What’s a chengyu for ‘subprime is contained’?

February 1, 2014 Leave a comment

What’s a chengyu for ‘subprime is contained’?

| Jan 28 13:18 | 14 comments | Share

There is a nice chengyu in the latest note from Bin Gao, BofAML’s China rates strategist: 居安思危, ‘be prepared’.

Oh yes, and the note also compares this week’s rescue of Credit Equals Gold No.1 to a Bear Stearns moment for China.

The last-minute deal saved a CNY3bn trust product which we expected a high probability of default. The deal will redeem investors’ principal, dollar for dollar, but it won’t pay the back coupon missed last year, amounting to 7.2% of principal. In that sense, this deal constitutes a debt work-out, a technical default, with investors suffering a small default loss.

Our economist expects this case and subsequent few to have little impact on China’s growth, forecasted to be 7.6% for 2014.

As a rate strategist, we are more interested in examining a set of scenarios, and what we see unsettles us.

We will be more specific: the bailout looks very much like the Bear Stearns moment.

The unspoken corollary being… the Chinese authorities might next face their own version of the Lehman choice: whether or not to bail out a much larger trust product, or a financial institution connected to it. The problem isn’t necessarily that growth iscertain to be blown off course, but that the tail risk is becoming more apparent.

Arguably, that would make higher money-market rates since June the equal of Libor in August 2007 (though we’d argue that the PBoC knows this and is trying to develop its own Fed-style collateral facilities).

Still, Bin Gao takes the analogy further:

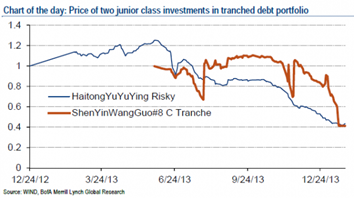

The evolution then follows with risky debt investments losing value fast. In the US, it started with subprime mortgage funds. In China, leveraged junior tranches of managed debt products are experiencing the same problem, due to a combination of higher rates and fear of worsening credit quality of the underlying names; a few have lost half of its value in the last six months. Cases in point: Haitong’s yueyueying risk-tranche and ShenYinWanGuo’s #8 tranche C have lost more than 60% from its recent peak…

It then goes with the failure of financial institutions. Just like we would never know what would have happened if Bear Stearns was not bailed out, we will never know what would have happened if China Credit Trust (CCT) had to foot the bill of CNY3bn to pay back trust investors. Although the company has CNY10bn net asset, CCT only has CNY3bn liquid assets with CNY1.35bn short-term liability; hence, it would find it difficult to pay the CNY3bn in full. The contagion effect could be quite strong. The company’s CNY10bn equity supported CNY271bn in trust assets as of 2012. At AUM/equity of 27 (as of 2012 and likely higher in 2013), the company actually has one of the lowest leverage ratios. The average AUM/equity of trusts companies is 43 to 1 by 3Q13 with the worst having their ratios rising up to the three-digit territory. In our view, it is only a matter of time before some of these institutions fail.

One counterargument to this is that Chinese coal mining has been a uniquely terrible business and a trust which featured these assets in size is a special case. BofAML’s objection to that view seems fair — financing of local government construction projects could also be hiding bad assets — but we’d note one curiosity.

Shaanxi Coal’s Shanghai IPO was up 25 per cent on its first day this week.

Someone’s mispricing something.