second quarter because 16% of the fund’s assets were in cash.

But he said the low-interest-rate environment is forcing him to look at other assets, like emerging-markets debt, to pick up income.

Another possible downside to the new fixed-income landscape is that a lot of bond asset classes outside of the core are very credit sensitive and if there’s a jolt to the economy, they’re likely to decline further than the aggregate.

“It works until it doesn’t work,” Ms. Jones said. “We’re seeing the first signs of declining credit quality. It can take a while to play out but you don’t want to be on that trajectory when the whole thing changes on you.”

For risk-adverse advisers, Ms. Jones recommends doing a laddered portfolio of high-quality bonds.

“You’ll still see bond prices go down, but you’ll have the flexibility to reinvest if rates go up,” she said.