Chaebolution and the Perils of Sum-of-the-Parts (SOTP) Valuation

June 10, 2014 Leave a comment

“Bamboo Innovators bend, not break, even in the most terrifying storm that would snap the mighty resisting oak tree. It survives, therefore it conquers.” |

| BAMBOO LETTER UPDATE | Jun 9, 2014 |

| Bamboo Innovator Insight (Issue 37) |

|

Chaebolution and the Perils of Sum-of-the-Parts (SOTP) Valuation

등잔 밑이 어둡다 or “It is dark under the lamp”, a local Korean proverb

“Nature has made up her mind that what cannot defend itself shall not be defended.” – Ralph Waldo Emerson (1803-1882)

“I started the passenger car business because I believed that it would surely be an important strategic business in Korea after 10 or 20 years. I know that we cannot make money in the first five or six years even though we invest 10 billion dollars. However, I know that the 10 billon dollars would surely raise the national competitiveness of our automobile industry in the long run.” – Samsung Chairman Lee Kun-hee

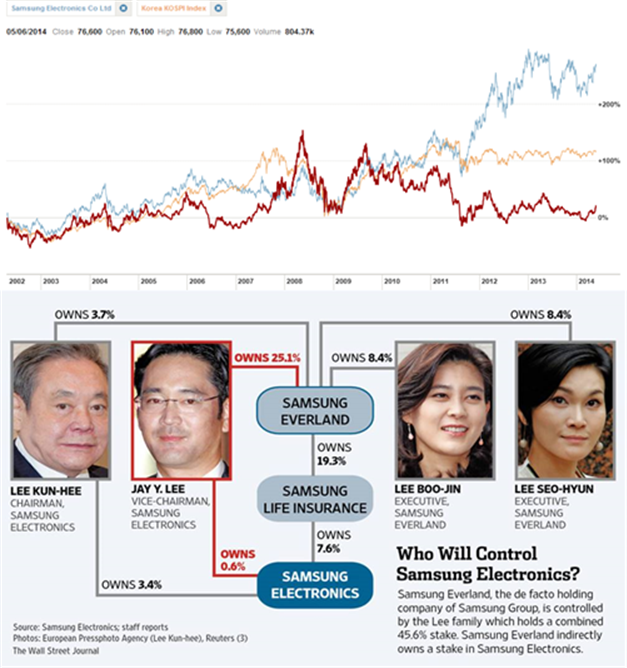

The “Chaebolution” movement – the transition towards meaningful restructuring for the diversified Korean conglomerates with complex circular shareholdings – is marking its most significant event last week. Samsung Group announced that Samsung Everland, which sits at the apex of an intricate web of circular shareholding, is going for listing and conversion into the Group’s holding company by early next year. Such spider web shareholdings is said to fester self-dealings, tunneling and expropriation activities by the controlling shareholders at the expense of long-suffering minority shareholders, resulting in the “governance discount” for Korean shares. With the listing, Samsung Group affiliates could account for over 30% of the market value of all listed companies in Korea. We like to argue that until a business group has gone through its own “chaebolution”, investors mechanically using sum-of-the-parts (SOTP) valuation method in summing up the imputed values of individual segments will be overestimating the enterprise value for conglomerates. This is because managers have incentives to manipulate and transfer earnings from segments operating in industries with lower valuation multiples to those with higher multiples, as doing so will lead to higher equity valuations. Compared to firm-level earnings, segment-level reports often involve more managerial discretion and are subject to less auditor scrutiny. To understand the implications of Samsung Group’s conversion to a holding company structure as part of the “forced refocusing” theme in Korea and Asia, we need to travel back twenty years ago with Samsung’s chairman Lee Kun-hee in his Porsche.

A car buff who loved to race around his company-owned racetrack, Lee had announced plans for Samsung Motors in 1994. This was a year after Lee undertook the famous burning ceremony of phones to demonstrate Samsung’s commitment to quality. The Great Samsung Machine cranked up its powerful efficient levers and the strategy was implemented at an incredible speed. Only two and a half years after the conclusion of the technology transfer agreement with Nissan, Samsung had completed construction and tooling of a $3-billion state-of-the-art production facility in Pusan that was ready to produce 240,000 cars per year. This is a remarkable feat because Samsung was able to leverage its brand reputation, group synergy in resource sharing, and market power in cross-subsidization by the flagship Samsung Electronics and various affiliates, such as direct subsidy and debt guarantees to procure the necessary capital at low cost. Lee was in a rush to “prove” his leadership credentials both inside Samsung and beyond after taking over the top post from his patriarch father Lee Byung-chull in 1987. After succeeding his father, Lee’s first project was the establishment of Samsung General Chemical, a foray that ended in failure. Lee needed a “next big thing” and Samsung Motors fits as the perfect legitimacy-seeking business.

Despite rave reviews, coupled with a trendy design studio in Los Angeles, Samsung Motors sold 45,000 cars, mostly to employees, when the first production output rolled out in March 1998. Samsung Motors had driven straight into the Asian Financial Crisis, with its woes compounded by the global excess of auto production capacity. Due to Lee’s insistence to locate the new factory in the home province of the former president Kim Young-sam, Samsung Motors suffered a severe cost disadvantage – nearly 40% more in setup costs per car than the competitors. Samsung Motors had to shutter its auto factory in Dec 1998 and declared bankruptcy in mid-1999, owing creditors over $3.7bn. It has been estimated that the startup’s total losses ultimately came to $13bn. In May 2000, Samsung Motors was sold to Renault. In place of cash payments, Lee handed creditors shares in Samsung Life (032380 KS, MV $19.9bn) as collateral for the debt on condition…

<Article snipped>

Samsung Electronics Vs LG Electronics and KOSPI – Stock Price Performance, 2002-2014

There is a Korean saying: 등잔 밑이 어둡다, or “It is dark under the lamp”. In applying SOTP as the lamp to light up the value of Asian conglomerates with their multiple business segments and affiliates, it is critical for value investors to STOP first to investigate the critical governance factor under the lamp. This dark source under the lamp is the master controller of the transient light thrown out to shine the segmental profits. The SOTP valuation method tends to overestimate firm value if not adjusted for inter-segment profit transfer and that the measurement errors increase with segment valuation dispersion. Understanding managers’ incentives to manipulate segment-level earnings is critical in pricing these companies properly.

To read the exclusive article in full to find out more about the implications of the forced refocusing on Samsung Group and its business affiliates, including the impact of the hidden debt guarantees and contingent liabilities, and the accounting and equity valuation insights of the chaebolution on other conglomerates such as the Hyundai Motor Group, please visit:

Value Unplugged 2014 and Value Investing Seminar in July in Italy Value Unplugged 2014 (www.valueunplugged.com) in Naples, Italy is now full. We’ll gather in a small, relaxed setting to learn and make friends. We’ll also attend Ciccio Azzollini’s sold-out Value Investing Seminar in July in Trani, Italy — the definitive summer conference for value investors – as one of the keynote speakers. http://www.valueinvestingseminar.it/content_/relatori.asp?lan=eng&anno=2014 |

| The Moat Report Asia |

|

“In business, I look for economic castles protected by unbreachable ‘moats’.” – Warren Buffett

The Moat Report Asia is a research service focused exclusively on competitively advantaged, attractively priced public companies in Asia. Together with our European partners BeyondProxy and The Manual of Ideas, the idea-oriented acclaimed monthly research publication for institutional and private investors, we scour Asia to produce The Moat Report Asia, a monthly in-depth presentation report highlighting an undervalued wide-moat business in Asia with an innovative and resilient business model to compound value in uncertain times. Our Members from North America, the Nordic, Europe, the Oceania and Asia include professional value investors with over $20 billion in asset under management in equities, secretive global hedge fund giants, and savvy private individual investors who are lifelong learners in the art of value investing.

Learn more about membership benefits here: http://www.moatreport.com/subscription/

https://www.moatreport.com/individual-subscription/?s2-ssl=yes

Our latest monthly issue for the month of June investigates the world’s #1 ODM (Original Design Manufacturer) and global #5 manufacturer of a consumer healthcare device product that is used frequently, even daily, thus providing the foundation for stable recurring cashflow. This company is also a hidden champion in a niche product segment (50-55% of group’s sales) that has become a high-growth fashion product currently accounting for less than 10% of the overall industry. The company is able to mass-manufacture this niche product, but not the giants, because of its unique process IP in flexible manufacturing system and know-how to handle large-scale complex orders. The manufacture of this product itself is difficult to replicate and requires FDA/CE licenses because of its medical device nature and the entry barrier is not capital but the know-how and R&D expertise. In particular, the manufacturing integrates different fields of science including polymer chemistry, physics, optics, engineering, materials control, process control, microbiology, and, injection molding. The firm has also developed a proprietary system of tracking the manufacturing process of different sets of product so that if a quality issue arose, when and where the problem set of products was being produced could be swiftly identified, thus diminishing the scale and cost of product recall. This system has helped the firm win the long-term trust of its ODM customers to place stable large orders. The Big Four giants do not have such a system and have to incur substantial losses from product recalls. The company also possess its own brand which has many loyal followers and support in its home market where it enjoys a 30% market share and contributes to 25% of group’s sales while sticky ODM customers account for 75% of group’s sales, mainly from the Japan market. As a result of its wide-moat advantages, the firm enjoys a consistently high ROE of 41%, double or triple that of the giants. From FY07 onwards, even during the depths of the Global Financial Crisis in 2007/09, the firm has not raised equity. Since listing in Mar 2004, the company has only done one rights issue in May 2005. Also, it is able to sustain a strong stable cash dividend payout (>70% with 3% yield) with its healthy net-cash balance sheet (net cash $30m; net cash-to-equity ratio 23%) and proven management execution in prudent capex expansion to support sustainable quality earnings growth. M&A deals in the healthcare and medical device sector has been growing due to their strong defensive nature and giants seeking growth to overcome their own patent cliff. The firm will always be an attractive takeover target by giants who wish to swallow it up to possess its valuable flexible manufacturing system and know-how to fill their own missing competency gap and hence will enjoy long-term downside protection in its terminal value. In the battle between “ODM vs Brand”, we find the story of the company to be quite similar to that of TSMC (2330 TT, MV $103bn), now the largest ODM foundry in the world. “Skate to where the puck is going to be, not where it has been,” as hockey legend Wayne Gretzky advised. In our view, the profit and valuation premium in the value chain will start to skate to the “Inno-facturers” who are the hidden ODM innovators (the brand behind brands) consolidating the industry, such as TSMC and this company. While its valuation is not cheap with EV/EBIT (FY13) at 20.6x, when we compare EV/EBIT relative to ROE, the company is relatively cheap, by as much as 130-220% when compared to giants and other comparables. When we compare EV/EBITDA relative to ROE, the valuation gap is 90-160%.This long-term valuation gap implies that the company, with its far superior and sustainable ROE, could potentially double to $2.4bn, as it continues to consolidate its niche product segment and enter into a new product cycle of an innovative product whose patents are expiring in 2014/15 (US/worldwide) to make ASP/margin improvements in sustaining quality profits and cashflow. Its share price has dropped 18% from its recent high and underperformed the index by 26% in the last six months. This will present a buying opportunity for long-term value investors who can penetrate beyond conventional valuation metrics because of a deep understanding of its business model and underlying source of its wide-moat advantages. In Asia, many firms break apart or become value traps due to shareholder conflict, envy and differences in opinion on the business direction of the company. The stable long-term corporate culture infused by the late founder, who established the company in 1986 with the current executive chairman and 2 other key shareholders, to combine the energy and ideas of everyone to work hard to keep the business running forever is underappreciated.

Our past monthly issues examine:

The Moat Report Asia Members’ Forum has been getting penetrating quality dialogues from our subscribers.Questions range from:

Do find out more in how you can benefit from authentic and candid on-the-ground insights that sell-side analysts and brokers, with their inherent conflict-of-interests, inevitable focus on conventional stock coverage and different clientele priorities, are unwilling or unable to share. Think of this as pressing the Bloomberg “Help Help” button to navigate the Asian capital jungle. Institutional subscribers also get access to the Bamboo Innovator Index of 200+ companies and Watchlist of 500+ companies in Asia and the Database has eliminated companies with a higher probability of accounting frauds and misgovernance as well as the alluring value traps.

|

| Professional Development Workshops for Executives and Lifelong Learners |

|

Our 7th run of the series of workshop From the Fund Management Jungles: Value Investing Exposed and Explored – (Part 1) Moat Analysis, (Part 2) Tipping Point Analysis and (Part 3) Detecting Accounting Fraud – on 8 Mar 2014 has been well-received with serious value investors, professionals, and serious lifelong learners attending.

Our 8th workshop on Tipping Point Analysis will be held in June 14; we are taking a short break as our business partner Linda is delivering her new baby!

Thank you for your support all this while!

|

|

Thank you so much for reading as always.

Warm regards, KB Kee Managing Editor The Moat Report Asia

Singapore Mobile: +65 9695 1860

A Service of BeyondProxy LLC 1608 S. Ashland Avenue #27878 Chicago, Illinois 60608-2013 Other offices: London, Singapore, Zurich

|

|

P.S.1 Here is a little more about my background: KB Kee has been rooted in the principles of value investing for over a decade as an analyst in Asian capital markets. He was head of research and fund manager at Aegis Portfolio Managers, a Singapore-based value investment firm. As a member of Aegis’ investment committee, he helped the firm’s Asia-focused equity funds significantly outperform the benchmark index. He was previously the portfolio manager for Asia-Pacific equities at Mirae Asset Global Investments, Korea’s largest mutual fund company. He holds a Masters in Finance and degrees in Accountancy and Business Management, summa cum laude, from Singapore Management University (SMU). KB had taught accounting at his alma mater in Singapore Management University and had also published an empirical research paper Why ‘Democracy’ and ‘Drifter’ Firms Can Have Abnormal Returns: The Joint Importance of Corporate Governance and Abnormal Accruals in Separating Winners from Losers in the Special Issue of Istanbul Stock Exchange 25th Year Anniversary Best Paper Competition, Boğaziçi Journal, Review of Social, Economic and Administrative Studies, Vol. 25(1): 3-55. KB has trained CEOs, entrepreneurs, CFOs, management executives in business strategy, macroeconomic and industry trends in Singapore, HK and China.

P.S.2 Why do I care so much about doing The Moat Report Asia for you? My personal motivation in embarking on this lifelong journey has been driven by disappointment from observing up close and personal the hard-earned assets of many investors, including friends and their families, burnt badly by the popular mantra: “Ride the Asian Growth Story!” I witnessed firsthand the emotional upheavals that they go through when they invest their hard-earned money – and their family’s – in these “Ride The Asian Growth Story” stocks either by themselves or through money managers, and these stocks turned out to be the subject of some exciting “theme” but which are inherently sick and prey to economic vicissitudes. They may seem to grow faster initially but the sustainable harvest of their returns is far too uncertain to be the focus of a wise program in investment. Worse still, the companies turned out to be involved in accounting frauds. Their financial numbers were “propped up” artificially to lure in funds from investors and the studiously-assessed asset value has already been “tunnelled out” or expropriated. And western-based fraud detection tools and techniques have not been adapted to the Asian context to avoid these traps.

After a decade-plus journey in the Asian capital jungles, it has been somewhat disheartening as I observe many fraud perpetrators go away scot-free and live a life of super luxury on minority investors’ hard-earned money. And these perpetrators make tempting offers to various parties in the financial community to go along with their schemes. When investors have knowledge in their hands, we have a choice to stay away from these people and away from temptations and do the things that we think are right. With knowledge, we have a choice to invest in the hardworking Asian entrepreneurs and capital allocators who are serious in building a wide-moat business.

|

| CONNECT WITH US |

| MOAT REPORT ASIA OUR TEAM SUBSCRIBE MEMBERS CONTACT US

The Moat Report Asia Other offices: London, Singapore, Zurich

|