China Scrambling After “Discovering” Thousands Of Tons Of Rehypothecated Copper, Aluminum Missing

June 12, 2014 Leave a comment

China Scrambling After “Discovering” Thousands Of Tons Of Rehypothecated Copper, Aluminum Missing

Tyler Durden on 06/04/2014 09:22 -0400

“Banks are worried about their exposure,” warns one warehousing source, “there is a scramble for people to head down there at the minute and make sure that their metal that they think is covered by a warehouse receipt actually exists.”

The rehypothecated catastrophe that we discussed in great detail here (copper financing), here (all commodities), and here (global contagion) appears to be gathering speed as the China’s northeastern port of Qingdao has halted shipments of aluminum and copper due to an investigation by authorities after they found “there is a discrepancy in metal that should be there and metal that is actually there.”

Copper prices are tumbling already (despite Gartman’s most recent prognostication on Dr. Copper’s China recovery meme) as the world’s 7th largest port disallows any shipments until the probe is complete.

“It’s such a massive port I would think virtually everybody has exposure,” warned one analyst, adding that this will bebearish for metals as “a lot of Western banks will try to offload material and try not to deal with Chinese merchants.”

China’s northeastern port of Qingdao has halted shipments of aluminium and copper due to an investigation by authorities, causing concern among bankers and trade houses financing the metals, trading and warehousing sources said on Monday. Port authorities could not immediately be reached for comment. China has a public holiday on Monday.

“We were told we can’t ship any material out while they do this investigation,” a source at a trading house said. The port of Qingdao is China’s third-largest foreign trade port and the world’s seventh-largest port, trading with 700 ports in more than 180 countries, according to its website (www.qdport.com/).

“Banks are worried about their exposure,” one warehousing source in Singapore said.

“There is a scramble for people to head down there at the minute and make sure that their metal that they think is covered by a warehouse receipt actually exists,” he said.

Metal imports have been partly driven in China as a means to raise finance, where traders can pledge metal as collateral to obtain better terms. In some cases the same shipment can be pledged to more than one bank, fuelling hot money inflows and spurring a clampdown by Chinese authorities.

“It appears there is a discrepancy in metal that should be there and metal that is actually there,” said another source at a warehouse company with operations at the port.

“We hear the discrepancy is 80,000 tonnes of aluminium and 20,000 tonnes of copper, but we hear that the volumes will actually be higher. It’s either missing or it was never there – there have been triple issuing of documentation,” he said.

Beijing last year set new rules to curb currency speculation amid signs that hot money inflows helped push the yuan to a series of record highs. The rules required banks to tighten the management of their foreign exchange lending and types of clients that are able to access those loans.

“It’s such a massive port I would think virtually everybody has exposure,” the trading source said.

“Once the investigation is over, it could be bearish for metals. I think that a lot of Western banks will try to offload material and try not to deal with Chinese merchants,” the trading source added.

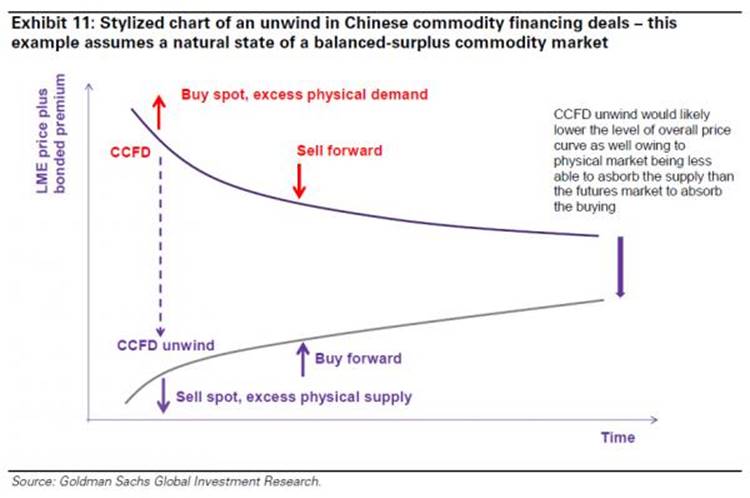

Critically – this is a major problem for any shadow-banking credit creation process as if the rehypothecated commodity-backed CCFDs are ultimately unwound, 1) someone will not get their collateral (payment problems – bailouts?), 2) less real collateral means less real credit expansion (which banks can;t fill because the firms that use this method of financing are anything but creditworthy), and 3) liquidation of any assets will proceed rapidly…

Goldman concludes that “an unwind of Chinese commodity financing deals would likely result in an increase in availability of physical inventory (physical selling), and an increase in futures buying (buying back the hedge) – thereby resulting in a lower physical price than futures price, as well as resulting in a lower overall price curve (or full carry).” In other words, it would send the price of the underlying commodity lower.

Finally, as we showed before when it comes to commodity financing deals, in terms of total notional value, both copper and aluminum pale by comparison to the one metal most used (by value) in China as a funding substitute: gold

As we commented previously:

When we previously contemplated what the end of funding deals (which the PBOC and the China Politburo seems rather set on) may mean for the price of other commodities, we agreed with Goldman that it would be certainly negative. And yet in the case of gold, it just may be that even if China were to dump its physical to some willing 3rd party buyer, its inevitable cover of futures “hedges”, i.e. buying gold in the paper market, may not only offset the physical selling, but send the price of gold back to levels seen at the end of 2012 when gold CCFDs really took off in earnest.

In other words, from a purely mechanistical standpoint, the unwind of China’s shadow banking system, while negative for all non-precious metals-based commodities, may be just the gift that all those patient gold (and silver) investors have been waiting for. This of course, excludes the impact of what the bursting of the Chinese credit bubble would do to faith in the globalized, debt-driven status quo. Add that into the picture, and into the future demand for gold, and suddenly things get really exciting.

So if tens of thousands of tons of copper and aluminum are suddenly “missing”, one can assuredly say: “at least the gold is still there.” Right?