Warehouse Collateral Fraud Vs Warehouse-System Business Moats in Asia to Store Value

June 26, 2014 Leave a comment

“Bamboo Innovators bend, not break, even in the most terrifying storm that would snap the mighty resisting oak tree. It survives, therefore it conquers.” |

| BAMBOO LETTER UPDATE | June 23, 2014 |

| Bamboo Innovator Insight (Issue 39)

The weekly insight is a mere teaser into the opportunities – and pitfalls! – in the Asian capital jungles. Get The Moat Report Asia – a monthly in-depth presentation report of around 30-40 pages covering the business model of the company, why it has a wide moat and why the moat may continue to widen, a special section on “Conversation with Management”, the context – why now (certain corporate or industry events or groundbreaking news), valuations (why it can compound 2-3x in the next 5 years), potential risks and how it is part of the systematic process in the Bamboo Innovator Index of 200+ companies out of 15,000+ in the Asia ex-Japan universe. |

|

Warehouse Collateral Fraud Vs Warehouse-System Business Moats in Asia to Store Value

“From saving comes having.” “If ye like the nut, crack it.” – Local Scottish proverbs, meaning nothing is achieved without effort.

A Scottish pelican flew by the Omaha of Singapore and Asia last week. Over coffee at the Singapore Management University away from the syndicates, two value investors – and one of our valued Moat Report Asia subscribers – from an illustrious Scottish-origin global fund house with investment offices from Botswana (arguably Africa’s best-managed nation) to Australia explained that their corporate symbol of pelican, characterized by their long beaks and large warehouse-like throat pouch, represents the prudent storage of value and wealth.

We exchanged our views on Asia, including how one Asian watch retailer, with attractive quantitative financial numbers and a “capex-light” business model with concessionary-fees paid to departmental store outlets, had a shareholder-syndicate that is responsible for quite a number of misgovernance-prone firms such as Asia Cassava(841 HK), Natural Beauty Bio-Tech (157 HK), LifeTech Scientific (1302 HK), China Distance Education (DL US) etc. Hidden related-party transactions have cast doubts on the quality of its receivables and other receivables used to prop up artificial sales. We also talked about briefly how we have both visited a prominent consumer brand in China – and that their neighbor on the same floor was a HK-listed green food processor, a market darling and “compounder” whose stock price had plunged over 90% coincidentally after our article was published in the local newspaper revealing its connections with a Singapore-listed company embroiled in accounting fraud – the chairmen of both companies are brothers.

The recent warehouse collateral rehypothecation fraud in China’s Qingdao port unravelled in early July was also of interest and relevance to understanding the governance risks in Asia. According to the 21st Century Business Herald, at least 17 financial institutions involved in copper, aluminum and other nonferrous metals financing business face losses of almost RMB15bn ($2.4bn) (not including the contagious rehypothecated collateral chains) in which the same stock of cooper stored at the port as collateral against loans was suspected to be illegally pledged by trading firms to more than one lender to obtain multiple loans. Qingdao Port ranks as China’s largest iron ore port and third-largest foreign trade port and the world’s seventh-largest port. Traders have used metals and commodities as collateral to bring into China around $160bn, about 31% of the China’s total short-term foreign exchange loans (duration < 1 year) and 14% of China’s total FX loans. Of these deals, gold, copper and iron ore are three leading commodities, followed by soybean, palm oil, natural rubber, nickel, zinc and aluminum. Some of this cheaper overseas money is used to speculate in “higher-yielding”, short-term investments in China via loans to local government financing vehicles (LGFVs) and property developers. Rather than being used to meet actual demand, these stocks are imported into bonded warehouse zones, areas where import taxes don’t apply, and re-exported when they are no longer needed as collateral. Such commodity finance loans to circumvent China’s capital controls allow traders to take advantage of the fact that interest rates in China are higher than on the offshore loans. The catalyst for the unravelling could be due to the sharp decline in profitability of such commodity financing due to lower RMB/USD rate differentials, higher RMB volatilities against USD and higher LME rolling costs. Since mid-2013, the Chinese government moved to reduce the amount of money that can be borrowed per commodity unit i.e. larger amounts of commodities are needed to raise the same amount of low cost foreign funding. The risks of the shadow banking sector and commodity financing are that no one knows who the ultimate borrower is, how indebted they are or how many people they owe. CITIC Resources (1205 HK), part of the powerful CITIC Group, had reported that half of its alumina stockpiles, worth $50m, at Qingdao port cannot be located after applying to courts in Qingdao to secure metal assets it owns in warehouses.

The trader at the heart of the fraud, Qingdao Decheng Resources, has a trading subsidiary office in Singapore’s financial hub called Zhong Jun Resources, headed by Chen Jihong, a Singapore mainland-Chinese citizen. Chen was detained by Chinese authorities in late April over the corruption probe related to Western Mining (601168 CH), a mining major in northwestern Qinghai province. Chen had shares in Qingdao Port (6198 HK) which went public in Hong Kong on June 6. Decheng’s parent, Dezheng Resources, bills itself as China’s lowest-cost aluminium producer, with smelters sited alongside power plants and open pit coal mines in Inner Mongolia and elsewhere. Many western banks were said to not realize they are involved in the Qingdao fraud. Citibank had made a loan to Swiss commodities trading firm Mercuria Energy Group that ended up sending money to China by way of the Qingdao port. Mercuria had agreed in March to buy the physical commodities business of JP Morgan Chase. Banks around the world lent $687bn to commodities-based businesses, according to Bloomberg. JPMorgan was the top U.S. lender worldwide, at $57bn, followed by Wells Fargo $47bn.

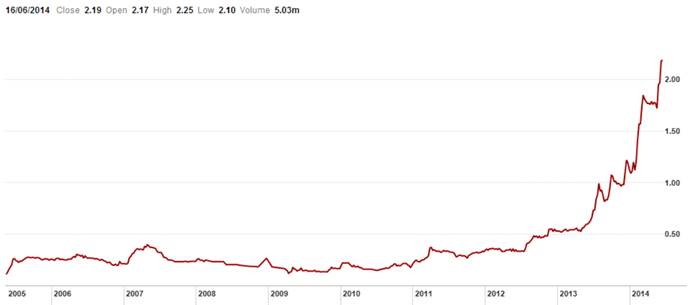

Interestingly, we have come to know about the Qingdao gang in Singapore around four years ago in 2010. A friend’s lady friend, a fresh graduate, was employed by the huge Qingdao firm at a relatively high monthly salary of US$6,000. The girl was spotted carrying expensive luxury branded bags and had boasted about how easy and comfortable her job was at this big company. The girl’s previous job in Singapore was at a Chinese “educational institute” and she was responsible for marketing the courses to overseas Chinese students – and getting lucrative commission for each successful case; the school folded. The Qingdao gang was one of the many entrepreneurs from China lured by the Singapore government to set up trading subsidiaries to build up the financial services sector and help its ambitions as the offshore centre for renminbi trade. They are in Singapore to seek cheaper US dollar loans for their commodity purchases on terms that are cheaper than dollar funding offered in China. Many of these commodity trading firms have no legally-enforceable assets in Singapore. Many businesses in Asia are simply “asset-shifters”… <Article snipped> The archetypal compounders Wal-Mart and Amazon have warehouse-system business moats to support their overall business model and strategy to compete to get closer to the end consumer with consumer intelligence and to deliver better service. The warehouses aren’t mere tangible assets for investment purposes but are embedded with intangible knowledge to win customers. For instance, Wal-Mart … <Article snipped> The case of Wal-Mart and Amazon illuminates the power of warehouse-system business moats in storing value for investors. How about the case of Asia? GD Express – Stock Price Performance, 2005-2014

We are reminded of one of our overseas due diligence exercises conducted in late March 2012 on several companies, including Malaysia’s GD Express (Bursa: GDX MK, MV $569m). Interestingly, after we saw the company which was at the cusp of a major expansion, share price compounded 7-folds to $569m in market value… <Article snipped> Asian Company X Vs Amazon – Stock Price Performance, 2009-2014

Asian Company X Vs Amazon – Stock Price Performance, 2011-2014

There is another Asian company with a warehouse-system business moat that we might highlight in our monthlyMoat Report Asia at the opportune time. This weekly insight is a mere teaser into the opportunities – and pitfalls! – in the Asian capital jungles beyond the “cheap” statistical stocks whose stock prices, volume and accounting numbers are often manipulated by syndicates and “insiders” (dubbed “Zhuang Jia” 庄家). The Moat Report, on the other hand, is a monthly in-depth presentation report of around 30-40 pages covering the business model of the company, why it has a wide moat and why the moat may continue to widen, a special section on “Conversation with Management”, the context – why now (certain corporate or industry events or groundbreaking news), valuations (why it can compound 2-3x in the next 5 years), potential risks and how it is part of the systematic process in the Bamboo Innovator Index of 200+ companies out of 15,000+ in the Asia ex-Japan universe. Above are the 5-year and 3-year price charts of the Asian company vs Amazon; its market value is between $500m-$1bn. The company has differentiated itself by providing… <Article snipped> Thus, like the good old Scottish values in the opening proverbs that nothing is achieved without effort, investing in physical tangible assets which are structured in the balance sheet for passive investment purposes might generate attractive short-term high-yielding returns effortlessly. However, these “effortless” arbitrage returns may not be sustainable and can unwind violently like the Qingdao fraud case. Seemingly long-term debt capital became short-term capital creating a duration mismatch between left-hand side arbitrage opportunities and right-hand side liabilities. Consequently, arbitrageurs became unable to maintain prices of assets. Most Asian entrepreneurs and business owners do not believe in “impractical” knowledge to build a wide-moat business, preferring opportunistic maneuvers in active asset-shifting and passive investments in property and warehouses for their yields and potential capital appreciation in an “effortless” way to make money. Thankfully, there are some low-profile resilient Asian innovators who see fit to crack the tough nut of knowledge in building a wide moat with a warehouse-system business model to reach out to their customers and serve them better. Instead of indulging in an ostentatious lifestyle with various forms of trophy assets, the quiet innovators save and reinvest the profits back into the business to widen the moat. Because the Bamboo Innovators know that building a wide moat is the only sustainable way to store value and wealth.

To read the exclusive article in full to find out more about the story of PT Davomas Abadi, APP, Golden Key, Astra, including the impact of hidden controlling ownership on governance risks and business valuation, please visit:

Some updates:

1) We will be away from July 1 to July 11 for our mandatory military camp training in Singapore, following which we will be on a business trip in Italy from July 13-20.

2) Value Unplugged 2014 and Value Investing Seminar in July in Italy

Value Unplugged 2014 (www.valueunplugged.com) in Naples, Italy is now full. We’ll gather in a small, relaxed setting to learn and make friends. We’ll also attend Ciccio Azzollini’s sold-out Value Investing Seminar in July in Trani, Italy — the definitive summer conference for value investors – as one of the keynote speakers. http://www.valueinvestingseminar.it/content_/relatori.asp?lan=eng&anno=2014

|

| The Moat Report Asia |

|

“In business, I look for economic castles protected by unbreachable ‘moats’.” – Warren Buffett

The Moat Report Asia is a research service focused exclusively on competitively advantaged, attractively priced public companies in Asia. Together with our European partners BeyondProxy and The Manual of Ideas, the idea-oriented acclaimed monthly research publication for institutional and private investors, we scour Asia to produceThe Moat Report Asia, a monthly in-depth presentation report highlighting an undervalued wide-moat business in Asia with an innovative and resilient business model to compound value in uncertain times. Our Members from North America, the Nordic, Europe, the Oceania and Asia include professional value investors with over $20 billion in asset under management in equities, secretive global hedge fund giants, and savvy private individual investors who are lifelong learners in the art of value investing.

Learn more about membership benefits here: http://www.moatreport.com/subscription/

https://www.moatreport.com/individual-subscription/?s2-ssl=yes

Our latest monthly issue for the month of June investigates the world’s #1 ODM (Original Design Manufacturer) and global #5 manufacturer of a consumer healthcare device product that is used frequently, even daily, thus providing the foundation for stable recurring cashflow. This company is also a hidden champion in a niche product segment (50-55% of group’s sales) that has become a high-growth fashion product currently accounting for less than 10% of the overall industry. The company is able to mass-manufacture this niche product, but not the giants, because of its unique process IP in flexible manufacturing system and know-how to handle large-scale complex orders. The manufacture of this product itself is difficult to replicate and requires FDA/CE licenses because of its medical device nature and the entry barrier is not capital but the know-how and R&D expertise. In particular, the manufacturing integrates different fields of science including polymer chemistry, physics, optics, engineering, materials control, process control, microbiology, and, injection molding. The firm has also developed a proprietary system of tracking the manufacturing process of different sets of product so that if a quality issue arose, when and where the problem set of products was being produced could be swiftly identified, thus diminishing the scale and cost of product recall. This system has helped the firm win the long-term trust of its ODM customers to place stable large orders. The Big Four giants do not have such a system and have to incur substantial losses from product recalls. The company also possess its own brand which has many loyal followers and support in its home market where it enjoys a 30% market share and contributes to 25% of group’s sales while sticky ODM customers account for 75% of group’s sales, mainly from the Japan market. As a result of its wide-moat advantages, the firm enjoys a consistently high ROE of 41%, double or triple that of the giants. From FY07 onwards, even during the depths of the Global Financial Crisis in 2007/09, the firm has not raised equity. Since listing in Mar 2004, the company has only done one rights issue in May 2005. Also, it is able to sustain a strong stable cash dividend payout (>70% with 3% yield) with its healthy net-cash balance sheet (net cash $30m; net cash-to-equity ratio 23%) and proven management execution in prudent capex expansion to support sustainable quality earnings growth. M&A deals in the healthcare and medical device sector has been growing due to their strong defensive nature and giants seeking growth to overcome their own patent cliff. The firm will always be an attractive takeover target by giants who wish to swallow it up to possess its valuable flexible manufacturing system and know-how to fill their own missing competency gap and hence will enjoy long-term downside protection in its terminal value. In the battle between “ODM vs Brand”, we find the story of the company to be quite similar to that of TSMC (2330 TT, MV $103bn), now the largest ODM foundry in the world. “Skate to where the puck is going to be, not where it has been,” as hockey legend Wayne Gretzky advised. In our view, the profit and valuation premium in the value chain will start to skate to the “Inno-facturers” who are the hidden ODM innovators (the brand behind brands) consolidating the industry, such as TSMC and this company. While its valuation is not cheap with EV/EBIT (FY13) at 20.6x, when we compare EV/EBIT relative to ROE, the company is relatively cheap, by as much as 130-220% when compared to giants and other comparables. When we compare EV/EBITDA relative to ROE, the valuation gap is 90-160%. This long-term valuation gap implies that the company, with its far superior and sustainable ROE, could potentially double to $2.4bn, as it continues to consolidate its niche product segment and enter into a new product cycle of an innovative product whose patents are expiring in 2014/15 (US/worldwide) to make ASP/margin improvements in sustaining quality profits and cashflow. Its share price has dropped 18% from its recent high and underperformed the index by 26% in the last six months. This will present a buying opportunity for long-term value investors who can penetrate beyond conventional valuation metrics because of a deep understanding of its business model and underlying source of its wide-moat advantages. In Asia, many firms break apart or become value traps due to shareholder conflict, envy and differences in opinion on the business direction of the company. The stable long-term corporate culture infused by the late founder, who established the company in 1986 with the current executive chairman and 2 other key shareholders, to combine the energy and ideas of everyone to work hard to keep the business running forever is underappreciated.

Our past monthly issues examine:

The Moat Report Asia Members’ Forum has been getting penetrating quality dialogues from our subscribers.Questions range from:

Do find out more in how you can benefit from authentic and candid on-the-ground insights that sell-side analysts and brokers, with their inherent conflict-of-interests, inevitable focus on conventional stock coverage and different clientele priorities, are unwilling or unable to share. Think of this as pressing the Bloomberg “Help Help” button to navigate the Asian capital jungle. Institutional subscribers also get access to the Bamboo Innovator Index of 200+ companies and Watchlist of 500+ companies in Asia and the Database has eliminated companies with a higher probability of accounting frauds and misgovernance as well as the alluring value traps.

|

| Professional Development Workshops for Executives and Lifelong Learners |

|

Our 8th run of the series of workshop From the Fund Management Jungles: Value Investing Exposed and Explored– (Part 1) Moat Analysis, (Part 2) Tipping Point Analysis and (Part 3) Detecting Accounting Fraud – on 14 June 2014 has been well-received with serious value investors, professionals, and serious lifelong learners attending, with some who flew in from Jakarta and KL!..

Our 9th workshop will be on Detecting Accounting Fraud Ahead of the Curve sometime later in the year.

Thank you for your support all this while!

|

|

Thank you so much for reading as always.

Warm regards, KB Kee

Managing Editor The Moat Report Asia Singapore Mobile: +65 9695 1860

A Service of BeyondProxy LLC 1608 S. Ashland Avenue #27878 Chicago, Illinois 60608-2013 Other offices: London, Singapore, Zurich

|

|

P.S.1 Here is a little more about my background: KB Kee has been rooted in the principles of value investing for over a decade as an analyst in Asian capital markets. He was head of research and fund manager at Aegis Portfolio Managers, a Singapore-based value investment firm. As a member of Aegis’ investment committee, he helped the firm’s Asia-focused equity funds significantly outperform the benchmark index. He was previously the portfolio manager for Asia-Pacific equities at Mirae Asset Global Investments, Korea’s largest mutual fund company. He holds a Masters in Finance and degrees in Accountancy and Business Management, summa cum laude, from Singapore Management University (SMU). KB had taught accounting at his alma mater in Singapore Management University and had also published an empirical research paper Why ‘Democracy’ and ‘Drifter’ Firms Can Have Abnormal Returns: The Joint Importance of Corporate Governance and Abnormal Accruals in Separating Winners from Losers in the Special Issue of Istanbul Stock Exchange 25th Year Anniversary Best Paper Competition, Boğaziçi Journal, Review of Social, Economic and Administrative Studies, Vol. 25(1): 3-55. KB has trained CEOs, entrepreneurs, CFOs, management executives in business strategy, macroeconomic and industry trends in Singapore, HK and China.

P.S.2 Why do I care so much about doing The Moat Report Asia for you? My personal motivation in embarking on this lifelong journey has been driven by disappointment from observing up close and personal the hard-earned assets of many investors, including friends and their families, burnt badly by the popular mantra: “Ride the Asian Growth Story!” I witnessed firsthand the emotional upheavals that they go through when they invest their hard-earned money – and their family’s – in these “Ride The Asian Growth Story” stocks either by themselves or through money managers, and these stocks turned out to be the subject of some exciting “theme” but which are inherently sick and prey to economic vicissitudes. They may seem to grow faster initially but the sustainable harvest of their returns is far too uncertain to be the focus of a wise program in investment. Worse still, the companies turned out to be involved in accounting frauds. Their financial numbers were “propped up” artificially to lure in funds from investors and the studiously-assessed asset value has already been “tunnelled out” or expropriated. And western-based fraud detection tools and techniques have not been adapted to the Asian context to avoid these traps.

After a decade-plus journey in the Asian capital jungles, it has been somewhat disheartening as I observe many fraud perpetrators go away scot-free and live a life of super luxury on minority investors’ hard-earned money. And these perpetrators make tempting offers to various parties in the financial community to go along with their schemes. When investors have knowledge in their hands, we have a choice to stay away from these people and away from temptations and do the things that we think are right. With knowledge, we have a choice to invest in the hardworking Asian entrepreneurs and capital allocators who are serious in building a wide-moat business.

|

| CONNECT WITH US |

| MOAT REPORT ASIA OUR TEAM SUBSCRIBE MEMBERS CONTACT US

The Moat Report Asia Other offices: London, Singapore, Zurich |