Devaluation stations: Et tu China?

February 1, 2014 Leave a comment

Devaluation stations: Et tu China?

| Jan 30 13:50 | 6 comments | Share

Part of the UP SHIBOR CREEK… SERIES

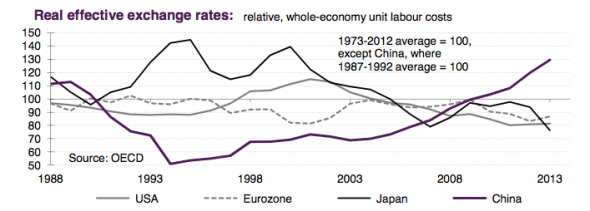

Lombard Street’s Charles Dumas charts the overvaluation of the Chinese currency:

As he notes, 2011 was the first year that evidence for an overvalued yuan began to emerge:

Since then China’s relative unit labour costs are up another 20%. Whatever the “right rate” may be in the above chart, it is indisputable that real appreciation of a massive 77% has occurred since China left its fixed, 8.28 yuan/dollar rate in 2005 in favour of a crawling peg. Of this about half is in the trade-weighted exchange rate, the other half being excessive wage-cost inflation.

The overvaluation according to Dumas has squeezed profit margins, inducing ongoing wage-cost inflation in the context of producer price deflation. When allowing for the producer price deflation, interest rates in real terms turn out to be a formidable 7.5-8 per cent, and more for those invested in the shadow banking system.

Small wonder there’s a 48 per cent investment rate in that context. Any move to reform the market and chances are the investment rate would crash, says Dumas, and with it the economy — hence ongoing government-mandated lending to entities that should probably not be borrowing, and the soaring debt ratio.

This is the difficulty that China faces with financial reform. As Dumas notes, any liberalisation would likely devalue the yuan and with it deposits:

As we have said before, with financial liberalisation of interest rates, banking and overseas capital movements, Chinese money would flee, bringing badly needed yuan devaluation and relieving many of the pressures described above. But that capital flight would drain cash from bank deposits, and force recapitalisation of the manifold bad loans that have been made.

Still, better this today than something worse tomorrow:

This is the “crisis now” scenario, painful but manageable. Without financial reform, the yuan will probably stay high, and the debt ratio could mount to crippling levels. At best, this will simply sap the economy and leave it moribund, like Japan post-1990 with a similar combination of excess debt but strong FX reserves. But at worst, a major debt crisis could cause the whole Chinese emergence to become open to doubt.

In short, ongoing overvaluation is forcing China’s debts up. And in Dumas opinion the PBOC/government should act now to allow for a managed devaluation than risk a greater crisis tomorrow.