Investors See End to Bond Rally; Americans Are Highly Exposed to Fixed Income

November 20, 2013 Leave a comment

Investors See End to Bond Rally

Americans Are Highly Exposed to Fixed Income

E.S. BROWNING

Updated Nov. 17, 2013 10:40 p.m. ET

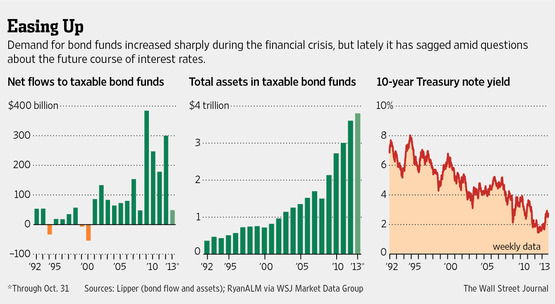

Smart analysts have been warning for years that the bottom could fall out of the surging bond market. They were wrong. Bond yields went to unprecedented lows, pushing bond prices to unprecedented highs and they just kept going. The weak economy, tiny inflation and exceptional Federal Reserve policies took bonds to unnatural levels.But nothing lasts forever. At some point, the economy will become more normal and yields will rise to more natural levels. Existing bonds with their lower yields will fall in value. Bond-fund investors will lose money.

Many bond-fund managers think the process has finally begun. The yield of the 10-year Treasury note has risen to 2.7% from about 1.6% in early May. Treasury-bond funds have fallen in value. Money managers have begun selling funds holding Treasurys and other high-grade bonds.

The spark for this is the Fed’s plan to start trimming its $85 billion in monthly bond-buying stimulus, which analysts expect to begin between December and June.

What no one knows is how fast the Fed will proceed, how fast yields will rise and how bad it will get for bonds. Some investors think the Fed will manage to hold Treasury yields down, limiting the damage. Others say longer-term Treasury yields could rise almost another percentage point by late 2014, sending bond prices lower.

U.S. taxable-bond funds today hold $3.8 trillion, up from $720 billion in 2000, according to data from Lipper. Americans are far more exposed to bonds than they ever have been. Many chose bond funds for safety, not realizing they can decline in value.

“Investors could be in for a rude awakening” if bond prices fall farther, said Barry Fennell, a senior Lipper research analyst who tracks fund flows.

Most bond experts, including Mr. Fennell, think the reaction to a Fed move will be less violent than last summer. But since the Fed stimulus program has never before existed and never before been withdrawn, no one knows.

“This is something we haven’t been through before,” said Steve Huber, a bond-fund manager at T. Rowe Price Group Inc. TROW +0.55% in Baltimore, which oversees $647 billion, including $153 billion in bond and money-market funds.

With job creation improving, the mortgage market strengthening and the Washington debt-ceiling dispute quieted, bond-fund managers expect the Fed to cut stimulus soon.

“We do think the Fed will reduce the size of its asset purchases in the next three or four months. December is possible and January into March is more likely,” said Rick Rieder, the leading bond-fund manager at BlackRock Inc., BLK +0.81% which manages $4.1 trillion, including $640 billion in bond portfolios Mr. Rieder oversees.

“I expect it will be some time in the first quarter of 2014,” said Ken Volpert, who heads the taxable-bond group at Vanguard Group Inc., which oversees $2.4 trillion, including nearly $750 billion in bond and money-market funds. Taxable bonds are everything except tax-free municipals, which march to a different drummer.

The men expect less excitement than in the summer. They think the 10-year Treasury yield could move up to about 3.2% or 3.25% in the first part of next year, less than half the summer jump.

Because inflation and economic growth are low, said Mr. Huber of T. Rowe Price, “rates won’t return to normal levels, 4% to 5%, for years.”

Still, a move like that would knock about 1.75% off of the value of a long-term Treasury-bond fund over six months, Mr. Rieder figures.

BlackRock is urging clients to shift to “unconstrained” bond funds, also called “go-anywhere” funds.

These can sell Treasury bonds and diversify and hedge using a wide range of global bonds that their managers think will do better.

These actively managed funds have much higher fees than index funds and rely at least partly on the manager’s ability to pick the right bonds.

Mr. Volpert of Vanguard is urging the opposite: Buy more broad-based funds if prices decline. In a portfolio of 60% stocks and 40% bonds, if bonds decline to 34% of the holding, investors would rebalance by buying the now-cheaper bonds and returning them to 40%. The goal would be to buy assets at reduced prices and hold down fees.

Mr. Huber has a third approach. He considers bonds world-wide fully priced or even overpriced. He is keeping more money than usual in very short-term bonds.

If bonds overreact globally after the Fed starts cutting stimulus, he plans to shift money to beaten-down bargains, notably in the developing world. Of course, it is hard to know when to buy in a volatile global market, especially for ordinary investors. Mr. Huber suggests they might look for bargains in U.S. corporate bonds.

There is also is the risk that bonds could fall more than many experts expect.

J.P. Morgan JPM +1.97% Chase & Co., for example, forecasts that 10-year Treasury yields could hit 3.65% in 2014, sending bond prices sharply lower and hurting people who had purchased bond funds in a search for safety.

More-optimistic fund managers think the Fed would prevent that, by slowing down or postponing stimulus cuts if markets panic.

“The Fed will indicate that if the market reacts, they will slow” the cutbacks, said Mr. Volpert.

Then there is the opposite possibility: that the economy could prove softer than expected, or another crisis could hit Washington. In that case, investors could buy more bonds in a flight to safety, driving bond prices higher and confounding the experts again.

John Herrmann, director of U.S. interest-rate strategy at Mitsubishi UFJ Securities (USA) in New York, thinks Janet Yellen, slated to become Federal Reserve chairman next year, could delay cutting stimulus spending longer than most people expect. He thinks Ms. Yellen could conclude that, with inflation low and economic growth still sub-par, there is no rush.

“People may be surprised at how long it lasts,” Mr. Herrmann said.

If so, Treasury bonds—and the stock market—could do better next year than the experts think.