China Keeps Plan Decisively Vague; Beijing Delivers a Squishy Reform Agenda After a Big Communist Party Meeting, With Promises for More Details Down the Road

November 13, 2013 Leave a comment

China Keeps Plan Decisively Vague

Beijing Delivers a Squishy Reform Agenda After a Big Communist Party Meeting, With Promises for More Details Down the Road

AARON BACK

Updated Nov. 12, 2013 7:24 p.m. ET

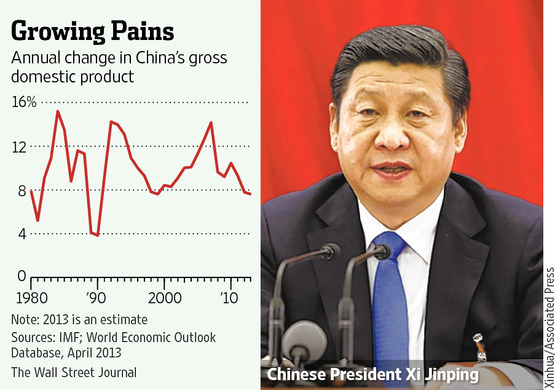

The Chinese Communist Party’s secretive meeting has come and gone, but President Xi Jinping‘s economic agenda remains a mystery. Ever since Mr. Xi became China’s top leader last year, investors and business executives have been told to wait until this fall’s so-called Third Plenum to get an idea of what his economic policies will be. Yet the statement that followed the conclusion of this meeting Tuesday didn’t clear the air. Granted, there was one reassuring message that stood out in a verbose communiqué following the conclave: Market forces will play “the decisive role” in allocating resources.At an earlier plenum in 1993, which laid the foundation for a critical wave of reforms to state-owned enterprises, the party merely pledged to allow the market to play a “basic role.” This year’s language is stronger, signaling Mr. Xi’s pro-market leanings.

But how, exactly, is the market’s role to be elevated? There is little indication. The party made encouraging promises to improve farmers’ land rights and to rationalize the government’s dysfunctional tax and budget systems. Previous party meetings have made similar promises with little follow-through.

Reform advocates, inside and outside the government, have a wish-list of measures to roll back the state’s economic power. Lifting controls that suppress deposit rates at banks would end an implicit subsidy for state-owned banks and the state-owned companies that borrow from them at the expense of China’s prodigious household savers. Opening up cross-border capital flows would further undermine the state’s control over the financial system.

Few expected clear promises to emerge from the plenum, but many hoped to see indications that the groundwork is being laid. Instead, the subject of financial reforms was avoided entirely. The closest thing was a brief paragraph that gave lip service to economic globalization and said that “restrictions will be relaxed on investment access.”

A fuller policy document is promised in coming days, and a special committee will be formed to oversee implementation. It is yet to be seen if the committee will be a sideshow or an entity empowered to cut through political rivalries. But the vague wording of the communiqué suggests the political will is lacking for the toughest decisions.

Some investors may interpret any such lack of resolve as positive news for China’s state-owned industrial complex. It suggests that government-controlled companies will continue to enjoy preferential access to capital at below-market rates. Besides big banks such asIndustrial & Commercial Bank of China 601398.SH -0.26% and China Construction Bank,601939.SH -0.69% other clear beneficiaries would include the Big Three state oil companies and other capital-intensive giants.

Long term, a failure to forge consensus on reforms would be bad news for China’s growth prospects. Debt levels will continue to rise, driven by excessive and inefficient investment by the state sector.

The Third Plenum was never going to deliver a perfectly laid plan for reform. Even so, the muddled outcome means big questions surrounding the direction of the world’s second-largest economy remain unanswered.

China Made Decisions About Market Reforms. We Think.

The meeting of China’s leaders that just wrapped up in Beijing was possibly the most important economic-planning session the world has seen in years. Or perhaps it wasn’t. This being China, it’s hard to say.

By now, China’s leaders understand the reforms the economy needs, and they presumably spent the past few days discussing them — but you’d hardly know it from the leaden communique issued after the gathering.

Traditionally, after each handover of power, the third full meeting of the Chinese Communist Party’s central committee is a big deal. Before this latest Third Plenum, the government was letting it be known that the session would stand in comparison with the one in 1978 that’s widely — if misleadingly — credited with introducing China’s program of market-oriented reforms and delivering more than three decades of astonishing economic growth.

As usual, though, the statement released after the meeting left analysts struggling to uncover meaning in commitments that could turn out to mean nothing. China will henceforth give markets a “decisive” role, the committee said — albeit in a system in which the state will still be “dominant.” To some commentators, that signaled an acceleration of pro-market reform; to others, a stalling. Another approach was to count the number of times the words “reform” and “socialism” appeared in the statement. (Respectively, 59 times and 28 times: Draw your own conclusion.)

The leadership’s inability to speak plainly to the country about its plans shows how far China’s system still has to travel before it achieves anything resembling political legitimacy: In this regard, in fact, the ruling elite has lately been moving backward — for instance, by tightening its repression of dissident voices. On the other hand, invoking China’s pro-market revolution of the late 1970s hardly signals complacency, let alone a desire to turn back the clock.

President Xi Jinping and his comrades plainly understand that China’s growth will fade and resistance to their leadership will increase unless corruption is curbed and the economy is rebalanced away from unprofitable state-directed investment and toward higher consumption and faster improvement of living standards. A growing role for market forces would achieve these shifts — but it would also undermine the power and privileges of the elite and risk short-term economic disruption.

Beijing is aware. A recent report co-written by the World Bank and China’s state-sponsored Development Research Center channeled advice that might have come from any champion of market capitalism. It called on the government to “implement structural reforms to strengthen the foundations for a market-based economy by redefining the role of government; reforming and restructuring state enterprises and banks; promoting competition; and deepening reforms in the land, labor and financial markets.” Yet China’s leaders have conservative instincts. They seek stability first. It’s a matter of (their own) survival.

It’s quite a dilemma. The government needs rapid growth to contain what would otherwise be increasing discontent; however, rapid growth, by its very nature, is politically destabilizing. The compromise lately has been cautious, sometimes grudging economic reform.

Over the coming weeks and months, as specific policies are announced, the intended pace of the next phase of political and economic reform will become clearer. For the country’s sake, there’s little question that faster would be best. For the sake of the country’s current leaders, that isn’t so obvious.

To contact the Bloomberg View editorial board: view@bloomberg.net.