Tumbling US oil price transforms trading

November 8, 2013 Leave a comment

November 6, 2013 8:50 am

Tumbling US oil price transforms trading

By Ajay Makan in London

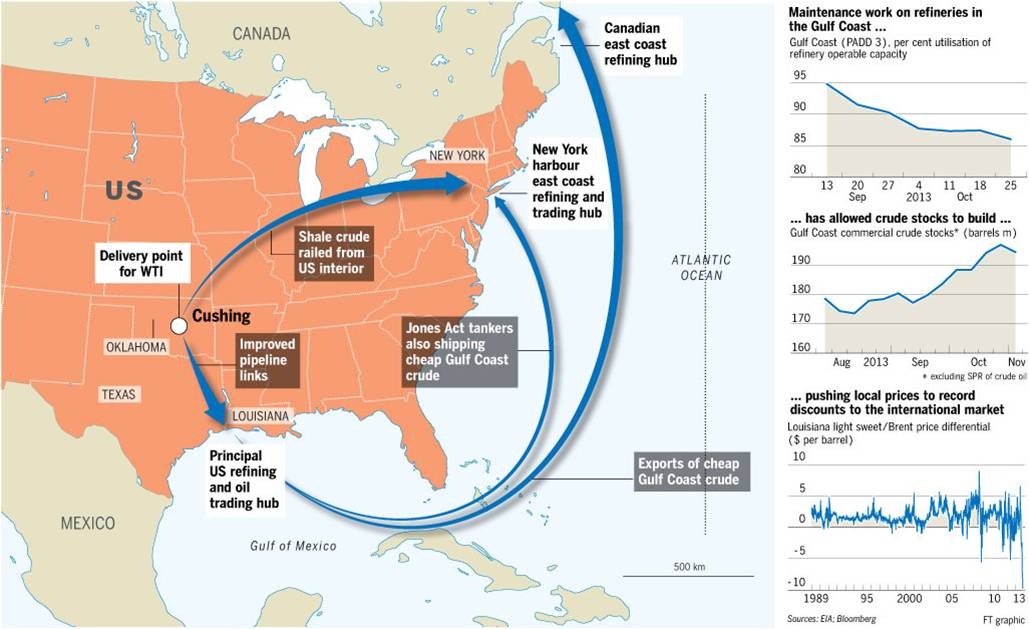

It is a taste of things to come. As the benchmark US oil price has slumped over the past month, so has the cost of crude in the Gulf of Mexico, one of the largest refining hubs in the world. The sharp price moves are testament to the impact of the US shale revolution, which has sent new supplies of crude from oilfields in North Dakota and Texas to the coasts of the US – with far-reaching effects on international oil markets.The low prices in the Gulf of Mexico are dramatically altering the incentives to move crude around North America and into the US. And as new trading patterns emerge, they invite scrutiny of one of their underlying causes – the effective ban on the export of crude oil from the US to countries other than Canada.

“The entire US crude market is disconnecting from global prices because it is increasingly easy to move oil around the country, but impossible to get it out,” says David Wech, an analyst at JBC Energy in Vienna.

At face value the latest divergence between US crude and global prices is relatively mild. As the US benchmark West Texas Intermediate has fallen towards $90 a barrel, its discount to the global marker Brent has reached $13.60 per barrel, still little more than half the level of a year ago.

But unlike in previous bouts of WTI weakness, when the Gulf of Mexico market remained stubbornly linked to global prices, this time coastal prices have fallen too, in part as better transport links have allowed more inland crude to flow to the coast.

In recent weeks Gulf blends from the shale-like Louisiana Light Sweet to the lower quality Mars have traded at record discounts to Brent of more than $10 per barrel, as crude stocks in the region have soared.

Since the start of October, LLS and Mars have both fallen by 10 per cent to lows of $95.95 and $91.25 per barrel respectively, while Brent has fallen by just 2 per cent to a low $105.19 per barrel.

In an open market such low prices for crude at one of the world’s major trading hubs would quickly attract buyers. But given the de facto ban on crude exports, they have instead encouraged an array of new trading patterns.

Traders say huge volumes of cheap Gulf of Mexico crude oil are now being shipped from the Gulf Coast to eastern Canada. One large trader of US oil expects eight Panamax tankers to ply the route in November and December, pushing US exports to 160,000 b/d, their highest level in more than a decade. Another expects exports to top 200,000 b/d in the last two months of the year.

“High stocks mean there is pressure to move US crude anywhere it can go, and Canada is the only destination,” says one trader. “This is a very obvious trading play which is wide open with logistics as they stand.”

Gulf Coast prices are distressed, so if you have crude at a switching point in North Dakota, you rail it east or west, anywhere but the Gulf

– Jan Stuart, head of energy commodities research at Credit Suisse

Shipments from the Gulf Coast to refineries around New York and Philadelphia are also increasing, say traders, although less markedly because of the Jones Act, a 1920 law, which requires more expensive US-flagged vessels be used for travel between domestic ports.

Low prices in the Gulf of Mexico also mean that shale oilfrom the interior needs to find alternative destinations. The discount of WTI to Brent makes it economic to transport crude by rail to refiners on the east coast of the US, which would otherwise have to use imported crude priced against the global benchmark.

At least half a million barrels a day are being transported by rail according to traders – a large increase compared with the summer when the discount of WTI to Brent had narrowed sharply – even though the practice is under scrutiny following a serious accident in the Quebec town of Lac-Mégantic in July.

“Gulf Coast prices are distressed, so if you have crude at a switching point in North Dakota, you rail it east or west, anywhere but the Gulf,” says Jan Stuart, head of energy commodities research at Credit Suisse.

However, with the US being such a big market for overseas producers, low Gulf of Mexico prices are also starting to have an impact much further afield.

They are reducing revenues for Middle Eastern and Latin American exporters, who sell crude to the US at prices linked to Gulf Coast markers. Saudi, Iraqi and Kuwaiti exports to the US, for example, are priced against the Argus Sour Crude Index, which fell by almost $7 per barrel in October.

Traders say that Middle Eastern exporters are missing out on several dollars in revenue for each barrel of oil shipped to the US instead of Asia.

Many analysts, however, do not expect the low prices in the Gulf to persist. As refineries return from maintenance and demand more crude they expect prices to quickly converge with Brent.

But others say that discounts will last, as refiners have an incentive to run down existing inventories before the end of the year, when many counties in Texas and Louisiana levy a tax on stocks held by refineries.

A chorus of voices from the International Energy Agency to energy industry executives and prominent former US government officials have already called on the US to dismantle the complex licensing system that strangles exports. If discounts persist at the Gulf Coast, more voices are likely to be added.